Capitalize on today’s evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Current inflation affects the economy through living costs, household purchasing power, business expenses and interest rates, even when monthly price data improves.

Energy, shelter costs and tariffs shape the impact of inflation, while market-based expectations help investors assess whether inflation is rising or easing.

Federal Reserve policy will respond to inflation and employment data, supporting a diversified investment approach as the outlook changes.

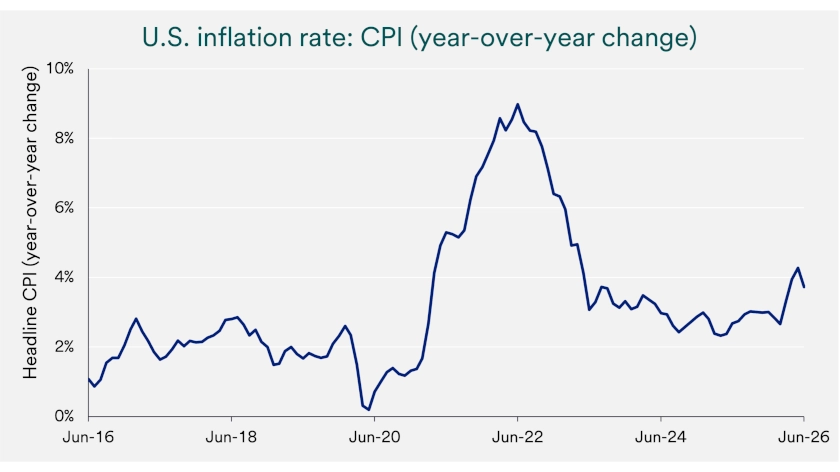

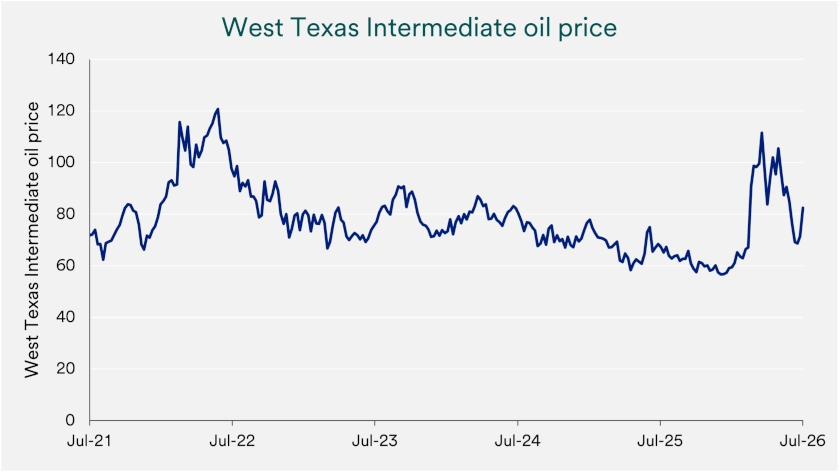

Current inflation affects the economy by raising the cost of living, influencing interest rates, and shaping investment decisions. In June 2026, the year-over-year Consumer Price Index (CPI) slowed from 4.2% to 3.5%. 1The decline offered relief to consumers, businesses and investors, but inflation still exceeded the Federal Reserve’s 2% long-term goal. Rising oil prices in recent weeks have led to investor questions about the durability of price deceleration witnessed in the June report.

Households experience the impact of inflation through purchasing power, or how much each dollar can buy. When prices rise faster than income or investment returns, families must spend more on the same goods and services, leaving less for saving and other goals. The Federal Reserve (Fed) may also keep interest rates higher when inflation stays elevated, which raises borrowing costs across the economy.

Energy drove much of June’s improvement in current inflation. The energy index fell 5.7% during the month, led by a 9.7% decline in gasoline prices, and those declines more than offset increases in food and shelter costs. Even after June’s drop, energy prices stood 15.7% above their June 2025 level and gasoline prices remained 26.7% higher, showing how quickly energy can change the inflation outlook.

