Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Consumer spending drives about two-thirds of U.S. economic activity, and June retail sales showed continued demand despite slower job growth and higher household costs.

Retail sales, small-business spending and restaurant bookings point to resilient demand, while higher gasoline prices could reduce spending on other goods and services.

Low layoffs, wage growth and manageable debt payments support the consumer outlook, although pressure varies by income group and borrowing needs.

Consumer spending remains the backbone of the U.S. economy and accounts for approximately two‑thirds of total economic activity. 1 Household purchases support business revenue, employment and investment so changes in spending often shape the pace of economic growth. Spending on necessities such as food, housing and energy provides a steady base, while purchases of travel, dining and entertainment offer a clearer view of households’ financial flexibility.

Households continue to spend, although the pace and mix of purchases vary across income groups and categories. Higher-income households provide important support, while many lower- and middle-income consumers have become more selective as higher prices take a larger share of their budgets. Overall demand continues to expand despite elevated borrowing costs, geopolitical uncertainty and consumer confidence readings that remain low by historical standards.

“Consumer spending continues to benefit from steady income growth and a supportive labor market.”

Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group

“Consumer spending continues to benefit from steady income growth and a supportive labor market,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group. Paychecks, relatively low layoffs and household savings give many consumers the capacity to keep spending. Slower job creation and higher costs warrant attention, but current data do not point to a broad household retreat.

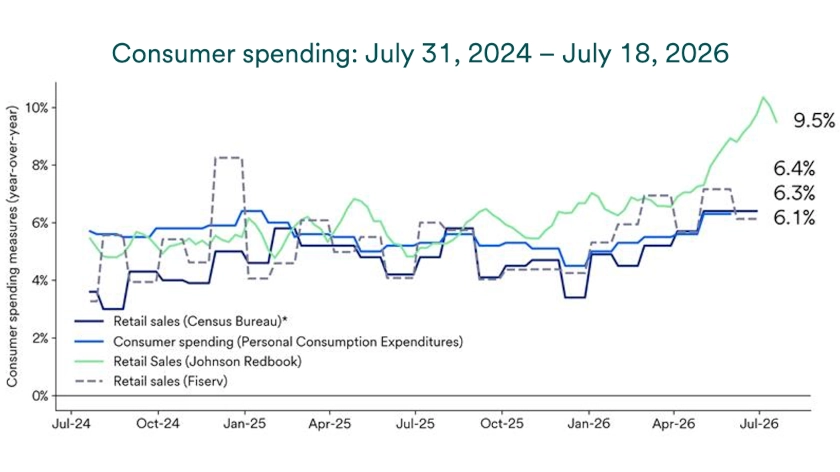

Recent retail sales data show continued growth in household demand. U.S. retail and food services sales rose 6.7% from a year earlier. 2 The annual increase indicates that consumers continue to support economic growth, even as they adjust where and how they spend.

Lower gasoline station receipts held back the overall June result, but several other categories recorded solid gains from a year earlier. Sales excluding automobiles and gasoline rose 5.7%, while online and other non-store retailers posted a 14.2% annual gain. 2 These results point to continued demand across a range of goods, with particularly strong growth in online spending.

Households also continued to spend on experiences, although restaurant sales grew more slowly than goods purchases. Food services and drinking place sales stood 3.8% above their June 2025 level. Consumers remain active, but they appear to compare prices and direct more money toward convenience, value or a compelling experience.

More frequently updated spending measures can reveal changes before broader government reports arrive. “High-frequency retail sales data, point-of-sale readings and restaurant bookings suggest that overall consumer behavior remains solid,” says Bill Merz, head of capital markets research for U.S. Bank Asset Management Group. These measures track transactions and customer activity more often than monthly government reports, helping investors identify shifts in consumer spending sooner.

Fiserv transaction data show that June sales rose 6.1% from a year earlier, while Johnson Redbook data through July 11, 2026 show 8.2% annual growth at department stores, warehouse clubs and supercenters. OpenTable reported a 10% year over year increase in seated diners month to date through July 19. Together, these readings reinforce the view that consumers continue to spend across goods and services.

The conflict in Iran has pushed national gasoline prices up more than one-third since February 27, according to AAA. 3 If those increases persist, households may have fewer dollars available for other goods and services. Higher fuel prices can also add to inflation and influence both consumer behavior and Federal Reserve interest rate decisions.

