Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Downside risk is the chance that an investment or portfolio loses value, especially during short-term market volatility.

Downside risk events can include policy changes, geopolitical developments, interest-rate shifts, economic slowdowns and sudden market disruptions.

Portfolio diversification remains central to downside protection. Investors may consider high-quality bonds, reinsurance, gold and advanced risk-management strategies based on their goals and risk tolerance.

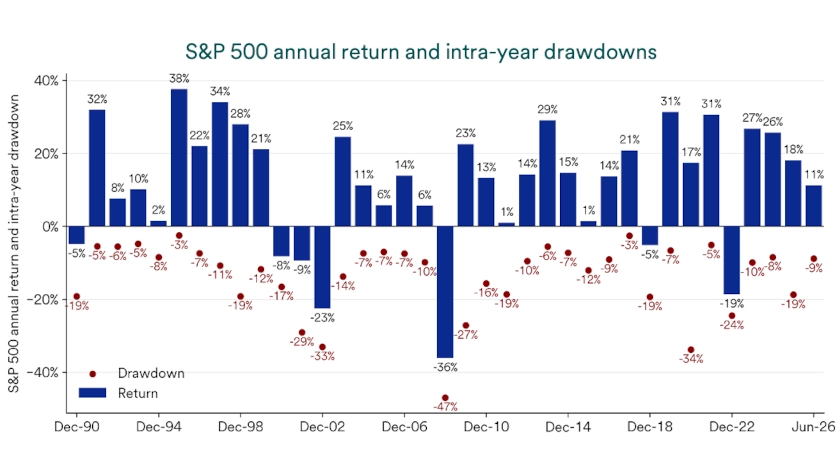

Investors often pay less attention to downside risk when stocks rise and market headlines look favorable. Equity markets have historically moved higher over long periods, but no one can know the next move with certainty. Investors earn long-term return potential by accepting risk, so a thoughtful plan for market declines can help preserve confidence when conditions change.

Markets can shift quickly as policy decisions, geopolitical developments, economic data and investor expectations change. A strong backdrop can become more challenging, and difficult periods can also create opportunities for investors with a clear plan. Understanding downside risk, the events that can trigger it and the investment tactics that may help reduce it can support better long-term decision-making.

Downside risk is the potential for investments to lose value, particularly over shorter periods. Stocks and bonds have generated positive returns over time, but specific events can still cause markets or individual holdings to fall. Higher-returning strategies usually come with wider swings in value, while more conservative strategies often aim to reduce those swings in exchange for lower return potential.

A diversified mix of assets can help reduce downside risk by spreading exposure across investments that may respond differently to market stress.

A diversified mix of assets can help reduce downside risk by spreading exposure across investments that may respond differently to market stress. Diversification does not eliminate losses, but it can help keep one setback from dominating an entire portfolio. Investors should review downside protection during calm markets so the plan already exists before volatility arrives.

A downside risk event occurs when a market, economic or policy development causes investments to decline. These events can affect investor confidence, market valuations or the economic outlook. The COVID-19 pandemic provides a clear example because it disrupted daily life, economic activity and financial markets in a short period.

As schools, workplaces and stores closed in early 2020, the S&P 500 Index lost 19.6% in the first three months of the year. Some investors moved assets out of stocks after the decline, which locked in losses and weakened their long-term strategy. The market then recovered quickly, and the S&P 500 ended 2020 with an 18% gain.

Downside protection means using investment tactics designed to help reduce the impact of short-term market declines. These tactics do not remove risk, and they may not fit every portfolio. Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group, and Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group, outline four approaches investors may consider as part of a broader risk-management strategy.

High-quality bonds can play an important role in a diversified portfolio because they may provide stability when stocks face pressure. Haworth recommends that investors consider an appropriate allocation to high-quality, longer-maturity bonds as part of their broader investment mix. “Making sure you own an appropriate position in high-quality, long-maturity bonds is key,” he says. “Bonds tend to provide stability to a portfolio in periods when equity markets experience volatility.”

The right bond allocation depends on an investor’s goals, time horizon and comfort with market swings. An investor near retirement or with a more conservative risk profile may need a higher bond allocation than an investor with decades before retirement. Bond maturities also matter because a balanced mix of shorter- and longer-term bonds may help portfolios respond more effectively during stock market declines.

“Sometimes people assume they don’t need to own bonds that mature in 10, 20 or 30 years,” Haworth says. “They think they only need a five-year bond portfolio. But we’ve seen that if clients only own bonds that mature sooner rather than later, when the market has down days, portfolio performance lags. Instead, we’d recommend a balanced portfolio that includes a diversified mix of shorter- and longer-term bonds.” Investors should also evaluate bond quality and consider whether lower-quality, higher-yielding bonds add more risk than they want during volatile periods.

Reinsurance works as insurance for insurance companies. It allows an insurance company to transfer part of the risk from large claims, such as those tied to hurricanes or other natural disasters, to another company. “If an insurance company has a policy of insuring against hurricanes, for example, they’re taking on significant risk,” Hainlin explains. “They can choose to offload some of that risk to a reinsurance company.”