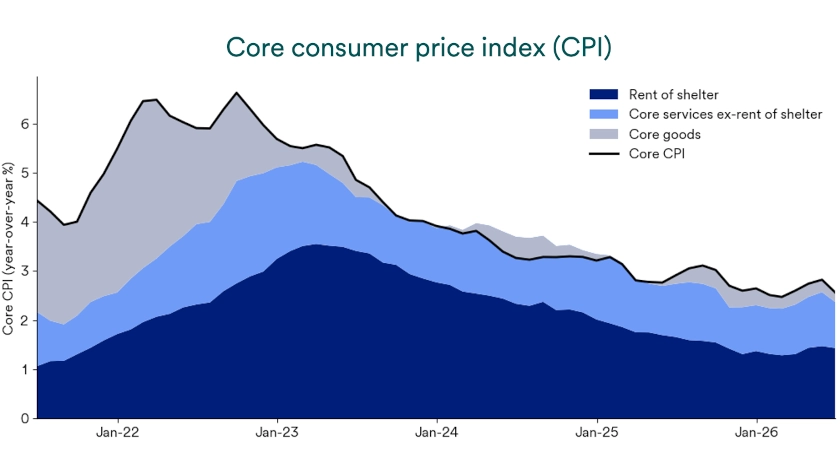

Core CPI excludes food and energy, two categories that can move sharply from month to month, to provide a clearer view of underlying price trends. Core prices rose 2.6% over the prior 12 months, down from 2.9% in May. The softer reading can influence interest rate expectations, but one month does not establish a lasting trend.

Shelter costs deserve close attention because housing consumes a large share of household budgets and carries significant weight in the CPI. The shelter index rose just 0.1% in June, its smallest monthly increase since January 2021, while rent for a primary residence increased 2.8% over the prior year. Official shelter measures often adjust slowly because leases reset when tenants relocate or renew, so reported inflation can lag changes in current market rents.

Former Fed Governor Stephen Miran described that delay in a December 15, 2025 speech. He said the earlier “catch‑up” in measured shelter inflation was largely complete and described elevated readings as an “after‑echo of past imbalances.” His assessment supports the possibility that shelter inflation could slow more quickly as the official data reflect today’s softer rent growth. 2

Geopolitical conflict can push inflation higher by disrupting energy supplies or increasing shipping and insurance costs. Consumers see higher oil and gasoline prices directly at the pump and indirectly through transportation, production and delivery costs. If those increases persist, consumers and businesses must absorb higher costs without an equivalent increase in income, which can slow economic growth and complicate Fed decisions.

“Markets are sensitive to sustained, accelerating inflation, but underlying inflation ex-energy has been modest in recent months,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group. Haworth adds, “Labor market weakness could suggest higher economic slowdown odds, which would represent a material market development, although recent labor market data has been encouraging.” Investors should assess inflation alongside employment and economic growth rather than treat one indicator as a complete market signal.

“Markets are sensitive to sustained, accelerating inflation, but underlying inflation ex-energy has been modest in recent months. Labor market weakness could suggest higher economic slowdown odds, which would represent a material market development, although recent labor market data has been encouraging.”

Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group

Tariffs can also raise the cost of imported goods and the materials U.S. companies use. President Trump recently announced a plan for 50% tariffs on certain Canadian goods under Section 338 of the Tariff Act of 1930, following a Supreme Court ruling that canceled most tariffs imposed under the International Emergency Economic Powers Act. Because tariff policy and related legal developments can change, investors should focus on how the measures ultimately affect import costs and consumer prices.

Economists can gauge the broad effect of tariff policy through the “effective tariff rate,” which compares customs revenue with the total value of imported goods. Businesses may absorb part of the cost, pass part of it to consumers or adjust supply chains. Those choices can cause tariffs to affect inflation unevenly and after a delay.

