Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

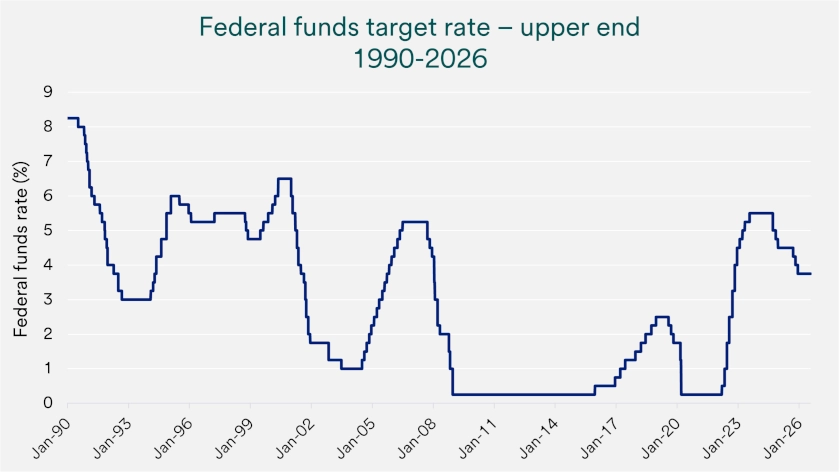

The Federal Reserve (Fed) held rates at 3.50% to 3.75% as the labor market remained consistent with maximum employment and inflation stayed above the Federal Reserve’s 2% target.

Core inflation and the Iran conflict’s energy-price shock shifted market expectations from 2026 rate cuts toward possible rate hikes.

Fed asset purchases support market liquidity, while diversified portfolios can help investors navigate changing inflation, interest-rate and geopolitical risks.

The Federal Reserve (Fed) influences borrowing costs, savings returns and financial conditions across the economy. Congress directs the Fed to pursue maximum employment and stable prices, commonly called its dual mandate. At its July 29 meeting, the Federal Open Market Committee (FOMC) kept the federal funds target range at 3.50% to 3.75%, an outcome investors generally expected.

The federal funds rate is the short-term rate banks use when lending reserves to one another overnight. Changes in that rate can influence mortgages, credit cards, business loans, savings yields and bond markets. The Fed adjusts policy when employment or inflation moves away from its goals, but the two sides of its mandate can point toward different decisions.

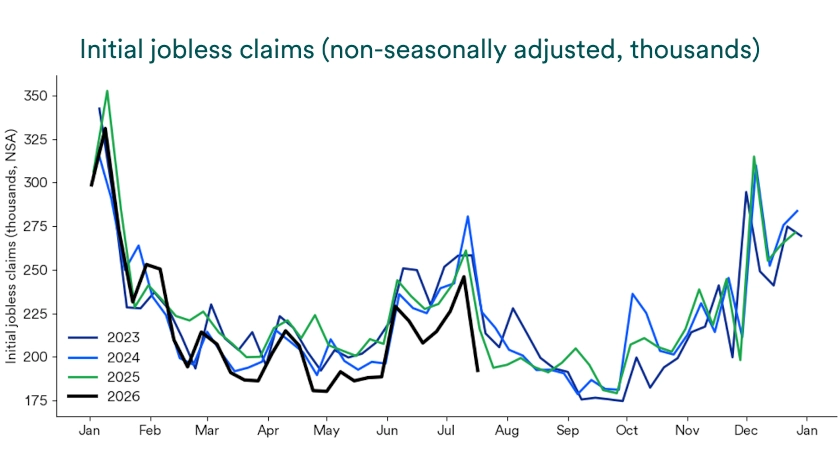

Current labor data indicate that the economy remains near maximum employment. The unemployment rate stood at 4.2%, employers continued to add jobs each month and weekly initial jobless claims remained low. 1 Those conditions reduce the need for the Fed to cut rates to support employment and allow policymakers to concentrate on inflation.

Inflation is creating the harder policy challenge. The core Personal Consumption Expenditures (PCE) Price Index, the Fed’s preferred measure of underlying inflation, has remained above the 2% target since March 2021. 2 Core PCE excludes volatile food and energy prices, which helps policymakers assess whether broad price pressures are easing on a sustained basis.