Elevated tax refunds provided a temporary cushion earlier in the year. Tax legislation passed last year translated to an extra $58 billion in individual tax refunds received so far from 2025 tax returns. 4 Those refunds covered the increase in gasoline spending until earlier in the summer, but they no longer provide meaningful support, increasing the economic importance of a resolution to Middle East tensions.

Consumers have navigated higher energy costs without sharply reducing overall spending so far. Continued income growth, limited layoffs and earlier tax refunds helped many households absorb higher expenses. A prolonged period of elevated gasoline prices would test that resilience, particularly if employment growth slows further or other essential costs remain high.

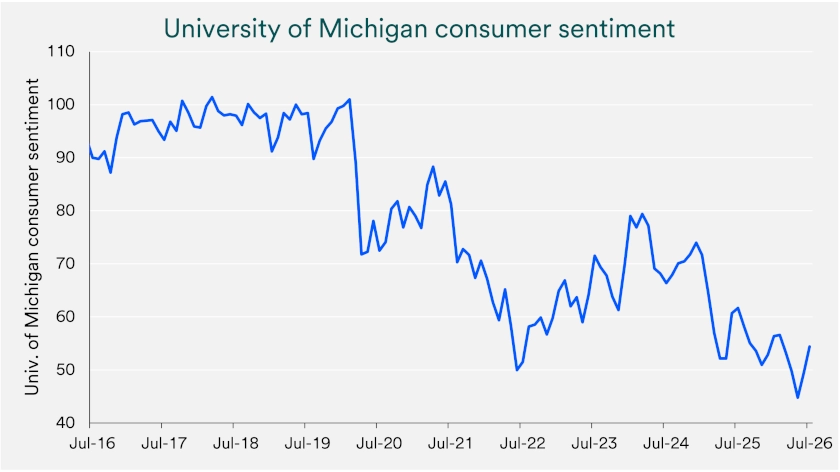

Consumer confidence improved from its May low, although households remain concerned about prices. The University of Michigan’s preliminary Consumer Sentiment Index rose to 54.4 in July from 49.5 in June, 5marking a second consecutive monthly increase and the highest reading since February. The index nevertheless remained below its year-earlier level.

Lower gasoline prices during much of the survey period helped lift July sentiment, while one-ahead inflation expectations eased to 4.2% from 4.6% in June. More than 70% of interviews occurred before renewed military activity on July 7 and the subsequent increase in gasoline prices. This timing limits how fully the July survey reflects consumers’ response to the latest rise in energy costs.

Consumer confidence no longer moves as closely with asset prices and spending behavior as it once did, reducing the values of surveys for economists and investors. Changes in survey methods, a rising share of spending by wealthier households, and the greater influence of respondents’ political affiliation have contributed to the persistent gap. Surveys still capture concerns about prices, jobs and economic uncertainty, while transaction and retail sales data show whether households have changed their behavior. Current results describe cautious consumers who continue to spend, rather than highly confident consumers who spend without restraint.

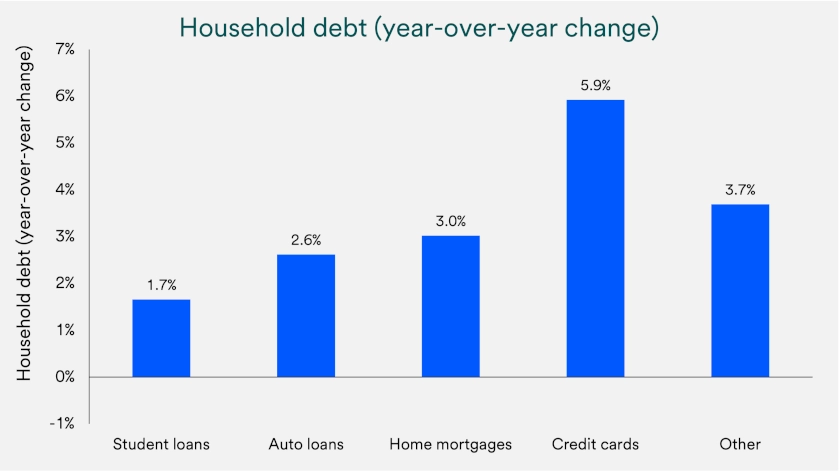

Household debt continues to rise, but growth remains measured. The Federal Reserve Bank of New York reports that total household debt increased 3.3% in the first quarter of 2026 from a year earlier, below the long-term average growth of 4.3%, bringing outstanding balances to $18.8 trillion. 4 The key question for consumer spending is whether required payments begin to crowd out other household expenses.

