Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

The U.S. dollar fell in 2025 but strengthened in 2026, affecting overseas returns for U.S. investors.

Interest rates, trade flows, global investment demand, and inflation expectations influence the value of the dollar.

Currency fluctuations can affect short-term returns, but diversified investors should stay focused on long-term goals.

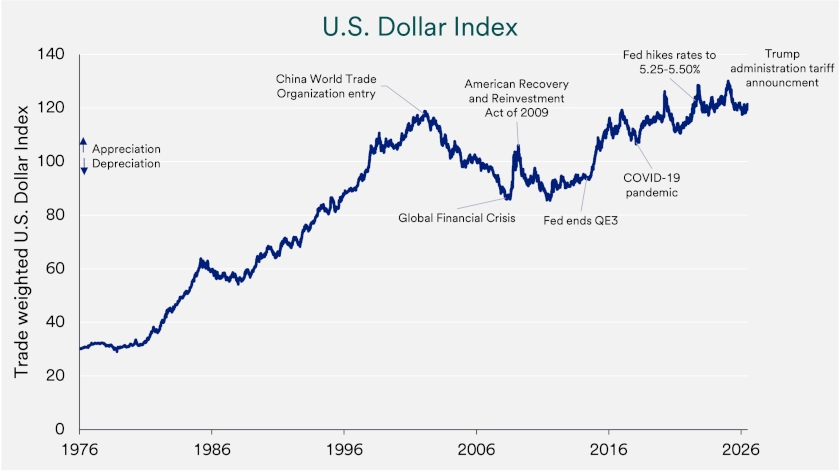

The U.S. dollar has moved enough to influence globally invested portfolios. The U.S. Dollar Index, or DXY, tracks the value of the U.S. currency against a basket of major global currencies. The index declined 9.4% in 2025, then rose 2.7% year-to-date in 2026 through July 8 after slipping early in the year. 1

Those moves helped foreign stocks outperform U.S. stocks in 2025 and early 2026, partly because U.S. investors benefited when converting foreign gains back into dollars. A weaker dollar can add to returns from investments priced in other currencies, while a stronger dollar can reduce those converted returns. Investors can’t control day-to-day currency shifts, but they can control their investment mix, diversification and time horizon.

Currency markets move as money flows around the world through trade and finance. Investors compare opportunities across countries, including interest rates, economic growth, inflation trends and market stability. “Relative currency values reflect the global flow of funds,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group. “When the dollar strengthens, it means more foreign money is flowing into the U.S. than out.”

“Relative currency values reflect the global flow of funds. When the dollar strengthens, it means more foreign money is flowing into the U.S. than out.”

Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group

Four forces often shape the value of the dollar: interest-rate differences, global investing demand, trade flows, and inflation expectations. Higher interest rates can attract money into a country when investors believe the potential return compensates them for the risk. Trade flows can also support a currency because countries that sell more goods abroad than they buy typically create steady demand for their currency as buyers pay for those exports. Inflation can work in the opposite direction by reducing purchasing power, which can pressure a currency compared with peers where prices rise more slowly. When these forces shift quickly, currencies can respond quickly.

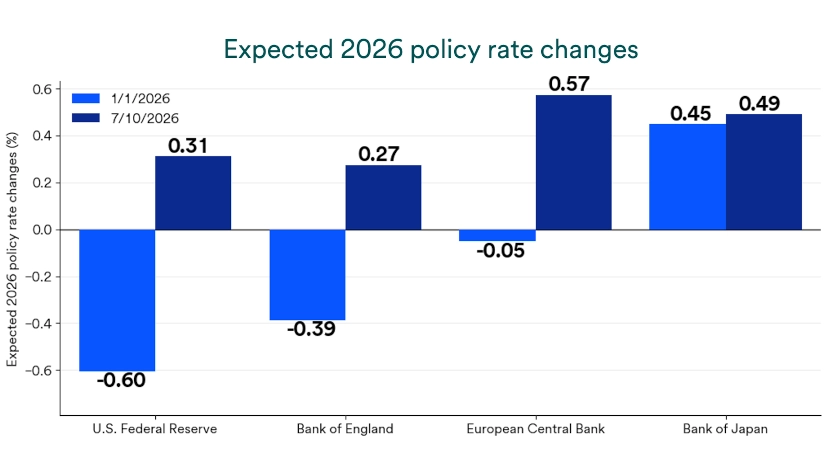

Two policy-related developments helped weaken the dollar in 2025. President Trump announced tariffs, which raised inflation expectations, while investors also anticipated more Federal Reserve (Fed) rate cuts, and those forces helped push the dollar sharply lower early in the year. Later, as inflation stabilized and expectations for rate cuts steadied, the dollar traded in a relatively narrow range. “Fed rate cut expectations can move the U.S. dollar because interest rates and bond yields direct global capital flows,” notes Bill Merz, head of capital markets research for U.S. Bank Asset Management Group. “So far in 2026, the shift from expected Fed rate cuts to potential hikes boosted the dollar, especially considering expectations for Fed hikes exceeded changing policy expectations from other major central banks like the European Central Bank, Bank of Japan, and Bank of England.”