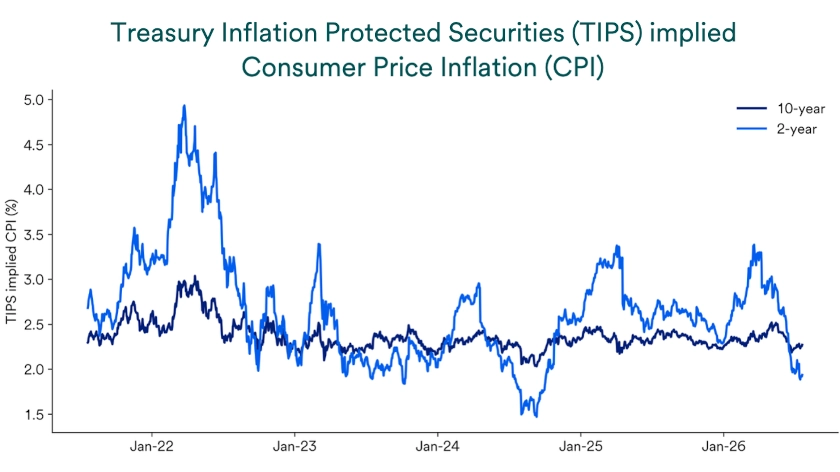

Market-based inflation expectations currently point to fading concern. “Capital markets can provide a valuable source of information about the outlook for inflation, because they often incorporate new information faster than lagging economic data or official forecasts,” says Bill Merz, head of capital markets research for U.S. Bank Asset Management Group. Prices from billions of dollars of bond transactions can help estimate future headline inflation. Bond-market prices indicate lower inflation expectations than when the Middle East conflict began and lower expectations than the average over the past three years. That conflicts with recent oil price increases as Middle East tensions escalated.

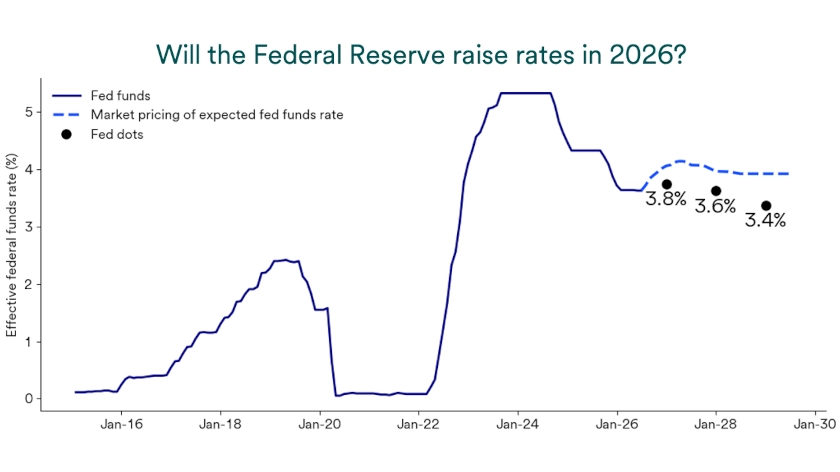

The Fed held the federal funds target range at 3.50% to 3.75% at its June 17, 2026, meeting and said economic activity continued to expand at a solid pace despite elevated uncertainty tied partly to the Middle East conflict. Inflation still exceeded the Fed’s 2% goal, partly because supply disruptions raised prices in certain sectors such as energy. That combination keeps interest rate expectations sensitive to each new inflation, labor market and consumer spending report.

The Fed’s June projections showed a firmer inflation outlook. Policymakers projected 2026 Personal Consumption Expenditure (PCE) inflation at 3.6% and core PCE inflation at 3.3%, both above the Fed’s 2% longer-run objective. PCE measures prices across a broad range of consumer spending, while core PCE excludes food and energy to highlight underlying trends, and the median federal funds rate projection signals that the Fed may need to raise rates if inflation stays elevated.