Credit card balances rose more quickly and stood 5.9% higher than a year earlier in the first quarter. Higher interest rates raise borrowing costs and can pressure households that carry balances from month to month. 6 Income growth provides an important offset, especially for consumers with steady employment and manageable monthly payments.

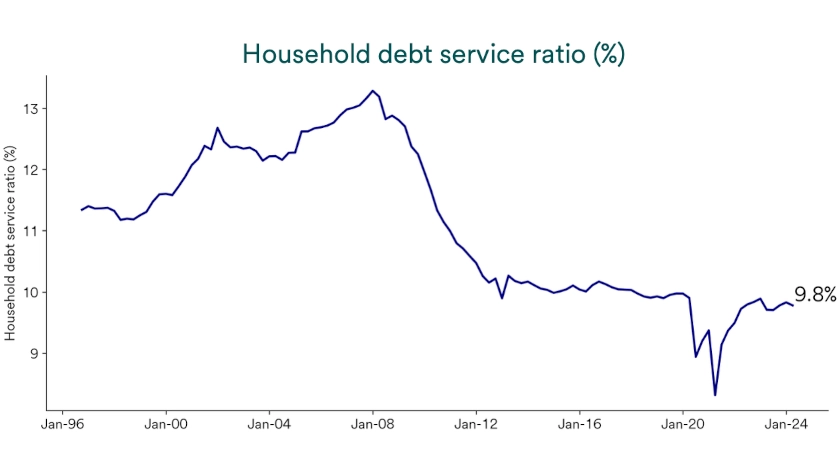

“A key to consumers maintaining healthy balance sheets is that income growth outpaces inflation,” says Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group. Nominal wages continue to exceed the cost of living, even as gains slow for lower‑income households. Wages before adjusting for inflation continue to rise faster than the cost of living, although gains have slowed for lower-income households. Household debt payments equal roughly 11.3% of disposable income, well below the 2007 peak of 15.8%, which suggests many households retain financial flexibility even as higher borrowing costs pressure some consumers. 7

Labor market conditions continue to support consumer spending, although hiring has slowed. Nonfarm payrolls increased by 57,000 jobs in June, while the unemployment rate changed little at 4.2%. 1 Professional and business services, social assistance and health care added jobs, while leisure and hospitality employment declined by 61,000 after weaker-than-usual seasonal hiring.

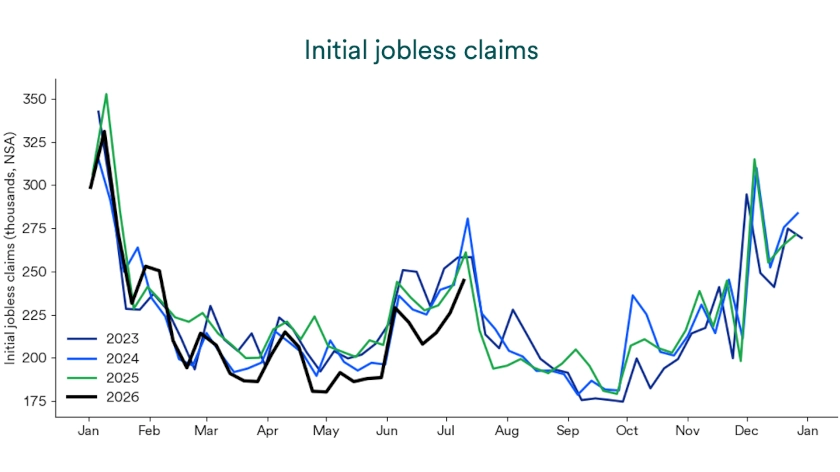

Weekly unemployment claims also point to a relatively stable labor market. Initial jobless claims rose modestly to 244,000 in the week ending July 11, in line with seasonal patterns. 1 Low claims help explain why consumer spending has remained resilient even as payroll growth slows. Employers may hire fewer workers without broadly reducing current staff, but a sustained increase in claims would signal greater pressure on household spending.

