Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Interest rates affect bonds by moving prices and yields in opposite directions; higher starting yields can improve bond income.

Federal Reserve policy, inflation, economic growth and Treasury supply will shape the 2026 bond market outlook.

A diversified bond portfolio can balance income, interest-rate risk, credit quality, liquidity and an investor’s time horizon.

Bonds can strengthen a diversified portfolio by providing income, preserving capital and helping offset stock market volatility. Today’s higher yields give investors a better opportunity to earn meaningful income than they had for much of the past decade. Investors can look beyond U.S. Treasuries, but each bond sector brings a different mix of credit risk, trading flexibility and sensitivity to changing interest rates.

A strong bond allocation starts with a purpose, not a prediction about the Federal Reserve’s next move. Income needs, time horizon and risk tolerance should determine how much exposure an investor takes to interest-rate changes and the possibility that a borrower may miss payments. When bond holdings support the broader financial plan, they can provide income and diversification even as market expectations shift.

Federal Reserve (Fed) policy has the greatest direct influence on short-term interest rates because the Fed sets a target for overnight bank lending. Longer-term Treasury yields respond to a wider mix of forces, including expected inflation, economic growth, federal borrowing and investor demand. Those different drivers can push short-term and long-term bond yields in different directions during the same market cycle.

Bond prices and bond yields usually move in opposite directions. When market yields rise, existing bonds with lower fixed payments become less attractive, so their prices generally fall. When yields decline, existing bonds that pay more interest can gain value because investors may pay a higher price for that income.

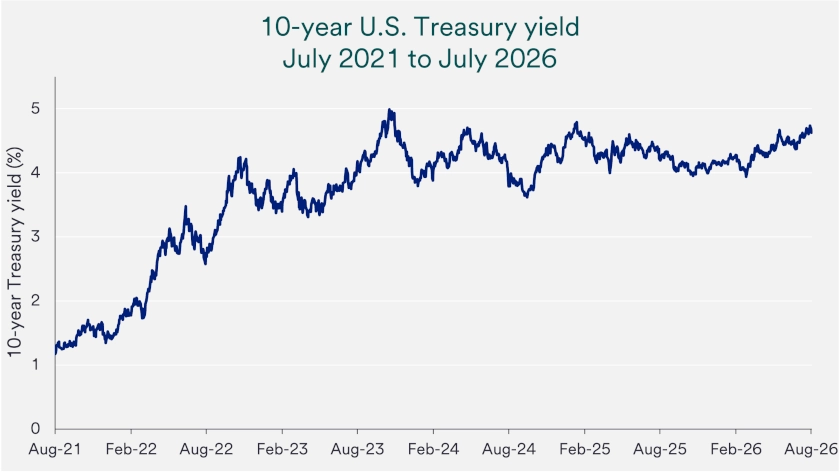

Higher starting yields can improve a bond portfolio’s long-term income potential even when prices fluctuate from day to day. At the July 31, 2026 market close, the 10-year U.S. Treasury yielded 4.71%, placing it near the upper end of its recent range. 1 Investors should still match maturities to their spending needs because longer-term bonds usually experience larger price changes when rates move.

Higher yields can make bonds more attractive, but yield alone does not measure value. Investors should compare the additional income with credit quality, maturity and liquidity, which describes how easily a bond can trade near its market value. A goal-based approach helps investors avoid taking risks that offer too little compensation.

Diversification can reduce dependence on a single interest-rate outcome. High-quality government and corporate bonds may emphasize stability and income, while lower-rated or less liquid holdings may offer more yield in exchange for greater risk. The appropriate mix should support cashflow needs, tax considerations and an investor’s comfort with price swings.

Fed policy, economic growth, inflation, Treasury issuance and investor demand all shape bond market returns. “Federal Reserve rate cuts pulled short-term bond yields lower last year, but shifting expectations for steady or higher future policy rates pushed short-term yields higher in recent months,” says Bill Merz, head of capital markets research for U.S. Bank Asset Management Group. He adds, “The combination of changing policy expectations, sticky inflation and stable growth expectations moved 10-year Treasury yields near the high end of their recent range.”

“Federal Reserve rate cuts pulled short-term bond yields lower last year, but shifting expectations for steady or higher future policy rates pushed short-term yields higher in recent months.”

