Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Market volatility can be caused by unexpected economic news, changes in Federal Reserve monetary policy and global events, among other factors.

Having a financial plan in place, re-examining your risk tolerance and maintaining an appropriately diversified portfolio can help you prepare for and better weather market volatility.

A financial professional can help you adjust your plan to protect your assets and capitalize on new opportunities.

If history is a guide, there will always be periods of market volatility, with dramatic swings both up and down. While not uncommon, these times can be anxiety-producing for investors. Your portfolio may be negatively affected, and you may consider changing your financial strategy.

Understanding what causes market volatility may help you better manage the emotions and behaviors that come with it. Let’s explore market volatility and what can help you ride the waves, such as a comprehensive financial plan.

Stock markets sometimes experience sharp and unpredictable price movements, either down or up. These movements are often referred to as a “volatile market” and can occur over a period of days, weeks or months.

The first thing to know is that volatile markets tend to be temporary. The second thing is that they’re not all bad: A market decline can be an opportunity for investors to find good value in specific investments that experience a temporary drop.

While the term “volatility” applies to both up and down market movements, investors tend to be more concerned about downside volatility. There are two main kinds of downside volatility:

While market volatility can happen with little warning, it rarely occurs for no reason. Factors that can cause market volatility include:

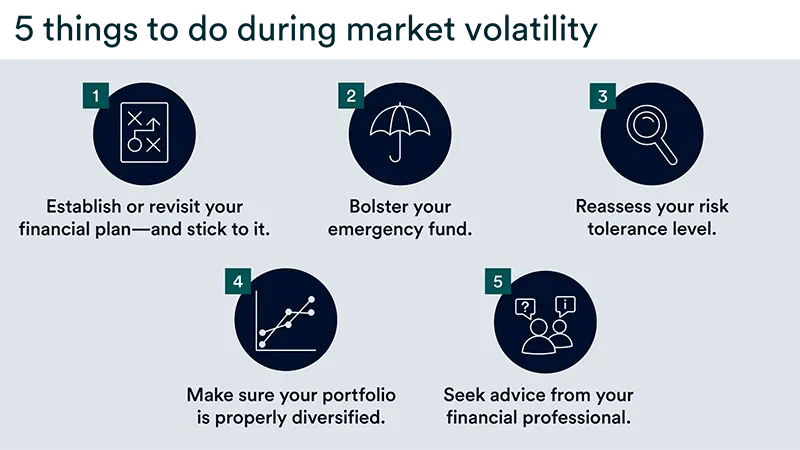

As previously covered, market volatility is temporary, so it’s important to remain calm if your portfolio is affected. But there are also steps you can take to help you better prepare for market turbulence.

A financial plan is the foundation of investing. Sticking with a plan helps you avoid the urge to move money in and out of the market in reaction to price changes.

As you create or review your plan:

You should expect volatility from time-to-time but remember that these tend to be temporary stages in the markets. In fact, a market decline can provide investors a good value in specific investments that experience a temporary drop.

Your emergency cash savings serve as a financial cushion during difficult times or to help you meet unexpected expenses. The conventional wisdom is that you should have the equivalent of three to six months’ worth of income readily available.

If your income fluctuates in economically challenging periods or due to the nature of your work, consider bumping up your emergency fund to meet expenses for six to nine months or more . It will provide peace of mind that you can get through challenging periods.

Your risk tolerance is one of the pillars of your investment strategy. From time to time, reexamine your views on investment risk.

A diversified portfolio that better weathers market volatility begins with owning an appropriate mix of investments aligned with your risk tolerance level. The mix of assets you hold should represent three broad investment categories: stocks, bonds and cash.

For those who still have a sense of caution about the stock market, a dollar-cost averaging strategy can be an effective way to help mitigate the risk of short-term market volatility when you put money to work in assets that can fluctuate in value.

Reassess your portfolio at least annually. And as your portfolio rises or falls in value due to varied investment performance, you may want to rebalance it to make sure it’s still aligned with your primary objectives.

Investors should always be prepared for market volatility. An experienced financial professional can review your current plan or guide you through the process of developing a plan to help you feel confident that you’re on track to your financial goals.

Even if you’re currently comfortable with your plan and investment portfolio, the economic environment can change quickly. A financial professional can help assess your circumstances and calibrate your plan as necessary to either help protect your financial position or take advantage of new market opportunities.

Volatility essentially measures the degree to which the price of an investment changes. Generally speaking, bonds are considered less volatile than stocks, though bonds can also experience price volatility, as bond prices can rise or fall during periods of interest rate changes. Different types of stocks or stock asset classes can also demonstrate different levels of price volatility.

Stock markets tend to be subject to less price volatility when the underlying economy is fairly stable. That often occurs during times of steady economic growth and modest inflation. Stock prices are ultimately a measure of the strength of a company’s earnings (profits). If earnings are growing steadily due to a favorable economic environment, markets tend to encounter fewer periods of volatility. Markets are prone to increasing volatility if a more unpredictable economic environment occurs or unexpected events develop.

Your financial goals are the foundation of your financial plan. Learn about our goals-focused approach to wealth planning.