Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

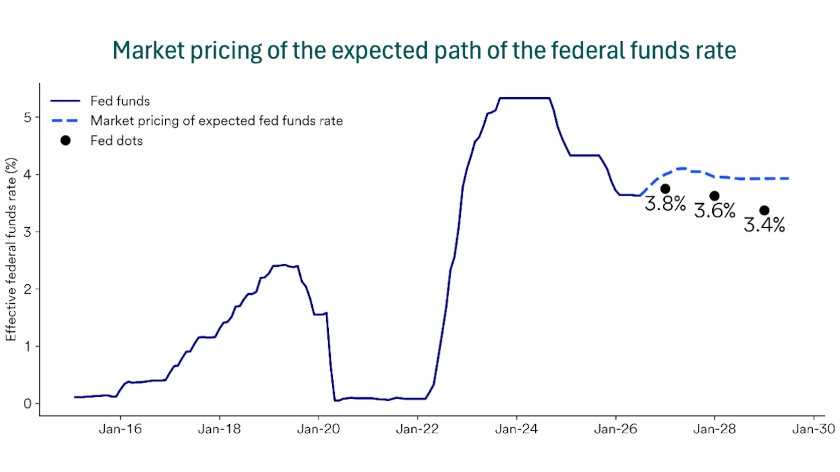

The U.S. Federal Reserve (Fed) kept its policy interest rate at a range of 3.50%-3.75% citing somewhat tighter financial conditions through higher market-based rates.

Kevin Warsh made no change to the previous, shortened Fed statement in his second meeting as Fed Chair, and reiterated the Fed’s 2% inflation target and the importance of restoring Fed credibility after years above that target.

Markets now price in high odds of a rate hike later in 2026 amid elevated inflation and energy prices.

The Federal Reserve held its target federal funds interest rate in the 3.50%-3.75% range at its July meeting, a decision investors generally expected. Nine members voted to leave the rate unchanged, while three members dissented, favoring a 0.25% hike. Ahead of the decision, investors expected a 35% chance of a rate increase. Elevated inflation, primarily stemming from higher energy prices, increased investor expectations for higher policy rates later this year. Investors now anticipate between one and two rate hikes by the end of 2026.

Fed Chair Kevin Warsh reinforced past comments relating to the Fed’s role and shared insight into the decision to hold rates steady:

Fed interest rate increases from 2022-2023 helped mitigate inflation over the past four years, but higher oil costs are again escalating near-term prices. The Core Personal Consumption Expenditures (PCE) Price Index accelerated from 3.0% in December 2025 to 3.4% in May 2026. West Texas Intermediate crude oil front month futures prices rose from near $57 per barrel at the beginning of the year to a peak of $113 in April. Prices fell before rising back above $84 this week. Higher energy prices, from constrained global supplies, have stoked many inflation readings and complicated the Fed’s outlook as it balances its mandates of maximum employment and price stability.

On the balance sheet, the Fed stopped shrinking its bond holdings in December. Those holdings stand near $6.6 trillion today after peaking near $9 trillion in 2022. The Fed began buying short-term Treasury bills in December 2025 to ensure ample banking system reserves and to keep short-term interest rates near their intended policy rate. The Fed recently announced it would reduce regular purchases. Expanding the balance sheet by purchasing Treasury bills results in improved market liquidity by absorbing a portion of incremental supply. Liquidity, the money readily available to purchase goods, services and financial assets, can also cushion markets against unforeseen financial market shocks, and liquidity measures remain constructive. Warsh has expressed reservations about its long-run efficacy and questioned its appropriateness as policy tool, forming a task force to explore the topic.

Two-year Treasury yields fell 0.02% to 4.27% today as investors removed the lingering possibility of a hike this week. However, 10-year Treasury yields rose 0.08% to 4.69% and 30-year yields rose 0.12% to 5.21%, the highest level since 2007; investors appear concerned inflation could remain persistent without tighter policy rates. Large stocks, represented by the S&P 500, fluctuated, eventually falling 1.5%, while small stocks fell 1.6%, represented by the Russell 2000 Index.