Recent data have not provided a clear path back to target. Core PCE inflation accelerated from 3.0% in December 2025 to 3.3% in June 2026, extending a period of above-target inflation that began more than five years ago. 2 With employment conditions still firm, persistent core inflation gives the Fed less reason to provide economic support through lower interest rates.

The Iran conflict added a new source of near-term inflation pressure through energy markets. West Texas Intermediate crude oil futures began 2026 near $57 per barrel, reached $113 in April and moved back above $84 during the week of the July Fed meeting after falling from that peak. 3 Higher energy costs can raise transportation and production expenses, then work through to prices paid by households and businesses.

The July vote showed that policymakers agreed inflation required close attention but differed on whether to increase rates immediately. Nine FOMC members supported holding the target range steady, while three preferred a 0.25% increase. Before the meeting, investors assigned a 35% probability to an increase, and markets now anticipate one to two rate hikes by the end of 2026, rather than the rate cuts expected earlier in the year.

Chair Kevin Warsh emphasized that the Fed still defines price stability as 2% inflation, saying, “There’s only a target and it’s 2%.” His message reinforced that policymakers do not view the long stretch of above-target inflation as acceptable. A firm commitment to 2% increases the likelihood that the Fed will keep rates elevated or raise them if inflation remains persistent.

Warsh also pointed to tighter financial conditions as a reason to wait. Market interest rates, including rates adjusted for inflation, had already risen and increased borrowing costs across the economy. That market-driven restraint can slow demand and inflation, giving the Fed time to evaluate incoming data before adding another policy-rate increase.

The Fed’s next steps depend on how inflation and employment evolve together. Continued job gains, low unemployment and limited layoffs would keep the employment side of the mandate near its goal. If core inflation remains above target and energy costs continue to lift prices, policymakers could conclude that higher rates are necessary to restore price stability.

“Markets now lean toward the Fed increasing rates this year, but inflation, oil prices and labor market conditions can shift the outlook.”

Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group

The outlook can change if the labor market weakens or energy prices retreat. A sustained rise in unemployment or jobless claims could increase the cost of tighter policy, while lower oil prices could reduce near-term inflation pressure. “Markets now lean toward the Fed increasing rates this year, but inflation, oil prices and labor market conditions can shift the outlook,” says Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group.

Investors should therefore treat the expected policy path as conditional rather than fixed. The July decision did not settle whether the next move will be an increase, a decrease or another hold. It clarified the decision framework: a labor market near maximum employment allows the Fed to prioritize inflation, while persistent core inflation and the energy shock strengthen the case for restrictive policy.

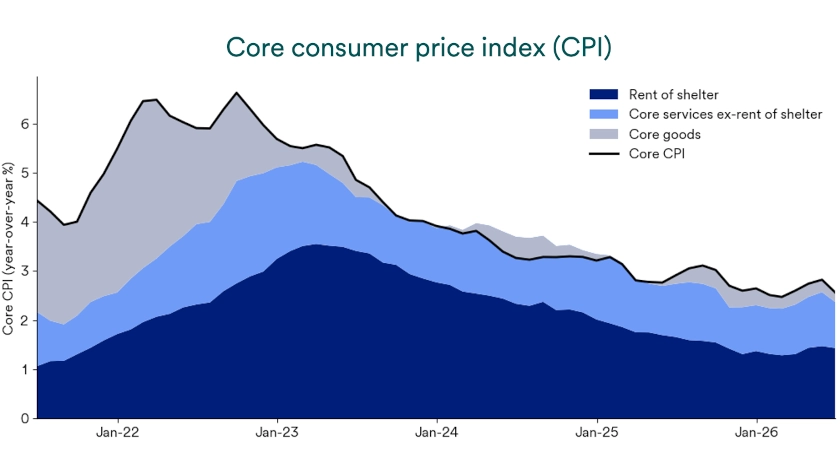

Some areas of inflation may still improve from here. The June Consumer Price Index (CPI) increased 3.5% from a year earlier, while core CPI excluding food and energy rose 2.6%. Shelter costs increased 3.3% over the year, but slower home-price and rent growth may still help cool official inflation readings over time. 1

Housing costs may continue easing with a lag, because rent trends usually move into official inflation data gradually. Slower rent growth can offset some pressure from higher goods, fuel and transportation costs later this year. The inflation backdrop looks far better than it did in 2022, but it looks less predictable than it did earlier this year.

