Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

July 1, 2026

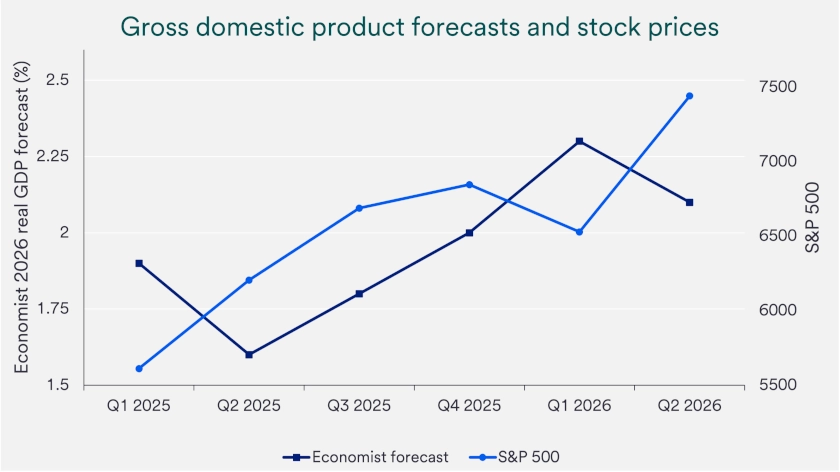

The third quarter begins with a familiar but evolving backdrop. Markets have absorbed meaningful uncertainty this year, yet the core growth supports remain in place: Consumers are still spending, businesses are still investing and growing earnings, and companies continue to build the infrastructure needed for a more data-driven economy. That combination gives investors reasons to stay engaged, even as risks remain active.

The U.S. economy enters the quarter from a position of resilience. Labor conditions remain steady enough to support consumer spending, while earlier income gains still provide some cushion against higher prices. Business investment offers another source of strength; artificial intelligence (AI)-related spending is broadening beyond large technology companies into systems, energy and industrial capacity needed to support long-term productivity.

The Iran conflict is still one of the more fluid risks for markets. Diplomacy has improved and shipping activity through the Strait of Hormuz has started to recover, but the reopening remains fragile and renewed disruption could quickly rebuild pressure on energy prices, shipping costs and inflation expectations. The conflict also reinforces an important distinction: The U.S. is in a better position than many energy-importing regions, but no economy is fully insulated from sharp increases in energy and transportation costs.

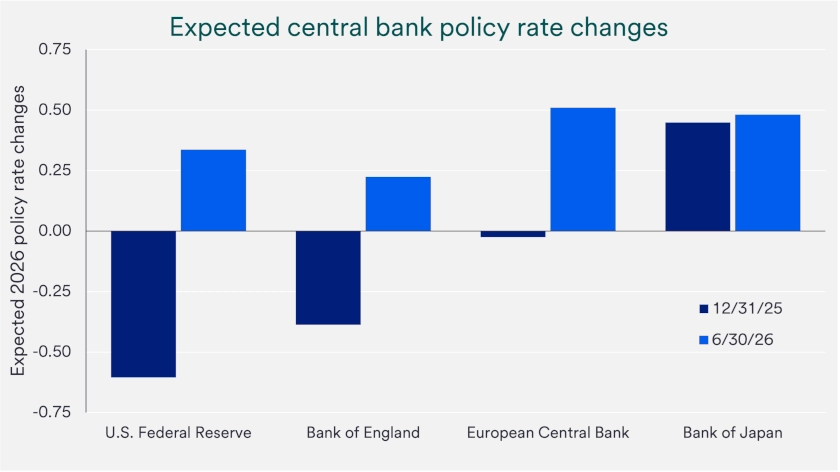

Federal Reserve (Fed) policy has entered a new chapter as well. At Kevin Warsh’s first meeting as chair, the Fed held rates steady while signaling a renewed focus on price stability, shorter communication and a broader review of how it sets and explains policy. Markets now price at least one 0.25% interest rate hike by year-end. Investors are also watching U.S. fiscal health, since debt and interest costs can influence Treasury demand, borrowing costs and market confidence.

Beyond the policy backdrop, 2026 still carries a distinctive calendar. The World Cup is underway, the United States celebrates its 250th anniversary and November midterm elections add another variable for policy and investor sentiment. Private markets are drawing renewed attention as the public listing pipeline reopens, including potential offerings from Anthropic and OpenAI by year-end. Investment opportunities remain, but they are unlikely to appear evenly across asset classes, sectors or regions. Strong earnings still support stocks, higher starting yields keep bonds relevant, real assets can help diversify inflation-sensitive portfolios, and alternative investments and private capital continue to reward selectivity. We are constructive about the opportunities ahead, while staying attentive to risks when growth, policy, geopolitics and fiscal priorities move at once.