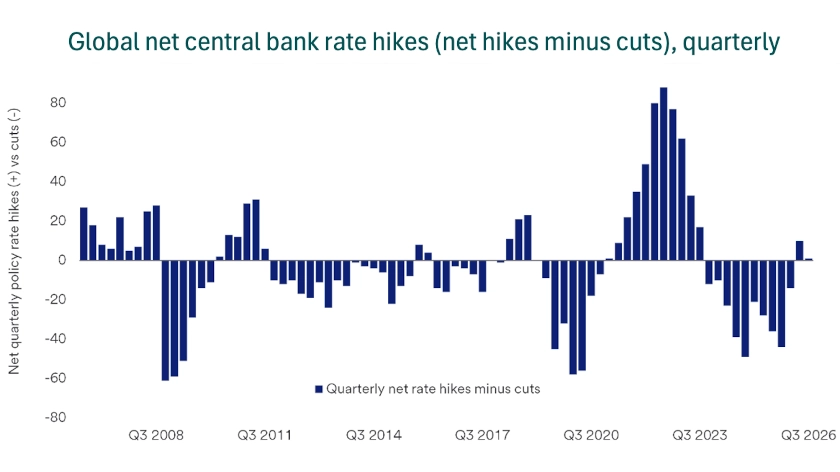

Globally, central banks eased policy in 2025, but many increased rates in response to recent energy price increases. The European Central Bank and Bank of Japan each increased rates so far this year, with the Bank of England and Bank of Canada expected to increase rates at some point this year.

We maintain a constructive outlook for diversified portfolios and see opportunities in growth-oriented allocations including U.S. stocks, global infrastructure and structured credit. While higher energy costs risk increasing inflation and dampening economic activity, consumer spending and corporate earnings growth remain resilient, with fiscal support in the form of lower corporate and individual taxes and recent tariff rebates. Diversified portfolios spanning a variety of allocations can help limit the impact of price swings on individual assets. We will keep you informed as new data arrives and as we update our assessment of market conditions.

As always, we value your trust and are here to help in any way we can. Please do not hesitate to let us know if we can help address your unique financial situation or be of assistance.

This information represents the opinion of U.S. Bank. The views are subject to change at any time based on market or other conditions and are current as of the date indicated on the materials. This is not intended to be a forecast of future events or guarantee of future results. It is not intended to provide specific advice or to be construed as an offering of securities or recommendation to invest. Not for use as a primary basis of investment decisions. Not to be construed to meet the needs of any particular investor. Not a representation or solicitation or an offer to sell/buy any security. Investors should consult with their investment professional for advice concerning their particular situation. The factual information provided has been obtained from sources believed to be reliable but is not guaranteed as to accuracy or completeness. U.S. Bank is not affiliated or associated with any organizations mentioned.

Based on our strategic approach to creating diversified portfolios, guidelines are in place concerning the construction of portfolios and how investments should be allocated to specific asset classes based on client goals, objectives and tolerance for risk. Not all recommended asset classes will be suitable for every portfolio. Diversification and asset allocation do not guarantee returns or protect against losses.

Past performance is no guarantee of future results. All performance data, while obtained from sources deemed to be reliable, are not guaranteed for accuracy. Indexes shown are unmanaged and are not available for direct investment. The S&P 500 Index consists of 500 widely traded stocks that are considered to represent the performance of the U.S. stock market in general. The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index and is representative of the U.S. small capitalization securities market. The Personal Consumption Expenditures (PCE) Price Index is a measure of the prices that people living in the United States, or those buying on their behalf, pay for goods and services. It is known for capturing inflation (or deflation) across a wide range of consumer expenses and reflecting changes in consumer behavior.

Equity securities are subject to stock market fluctuations that occur in response to economic and business developments. International investing involves special risks, including foreign taxation, currency risks, risks associated with possible differences in financial standards and other risks associated with future political and economic developments. Investing in emerging markets may involve greater risks than investing in more developed countries. In addition, concentration of investments in a single region may result in greater volatility. Investing in fixed income securities is subject to various risks, including changes in interest rates, credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in lower-rated and non-rated securities present a greater risk of loss to principal and interest than higher-rated securities. Investments in high yield bonds offer the potential for high current income and attractive total return but involve certain risks. Changes in economic conditions or other circumstances may adversely affect a bond issuer's ability to make principal and interest payments. The municipal bond market is volatile and can be significantly affected by adverse tax, legislative or political changes and the financial condition of the issues of municipal securities. Interest rate increases can cause the price of a bond to decrease. Income on municipal bonds is free from federal taxes but may be subject to the federal alternative minimum tax (AMT), state and local taxes. There are special risks associated with investments in real assets such as commodities and real estate securities. For commodities, risks may include market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes and the impact of adverse political or financial factors. Investments in real estate securities can be subject to fluctuations in the value of the underlying properties, the effect of economic conditions on real estate values, changes in interest rates and risks related to renting properties (such as rental defaults).

U.S. Bank and its representatives do not provide tax or legal advice. Your tax and financial situation is unique. You should consult your tax and/or legal advisor for advice and information concerning your particular situation.

Are tariffs contributing to inflation in the U.S. economy?

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.