Investors should focus on the interaction among energy prices, tariffs, shelter costs, consumer spending and Fed policy rather than any single inflation report. Falling energy prices and slower shelter inflation could ease headline and core inflation, while energy shocks, tariffs or firm demand could keep inflation elevated and lead the Fed to hold rates higher for longer or consider additional increases. The path will depend on incoming data because energy markets, policy decisions and consumer or business behavior can change inflation quickly.

A diversified investment strategy can help investors stay aligned with long-term goals as inflation and interest-rate expectations adjust. Diversification cannot prevent losses, but it can reduce dependence on one market outcome or inflation forecast. Investors should expect this outlook to keep changing as new reports are released.

Inflation matters to investors because it can reduce the real value of portfolio growth over time. Even when an account balance rises, those gains may buy less if the cost of goods and services continues to increase. For long-term investors, the goal is not only to grow assets, but also to preserve purchasing power.

Inflation can also influence interest rates, which can affect both bonds and stocks. When rates move higher, older bonds with lower yields often lose value in the market. Higher rates can also weigh on stock prices by reducing the present value of future earnings. A diversified investment strategy can help investors manage these risks while staying focused on long-term growth.

Inflation reduces purchasing power by making everyday goods and services more expensive over time. As prices rise, each dollar buys less than it did before. This gradual change can affect household budgets, retirement planning, and long-term savings goals.

The long-term impact can be significant. Based on the Consumer Price Index from the U.S. Bureau of Labor Statistics, something that cost $1 at the start of 2000 cost about $1.93 by the start of 2026. That means prices nearly doubled over that period, showing why inflation remains an important part of financial planning and investment strategy.

Inflation explains the difference between nominal returns and real returns. A nominal return is the number shown on an investment statement, paycheck, or savings account. A real return adjusts for inflation and shows how much buying power increased after rising prices are considered.

For example, a bond may pay a 5% nominal yield over a year. If inflation averages 2% during that same period, the real return is closer to 3%. Investors track this difference because strong long-term results depend on growing wealth faster than the cost of living.

Many people notice inflation when prices jump in a given month or year. Investors usually focus on inflation as a long-term risk because prices tend to rise over time, even when inflation slows for a period. That steady increase can gradually reduce the future value of savings and investment gains.

For long-term investors, inflation is not just a short-term headline. It is an ongoing part of portfolio planning, retirement income planning, and wealth preservation. A sound investment approach aims to outpace inflation over time so investors can maintain spending power and stay on track toward long-term financial goals.

The best response to an uncertain inflation path is to stay focused on what you can control. Inflation remains a key driver of interest rates and market volatility, and tariffs and energy shocks can create short-term setbacks even when the longer-term trend is improving. A disciplined plan and a broadly diversified portfolio can help investors avoid making lasting decisions based on a single report or a short burst of volatility. That approach can keep long-term goals at the center of the plan.

If inflation continues to cool, especially if shelter inflation keeps easing with a lag, the case for lower rates can strengthen. If energy prices rise sharply or tariffs become more inflationary than expected, that timeline can shift. Talk with your financial professional

In June 2026, CPI increased 3.5% over the prior 12 months and fell 0.4% for the month. 1 Those figures reflect the average change in prices across a broad basket of goods and services. Inflation can still feel uneven because housing, food and energy prices do not always move in the same direction as the overall average.

Core inflation removes food and energy because those prices can move sharply from month to month. In June, core CPI was unchanged for the month and 2.6% from a year earlier, which showed that underlying inflation pressure was still present. 1 Core measures can help investors see whether inflation is easing in the parts of the economy that tend to move more slowly.

The Federal Reserve has said it targets 2% inflation over time as measured by the core Personal Consumption Expenditures price index. PCE can better reflect how consumers change what they buy when prices move, and it covers a broader set of spending categories. That is why PCE often carries more weight when investors think about the path of interest rates.

Federal Reserve calibrates monetary policy to help lower inflation.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.