Daniel Farley, CFA

Chief Investment Officer

Kaush Amin, CFA

Head of Private Market Investing

Chad Burlingame, CFA, CAIA

Head of Impact Investments

Thomas Hainlin, CFA

National Investment Strategist

Robert Haworth, CFA

Senior Investment Strategy Director

William Merz, CFA

Head of Capital Markets Research

William Northey, CFA

Senior Investment Director

Terry Sandven

Chief Equity Strategist

Quick take: Consumer and business spending should keep the U.S. economy expanding, while inflation, energy costs and policy uncertainty remain the main risks. The global backdrop still looks constructive, but less even across regions.

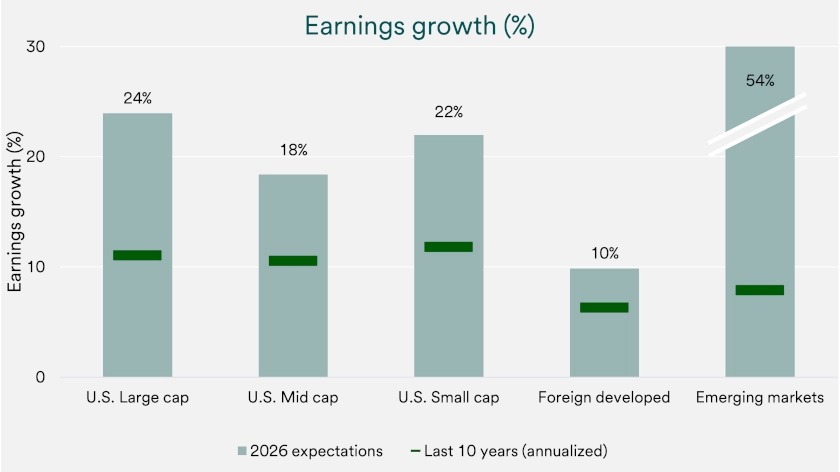

Quick take: Stocks enter the third quarter with earnings support, broader participation and continued technology investment. Elevated valuations and uneven consumer trends keep selectivity important across company size, sector and region.

Quick take: Bonds offer meaningful income, although prices may move as investors assess inflation and Federal Reserve policy. Selective income opportunities are attractive when paired with careful risk control.

Quick take: Real assets can help diversify portfolios when inflation and energy risks rise. Public real estate and infrastructure offer income potential, while commodities are useful but more volatile.

Quick take: We prefer to be selective in private capital as public listings reopen and private credit faces redemption pressure. Long-term themes look attractive when supported by strong underwriting, patience and appropriate fund structures.

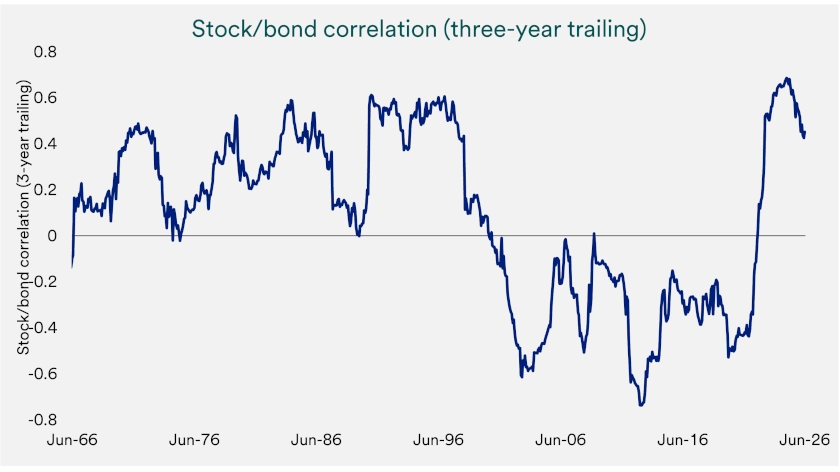

Quick take: Hedge funds may benefit from a market with wider performance gaps across sectors and companies. Flexibility, careful risk-taking and manager selection remain central to their role in portfolios.