Bill Merz, head of capital markets research for U.S. Bank Asset Management Group

Inflation remains central to the bond market outlook because investors want income that can keep pace with rising prices. Core Personal Consumption Expenditures inflation, the Fed’s preferred measure of underlying price pressure, increased from 3.0% in December 2025 to 3.3% in June 2026. Higher energy costs can also raise transportation, production and consumer prices, making progress toward the Fed’s 2% inflation goal slower and less predictable.

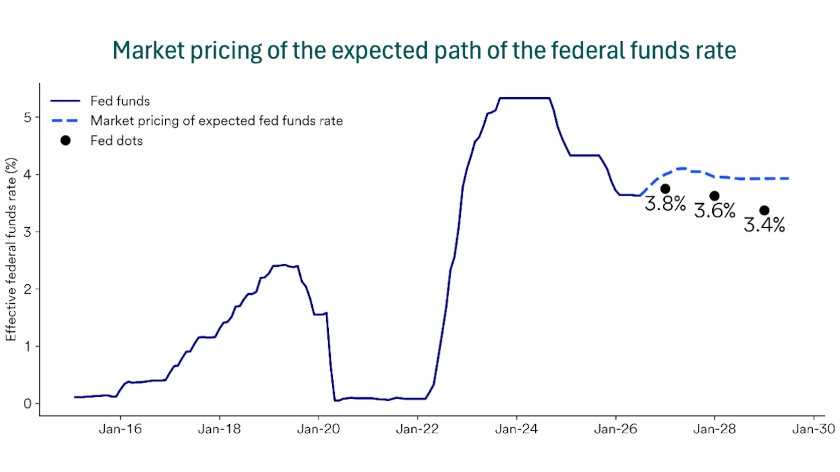

At its July 29 meeting, the Federal Open Market Committee kept the federal funds target range at 3.50% to 3.75%. Nine members supported holding rates steady, while three preferred a 0.25 percentage-point increase. The split vote showed broad concern about inflation but differing views on whether financial conditions are already sufficient to restrain the economy and inflation.

Chair Kevin Warsh reinforced the Fed’s commitment to its 2% inflation target, saying, “There’s only a target and it’s 2%.” Market interest rates had already increased borrowing costs, which gave policymakers time to review new inflation and employment data before raising the policy rate. Bond investors responded by weighing the risk of another increase against the income available at current yields.

Markets now anticipate one or two rate increases by the end of 2026, reversing early 2026 expectations for rate cuts as inflation and energy prices remain elevated. “Markets now lean toward the Fed increasing rates this year, but inflation, oil prices and labor market conditions can shift the outlook,” says Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group. Bond investors can prepare for several outcomes by balancing short-, intermediate- and longer-term maturities instead of relying on one policy forecast.

Federal borrowing also affects bond yields because investors must absorb the Treasury securities issued to finance government spending. A larger supply can lead investors to demand higher yields, especially when inflation or fiscal policy creates added uncertainty. Higher yields may improve income for new buyers, but they can reduce the market value of existing bonds.

“Over the long run, bond buyers want to see federal cash flow support bond principal and interest payments, which would suggest lower spending or higher taxes,” says Bill Merz. If investors doubt that federal revenue will keep pace with borrowing, they may require more income to hold longer-term Treasury debt. That pressure can create opportunity for income-focused investors, but it also supports diversification across maturities and bond sectors.

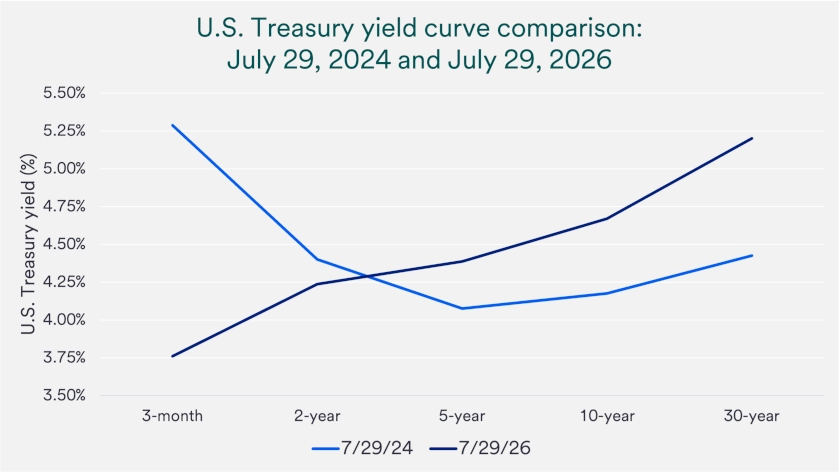

The yield curve compares Treasury yields across different maturities. It has moved toward a more typical upward slope after a long period when short-term yields exceeded many longer-term yields. Investors can now earn somewhat more income for extending maturity, although longer-term bonds still tend to experience larger price swings when interest rates change.

