Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Cash and cash equivalents can provide liquidity, portfolio stability and emergency funds.

Cash equivalent securities include savings, checking and money market accounts, and short-term investments.

A general rule of thumb is that cash and cash equivalents should comprise between 2% and 10% of your portfolio.

There’s a proper role for cash in any asset mix. It’s always important to have cash on hand to meet emergency needs or to fund short-term opportunities. Cash can also play an important role in long-term financial planning. However, it’s just as important to be cautious about holding too much cash.

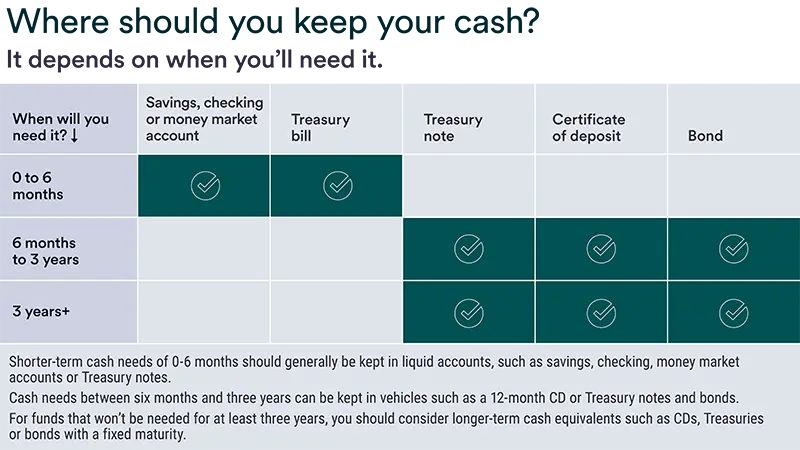

Cash equivalent vehicles are typically defined as savings, checking and money market accounts, as well as short-term investments with maturities less than 90 days, such as CDs, bonds and treasuries.

Cash serves different purposes depending on the objective. A general rule of thumb is to maintain at least 3-6 months of income in cash for emergencies or to cover near-term spending plans. However, another perspective is needed within a long-term investment portfolio.

For example, cash provides retirees with peace of mind that they have sufficient liquid reserves to weather periods of uncertainty or an economic downturn. A portion of a retirement portfolio can be directed to cash equivalents to help meet income needs over a 2- or 3-year period. Those funds won’t be subject to equity or bond market fluctuation.

Investors with years to go before retirement and primarily focused on wealth accumulation have the flexibility to seek higher returns that come with an associated risk. Holding a modest percentage of your portfolio in cash and cash equivalents allows you to quickly take advantage of investment opportunities, particularly at times of market disruptions or fluctuation.

Determining the right cash level for your portfolio is a common question, and the answer varies depending on your unique circumstances and current market conditions.

Some factors that help to determine how much to hold in cash and cash equivalents include:

A general rule of thumb is that cash or cash equivalents should range from 2% to 10% of your portfolio, although this will vary from person to person.

One situation where setting aside extra cash may make sense is if you’re planning on a big purchase or expense within the next few years, such as buying a home, undergoing a major home renovation or paying for college tuition.

On the other hand, you may want to maintain a lower cash position based on your ability to meet short-term cash needs through borrowing. In a low-interest rate environment, for example, you might be able to tap into a home equity loan or line of credit. It avoids the need to set aside extra cash.

Income and net worth are two additional considerations. For example, if you have a steady income and can count on liquidity from a paycheck or annual bonus, a smaller cash position may be appropriate.

If you work as an independent contractor or have a job where your income stream varies, keeping more in cash reserves may be prudent. This can protect you against an unexpected income shortfall or sudden expense.

It can be challenging to find the right balance of cash and cash equivalent holdings. There are pluses and minuses to being overweight or underweight in cash and cash equivalents. As always, your cash position should be informed by your financial goals, risk tolerance and time horizon.

A widely accepted approach is to maintain a cash reserve that’s at least the equivalent of six months of income.

A financial professional can offer guidance on any additional cash you may need to hold based on your financial circumstances, as well as how to ladder it into different types of cash equivalents depending your time horizon and goals.

Laddering cash into short-, mid- and longer-term investment vehicles can be important because it provides liquidity and backup and is a good way to diversify your fixed-income portfolio.

Laddering cash equivalents into short-, mid- and longer-term investment vehicles can be important because it provides liquidity and backup and is a good way to diversify your fixed-income portfolio.

For example, if your child is going to college, you might decide to set aside cash in a checking or money market account to cover the first semester’s tuition, put the second semester’s tuition in a six-month CD, the following year’s tuition savings in a 12-month CD and so on.

You may also wish to consider laddering cash equivalents in fixed-income assets with maturities on a regular basis, allowing them to reinvest and capture yield as rates go up.

You should assess the percentage of cash and cash equivalents in your investment portfolio at least annually, tied to your regular financial plan review. It’s the most effective way to assure that your portfolio is positioned in a way that will help you achieve your financial goals.

Just as your life evolves, so should your financial plan. Learn how we can help you design a plan that fits your life.