Interest-rate decisions represent only one part of Fed policy. The Fed also influences financial markets through its balance sheet, which includes Treasury securities and other bond holdings. Those holdings stand near $6.6 trillion after peaking near $9 trillion in 2022, and the Fed stopped shrinking the balance sheet in December 2025. 3

The Fed began buying short-term Treasury bills in December 2025 to maintain ample reserves in the banking system and keep overnight rates near its policy target. Treasury bills are short-term U.S. government securities, and Fed purchases absorb part of the supply available to the market. The Fed recently announced that it would reduce regular purchases, but measures of liquidity, or money readily available to buy goods, services and financial assets, remain constructive.

Balance-sheet policy can support orderly financial markets and help the system absorb unexpected shocks. It cannot remove the economic risks created by inflation, higher energy costs or geopolitical conflict. Investors should consider Federal Reserve asset purchases alongside the dual mandate, market interest rates and the broader economic outlook rather than rely on a single policy signal.

The current environment favors discipline over precise forecasts of the Fed’s next move. Consumer spending and corporate earnings remain resilient, while higher energy costs could lift inflation and slow economic activity. A range of plausible outcomes makes portfolio construction more useful than attempting to time each policy decision.

Diversification can broaden potential return sources when inflation, interest rates and geopolitical risks move together. A portfolio that combines globally diversified stocks, global infrastructure, bonds and other income-oriented assets may respond differently across economic scenarios, although diversification does not guarantee returns or protect against losses. Investors can review whether their mix still reflects their goals, time horizon and tolerance for risk with a financial professional.

Fed policy will continue to respond to the evidence. Strong employment conditions and persistent inflation currently support a restrictive stance, while future labor, inflation and energy data can change the outlook. A long-term plan can help investors stay anchored when short-term headlines move faster than long-term fundamentals.

A nation’s central bank, which in the United States is the Federal Reserve, typically controls monetary policy. The Fed’s management of monetary policy can have a significant impact on the shape of the nation’s economy. Congress’ mandate for the Fed is to maintain price stability (manage inflation); promote maximum sustainable employment (low unemployment); and provide for moderate, long-term interest rates. Fed monetary policy influences the cost of many forms of consumer debt such as mortgages, credit cards and automobile loans.

The Fed is the nation’s central bank, and perhaps the most influential financial institution in the world. The central governing board of the Federal Reserve reports to Congress, while the President appoints the chair of the Federal Reserve. There are also 12 regional Federal Reserve banks that are set up like private corporations.

The Federal Reserve’s Federal Open Market Committee sets a target interest rate policy for the federal funds rate. This is the rate at which commercial banks borrow and lend excess reserves to other banks on an overnight basis. The Fed raises or lowers the rate to impact underlying economic conditions. For example, in 2022, as inflation surged, the FOMC began raising interest rates to make borrowing more expensive and slow economic activity. The Fed designed that strategy to ease pricing pressures and reduce the inflation rate. In periods when the economy is slow or in a recession, the Fed tends to lower rates to try to stimulate economic activity and help the economy expand again.

The Fed kept the federal funds target range at 3.50% to 3.75%. Nine FOMC members supported the decision, while three preferred a 0.25% increase. Policymakers balanced a labor market near maximum employment against core inflation above the 2% target and additional pressure from higher energy prices. 1

Core PCE excludes food and energy to help identify underlying inflation, but the Fed evaluates the full economic effect of an energy shock. Higher oil prices can increase transportation and production costs and influence a wider range of consumer prices. Core PCE has also remained above the Fed’s 2% target since March 2021, so the energy shock adds to an existing inflation challenge rather than creating it alone.

Markets shifted from expecting rate cuts earlier in 2026 to anticipating one or two rate hikes by year-end after inflation remained elevated and energy prices rose. That expectation can change as new inflation, employment and oil-price data arrive. The Fed can hold, raise or lower rates based on how those indicators affect its maximum-employment and stable-price goals.

The Federal Reserve held its target federal funds interest rate in the 3.50%-3.75% range at its July meeting, a decision broadly anticipated by investors.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.