Geopolitical conflict can lift energy prices and renew inflation concerns. Higher fuel costs can spread through transportation, manufacturing and consumer prices even when other inflation measures improve. Investors may then demand higher long-term bond yields to offset the risk that inflation reduces the purchasing power of future interest payments.

Investors can treat fixed income as a toolkit rather than a single bet on the direction of rates. Spreading holdings across maturities and sectors can help balance income, price sensitivity and credit risk while preserving access to cash. Investors should use higher-yielding bonds selectively and give credit quality, liquidity and portfolio objective as much attention as the advertised yield.

Today’s more normal yield curve gives investors an opportunity to reassess bond maturity exposure. Short-term bonds may provide attractive income with smaller day-to-day price changes, while intermediate- and longer-term bonds can add income and may help diversify a portfolio if economic growth slows. The right mix depends on cashflow needs, time horizon, tax profile and how much portfolio volatility an investor can reasonably tolerate.

While rising interest rates offer investors the chance to earn higher yields on fixed income investments, they negatively affect existing bondholders. When interest rates increase, the prices of existing bonds drop. As a result, existing bondholders may see their total returns decrease, depending on how much interest rates rise.

The impact is more significant on those who hold longer-term bonds. Bonds with a longer duration pay a fixed amount of interest regardless of ongoing market trends. Therefore, when interest rates increase, these bonds can decrease in value more sharply. Shorter-term bonds that are maturing sooner experience less price volatility as interest rates fluctuate.

Investors in bond mutual funds should evaluate the fund’s duration as a key factor in understanding the price risk associated with the fund’s fixed income holdings. Conversely, if interest rates fall, longer-term bonds tend to be much more appealing and can increase in value more significantly than shorter-term bonds.

Bond yields mirror the market’s interest rate expectations. When yields rise, it signals that markets expect higher interest rates which could reflect a Federal Reserve (Fed) increase in the federal funds rate, or higher inflation or economic growth expectations. Conversely, when bond yields fall, it indicates anticipation of upcoming Fed rate cuts or slower growth and inflation.

Today’s bond market offers real opportunity, but it does not eliminate tradeoffs. Attractive yields give income-focused investors more room than they have had in years, yet policy uncertainty, inflation risk, and fiscal pressure still support a balanced approach. Investors who spread exposure thoughtfully and keep fixed income aligned with broader portfolio goals can improve their chances of earning durable income without taking uncompensated risk.

Talk to your wealth professional for more information about how to position your fixed income investments consistent with your goals, investment time horizon, risk tolerance and tax profile. A conversation can help translate rate headlines into practical choices about maturity, credit quality, and diversification.

Investments in fixed income securities are subject to various risks, including changes in interest rates, credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Investment in fixed income securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term securities. Investments in lower-rated and non-rated securities present a greater risk of loss to principal and interest than higher-rated securities.

The municipal bond market is volatile and can be significantly affected by adverse tax, legislative or political changes and the financial condition of the issues of municipal securities. Interest rate increases can cause the price of a bond to decrease. Income on municipal bonds is generally free from federal taxes but may be subject to the federal alternative minimum tax (AMT), state and local taxes.

Bond yields change as investors react to economic growth, inflation trends, and Federal Reserve policy decisions. When inflation looks higher or the Fed signals tighter policy, investors often demand higher yields to hold bonds. When inflation cools or growth slows, yields can fall as investors accept a lower return in exchange for stability.

Bond prices and interest rates typically move in opposite directions. When rates rise, existing bonds with lower interest payments become less attractive, so their prices often fall; when rates fall, those existing bonds can rise in value. If you hold a bond to maturity, you generally get face value back (assuming no default), but the market price can fluctuate along the way.

Higher yields can improve the income a bond portfolio generates and raise the starting point for longer-term returns compared with low-yield periods. However, bonds can still help diversify a portfolio and support steadier cash flow even when rates are lower. Many investors focus less on timing and more on building a bond mix that matches their time horizon and comfort with price swings.

The U.S. Treasury market continues to reflect the interplay between monetary and fiscal policy, along with inflation and growth trends.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.