Wage growth also continues to support purchasing power. Average hourly earnings rose 3.5% over the past year, helping many households manage higher gasoline prices. 1 “Income growth remains a key stabilizer for consumers as the labor market moves toward better balance,” says Hainlin.

Fed policy will shape the next phase of the consumer cycle. Interest rates influence borrowing costs for mortgages, auto loans, credit cards and other household debt. Recent inflation pressures from energy prices has prompted investors to anticipate that the Fed may raise rates in 2026, which could make consumers more selective even as steady income growth and low layoffs provide support.

Financial markets have started to reflect these competing forces. Broad equity markets entered 2026 on firmer footing even as consumer‑oriented stocks lagged, a pattern consistent with investor expectations for slower but continued growth. Stable consumer spending continues to support corporate revenue despite higher borrowing costs and other financial pressures.

Consumer behavior remains an important variable for investors. Steady spending, low layoffs and ongoing income growth suggest that households can continue supporting economic expansion. Higher energy prices, uneven confidence and pressure on lower-income households, however, support a selective view of companies that depend on discretionary purchases.

For long-term investors, the consumer outlook supports a constructive but disciplined approach. Spending resilience can help extend the economic cycle, although benefits may not flow evenly across sectors, income groups or companies. As Terry Sandven, chief equity strategist for U.S. Bank Asset Management Group, observes, “The durability of the consumer remains a key reason the broader economic outlook stays constructive.”

Consumer spending plays a major role in the U.S. economy, accounting for about two-thirds of total economic activity.1 What households buy each day helps shape the pace of economic growth. When consumers spend, that money supports business sales, helps companies maintain jobs, and encourages investment in inventory, equipment, and services. Those dollars then continue moving through the economy as workers and business owners spend their income. In that way, strong consumer spending can support broader growth, while weaker spending can slow the economy and, in some cases, contribute to a recession.

The job market is one of the most important forces behind consumer spending. When people feel secure in their income and confident about their finances, they are generally more willing to spend. That confidence often shows up most clearly in optional purchases such as dining out, travel, cars, and home appliances. When economic conditions become more challenging, however, households often grow cautious. Concerns about job stability, rising prices, or slower growth can lead people to delay or reduce spending, especially on purchases that are easier to put off.

Consumer spending often shifts as the economy moves through periods of growth and slowdown. During stronger economic periods, people tend to feel better about their financial outlook and more comfortable spending on travel, cars, and other less essential items. They may also feel more willing to borrow when jobs and income appear stable. During downturns, spending usually changes direction. Households often focus more on everyday needs such as food, medicine, and utility bills, while spending on optional items tends to weaken.

Consumer spending remains one of the clearest signals of economic health because it shows how households are responding to changing conditions in real time. Since the U.S. economy depends heavily on consumer demand, household spending makes up the largest share of economic output. When spending remains steady or rises, the economy is more likely to keep expanding. When spending increases too quickly, it can also add to inflation pressure as demand for certain goods outstrips supply. On the other hand, when households pull back, economic growth often slows and the risk of recession can increase.

As always, investors should work with their wealth planning professional to ensure portfolios align with both current economic conditions and long‑term financial goals.

Consumer spending matters because it makes up approximately two‑thirds of U.S. economic activity and often drives short‑term economic growth. 1 It includes everyday purchases of goods and services, and government agencies track it closely as a key part of gross domestic product and as an early gauge of economic strength. When consumer spending holds up, it supports business revenue and hiring, which can help the economy keep expanding.

Retail sales trends suggest consumer demand remains steady overall. The Census Bureau’s retail and food services sales data rose 0.2% month‑to‑month in June while still running higher than a year earlier, which points to continued spending even as momentum cools. 2 Taken together, the data suggests households are shifting where they spend rather than stepping away from spending altogether.

Rising household debt can be a risk to consumer spending, but the impact depends on whether payments strain monthly budgets. Recent Federal Reserve Bank of New York data shows household debt rose modestly in late 2025, with credit card balances increasing alongside other categories. 4 Even so, broader measures that compare debt with income have remained relatively low by historical standards, which suggests many households still have capacity before debt becomes a widespread spending constraint.

Growth slowed late last year as the government shutdown weighed on activity, while consumer spending, hiring and income trends remained broadly supportive.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.