When the dollar strengthens, U.S. consumers often see the effect first through the price of imported goods. The math is straightforward: a German car priced at €50,000 costs $60,000 when the exchange rate is $1.20 to €1, but the same car costs $45,000 if the dollar strengthens to $0.90 to €1. The price in euros does not change, but the exchange rate changes the cost for a U.S. buyer.

A stronger dollar can create a different challenge for large U.S. companies that sell products and services overseas. When those companies convert foreign sales back into dollars, a stronger dollar can reduce the reported value of those revenues. It can also make U.S. exports more expensive for foreign buyers, which may reduce demand and weigh on sales. “If the dollar continues to strengthen, it could dampen corporate earnings, which could impact stock market performance in the short term,” says Haworth.

For U.S. investors, currency tends to have the biggest impact when they own assets outside the United States. Haworth advises investors not to over-focus on currency moves when evaluating domestic stocks, but he sees currency effects as more meaningful in overseas investments because gains and losses eventually convert back into dollars. The 2025 results illustrate that point clearly: the MSCI EAFE Index returned 23.7% in local currency, but U.S. investors earned 31.2% after conversion because the dollar weakened notably in the first half of the year. 2

The reverse can also happen when the dollar strengthens. A strong dollar can reduce what a U.S. investor receives from foreign gains after conversion, even when the underlying investment performs well in its local market. That makes currency one part of the return equation for international investments, alongside earnings growth, valuation, interest rates and economic fundamentals.

Even so, currency is usually a supporting role rather than driving the full investment story. “Currencies fluctuate less than stocks overall, and predicting their direction is difficult because numerous factors influence relative currency values,” says Haworth. “Equity investors, in particular, should be somewhat insensitive to short-term dollar trends when positioning long-term investment assets.”

The value of the U.S. dollar changes over time as investors, businesses, and governments respond to shifts in economic conditions and confidence. Interest rates in the United States play a major role because higher rates often attract money into Treasury bonds and other dollar-based investments, which can lift the currency. Lower rates can reduce that support. Inflation, demand for safe investments, and a changing trade deficit can also shape the dollar’s path over longer periods.

The U.S. dollar remains central to the global financial system. Countries, companies, and banks use it every day to trade goods, borrow money, and settle payments across borders. Many key commodities, including oil, are priced in dollars, which helps sustain currency demand. A large share of global debt is also issued in dollars, especially in emerging markets. Because so many financial transactions move through dollar-based systems, the currency continues to hold a leading role in world finance.

Long-term currency trends usually reflect the strength and stability of a country’s economy. Steady growth, trusted institutions, and confidence in financial markets can attract foreign investment and support the dollar over time. Trade also plays a role because stronger exports can increase demand for U.S. goods and services. Inflation and interest rates remain important as well. Persistent inflation can weaken a currency, while stable prices and competitive rates can help the dollar hold its value.

Currencies move every day, but major shifts usually develop slowly. Investors, businesses, and central banks often wait for clearer signs that economic trends are lasting before making large changes. Long-term trade agreements, loans, and other financial commitments also limit sudden swings in demand. The foreign exchange market is the largest and most liquid in the world, so it takes sustained pressure to move major currencies in a lasting way. As a result, big changes in the dollar usually build over time.

The practical takeaway is to stay anchored to a diversified approach and discuss any major overseas exposure with your wealth management professional, especially when headlines tempt quick reactions.

The dollar often moves as money flows around the world through trade and investing. Interest‑rate differences, demand for investments across countries, trade flows, and inflation expectations can all push the dollar higher or lower.

A strong dollar can lower the cost of imports, but it can also weigh on U.S. companies that sell overseas by shrinking foreign revenues once they convert back into dollars. It can also reduce what U.S. investors receive from foreign gains after conversion back into dollars.

A weak dollar can boost the dollar value of overseas gains when investors convert them back into dollars. It can also raise the cost of imports, which may add inflation pressure over time.

In recent years, the communications services and information technology sectors routinely outperformed the broader S&P 500, despite exhibiting some volatility, and this trend is expected to continue in 2026.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.