Investors can access reinsurance-related securities, which seek returns from premiums paid to take on insurance-related risk. These securities may help diversify a portfolio because hurricanes, earthquakes and other natural disasters do not move in direct alignment with the business cycle, corporate profits or stock market trends. Reinsurance-related securities have tended to generate competitive results, with returns comparable to some equity asset classes and lower annual return variation reflected here in the “annualized volatility” column.

|

Asset Class |

Annualized Return |

Annualized Volatility |

|---|---|---|

|

Large cap stocks |

10.99% |

15.09% |

|

Mid Cap Stocks |

9.47% |

17.58% |

|

Small cap stocks |

8.18% |

20.21% |

|

Reinsurance |

7.90% |

3.79% |

|

High-yield corporate bonds |

6.74% |

9.07% |

|

U.S. REITs |

6.61% |

21.60% |

|

Foreign emerging stocks |

6.32% |

20.34% |

|

Foreign developed stocks |

6.08% |

16.72% |

|

Investment grade corporate bonds |

4.27% |

6.47% |

|

Municipal bonds |

3.52% |

4.78% |

Asset Class

Large cap stocks

Annualized Return

10.99%

Annualized Volatility

15.09%

Asset Class

Mid Cap Stocks

Annualized Return

9.47%

Annualized Volatility

17.58%

Asset Class

Small cap stocks

Annualized Return

8.18%

Annualized Volatility

20.21%

Asset Class

Reinsurance

Annualized Return

7.90%

Annualized Volatility

3.79%

Asset Class

High-yield corporate bonds

Annualized Return

6.74%

Annualized Volatility

9.07%

Asset Class

U.S. REITs

Annualized Return

6.61%

Annualized Volatility

21.60%

Asset Class

Foreign emerging stocks

Annualized Return

6.32%

Annualized Volatility

20.34%

Asset Class

Foreign developed stocks

Annualized Return

6.08%

Annualized Volatility

16.72%

Asset Class

Investment grade corporate bonds

Annualized Return

4.27%

Annualized Volatility

6.47%

Asset Class

Municipal bonds

Annualized Return

3.52%

Annualized Volatility

4.78%

Source: Bloomberg. Past performance is no guarantee of future results.

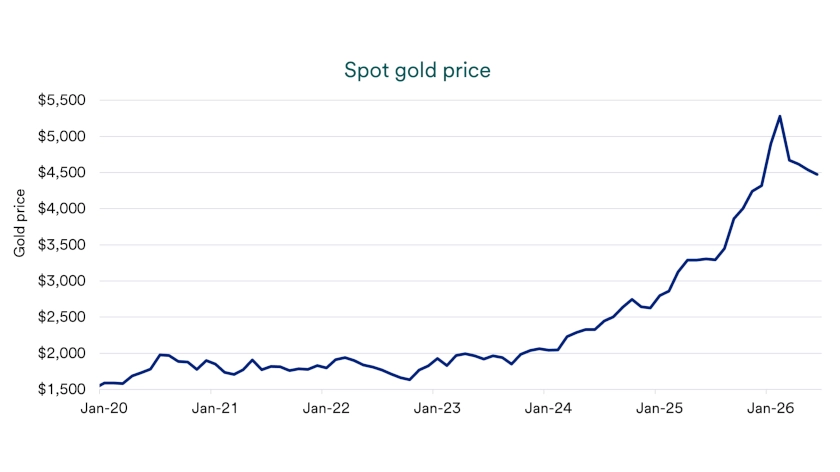

Gold can also support diversification because it often moves differently than stocks. Investors sometimes view gold as a potential safe-haven asset during periods of market stress, geopolitical uncertainty or declining confidence in financial assets. “We’ve seen some scenarios where gold has been a safe-haven asset when things are going poorly in the equity market,” Haworth explains. “It doesn’t always happen, and it’s not always perfect, but if worse comes to worst, having a modest portfolio position in gold can provide protection in those environments.”

Gold does not provide the same consistency as high-quality bonds or reinsurance-related securities, and it can experience meaningful price swings. Haworth and Hainlin both emphasize that bonds and reinsurance have tended to deliver more consistent returns relative to risk than gold. Investors should treat gold as a modest potential diversifier rather than a complete downside protection strategy.

Some investors may want protection beyond changes to their mix of stocks, bonds and diversifying assets. Derivatives and structured products may help certain investors manage stock market exposure without moving an entire portfolio into bonds. These tools require careful review because they can limit losses in some scenarios while also reducing potential gains.

Both derivatives and structured products can help hedge stock investments, but they add complexity and may reduce liquidity. Investors may not be able to sell them quickly or easily, and some products require active monitoring. These strategies generally fit investors who understand the trade-offs and can work closely with an investment professional.

Investors should connect downside protection tactics to their financial goals, time horizon, income needs and comfort with market volatility. Bonds, reinsurance, gold, derivatives and structured products can each serve a role, but none should replace a disciplined long-term plan. A portfolio review can help determine whether current allocations still match the investor’s objectives and risk tolerance.

Haworth adds that investors who manage their own portfolios may benefit from reviewing investments quarterly and considering annual adjustments as markets move and personal circumstances change. A long-term investment strategy tailored to specific goals can provide the foundation for managing downside risk. Tactical adjustments can then help address changing market conditions without letting short-term headlines drive every decision.

Learn about our approach to investment management.