This commentary was prepared June 2026 and represents the opinion of U.S. Bank. The views are subject to change at any time based on market or other conditions and are not intended to be a forecast of future events or guarantee of future results and are not intended to provide specific advice or to be construed as an offering of securities or recommendation to invest. Not for use as a primary basis of investment decisions. Not to be construed to meet the needs of any particular investor. Not a representation or solicitation or an offer to sell/buy any security. Investors should consult with their investment professional for advice concerning their particular situation. The factual information provided has been obtained from sources believed to be reliable but is not guaranteed as to accuracy or completeness. Any organizations mentioned in this commentary are not affiliated or associated with U.S. Bank in any way.

U.S. Bank and its representatives do not provide tax or legal advice. Your tax and financial situation is unique. You should consult your tax and/or legal advisor for advice and information concerning your particular situation.

Diversification and asset allocation do not guarantee returns or protect against losses. Based on our strategic approach to creating diversified portfolios, guidelines are in place concerning the construction of portfolios and how investments should be allocated to specific asset classes based on client goals, objectives and tolerance for risk. Not all recommended asset classes will be suitable for every portfolio.

Past performance is no guarantee of future results. All performance data, while deemed obtained from reliable sources, are not guaranteed for accuracy. Indexes shown are unmanaged and are not available for investment. The S&P 500 Index is an unmanaged, capitalization-weighted index of 500 widely traded stocks that are considered to represent the performance of the stock market in general.

Equity securities are subject to stock market fluctuations that occur in response to economic and business developments. International investing involves special risks, including foreign taxation, currency risks, risks associated with possible difference in financial standards and other risks associated with future political and economic developments. Investing in emerging markets may involve greater risks than investing in more developed countries. In addition, concentration of investments in a single region may result in greater volatility. Investing in fixed income securities is subject to various risks, including changes in interest rates, credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Investments in debt securities typically decrease in value when interest rates rise. The risk is usually greater for longer-term debt securities. Investments in lower-rated and non-rated securities present a greater risk of loss to principal and interest than higher-rated securities. Investments in high yield bonds offer the potential for high current income and attractive total return but involve certain risks. Changes in economic conditions or other circumstances may adversely affect a bond issuer’s ability to make principal and interest payments. The municipal bond market is volatile and can be significantly affected by adverse tax, legislative or political changes and the financial condition of the issuers of municipal securities. Interest rate increases can cause the price of a bond to decrease. Income on municipal bonds is free from federal taxes but may be subject to the federal alternative minimum tax (AMT), state and local taxes. There are special risks associated with investments in real assets such as commodities and real estate securities. For commodities, risks may include market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes and the impact of adverse political or financial factors. Investments in real estate securities can be subject to fluctuations in the value of the underlying properties, the effect of economic conditions on real estate values, changes in interest rates and risks related to renting properties (such as rental defaults). Hedge funds are speculative and involve a high degree of risk. An investment in a hedge fund involves a substantially more complicated set of risk factors than traditional investments in stocks or bonds, including the risks of using derivatives, leverage and short sales, which can magnify potential losses or gains. Restrictions exist on the ability to redeem or transfer interests in a fund. Private capital investment funds are speculative and involve a higher degree of risk. These investments usually involve a substantially more complicated set of investment strategies than traditional investments in stocks or bonds, including the risks of using derivatives, leverage, and short sales, which can magnify potential losses or gains. Always refer to a Fund’s most current offering documents for a more thorough discussion of risks and other specific characteristics associated with investing in private capital and impact investment funds. Reinsurance allocations made to insurance-linked securities (ILS) are financial instruments whose performance is determined by insurance loss events primarily driven by weather-related and other natural catastrophes (such as hurricanes and earthquakes). These events are typically low-frequency but high-severity occurrences. Private equity investments provide investors and funds the potential to invest directly into private companies or participate in buyouts of public companies that result in a delisting of the public equity. Investors considering an investment in private equity must be fully aware that these investments are illiquid by nature, typically represent a long-term binding commitment and are not readily marketable. The valuation procedures for these holdings are often subjective in nature. Private debt investments may be either direct or indirect and are subject to significant risks, including the possibility of default, limited liquidity and the infrequent availability of independent credit ratings for private companies.

Includes AI-generated performers.

©2026 U.S. Bancorp

Knowing your investment goals and risk tolerance helps us diversify your portfolio with a mix of equities, bonds and real assets.

New year, updated tax rules. Review adjustments to tax brackets, deductions and retirement contributions to help inform your tax planning.

After a dip in April, the S&P 500 and other major stock market indices continue to rally, hitting historic highs.