Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

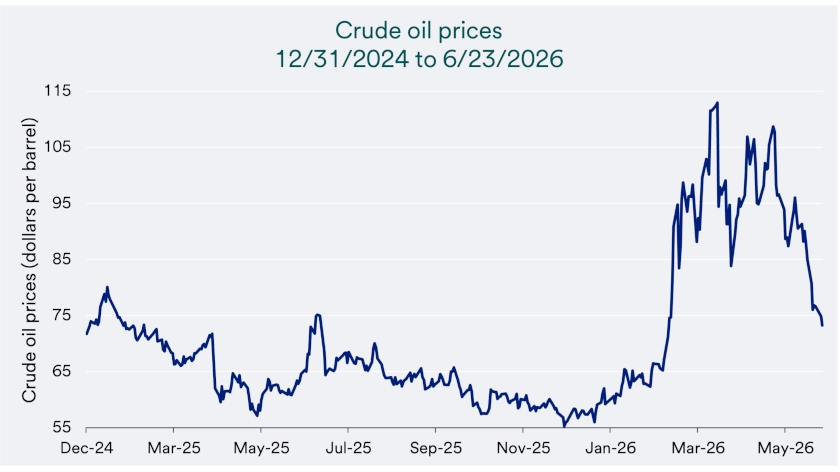

The Iran conflict keeps oil prices tied to Strait of Hormuz shipping, where partial reopening still leaves energy and fertilizer costs, and inflation risks, in focus.

The Russia-Ukraine conflict continues to affect markets through energy flows, trade policy and economic sanctions, even as investors adapt to recurring headlines.

Investors should watch whether supply disruptions persist and keep portfolios aligned with long-term goals.

The Iran conflict and Russia-Ukraine war continue to influence global markets though oil prices, energy shipping routes, and inflation expectations. One of the biggest near-term risks centers on the Strait of Hormuz, a critical corridor for global oil and liquefied natural gas shipments. For investors, the key question is whether these conflicts create lasting supply disruptions or remain shorter-term market shocks.

Iran moved to the center of investor attention after U.S. and Israeli military operations expanded in late February and continued until April 7th, when President Trump announced a two-week ceasefire agreement. Recent negotiations have supported a gradual restart of tanker transit, but shipping traffic through the Strait of Hormuz remains well below pre-conflict levels. The S&P 500 fell 9% below its January peak, while the MSCI EAFE Index of developed international markets and the MSCI Emerging Markets Index declined 8% to 12% before rebounding as investors refocused on resilient consumer spending, strong corporate earnings growth and signs that Gulf energy supplies may begin moving more freely. 1

“Investors are navigating a lot of moving parts in 2026, adding geopolitical conflict to a change in Federal Reserve leadership and midterm elections.”

Terry Sandven, chief equity strategist with U.S. Bank Asset Management Group

International markets have faced more pressure because many economies in Europe and Asia rely more heavily on imported energy. Since the ceasefire announcement, U.S. and emerging market stocks have reached new all-time highs, showing that markets can recover when investors see lower odds of a broader disruption. The rebound also reinforces the importance of investors separating headlines from material changes in economic activity.

Energy markets remain the clearest link between the Iran conflict and global markets because the Strait of Hormuz has few near-term substitutes at scale. The U.S. Energy Information Administration estimates that oil flows through the strait averaged about 20 million barrels per day in 2024, or roughly 20% of global petroleum liquids consumption. The agency also reports that about 20% of global liquefied natural gas trade moved through the same route in 2024, making the corridor especially important for Europe, a major importer after losing access to Russian pipelines of natural gas. 2

The International Energy Agency also describes the Strait of Hormuz as a pivotal chokepoint for seaborne oil trade. That role explains why even the threat of slower shipping can move prices before consumers or businesses experience a physical shortage. When energy prices rise, investors begin to assess whether higher transportation, heating and production costs could last enough to affect inflation, household budgets and corporate profits.

Disruptions can also raise food-price risk by tightening fertilizer supply and increasing farm input costs. The Fertilizer Institute indicates that nearly 50% of the global exports of urea, the most common nitrogen fertilizer, originate from countries west of the strait and typically transit this route. 3 For regions that rely on imported energy and fertilizer, higher costs can work through the economy over time through transportation expenses, food production costs and consumer prices.

Three simplified outcomes help investors frame the range of possible market paths. In a low-impact case, shipping conditions improve quickly, commercial traffic resumes more reliably and energy prices ease as supply concerns fade. In that environment, investors may continue to look through the recent shock as long as broader economic data remain steady.

A mid-impact case would involve an ongoing disruption keeping energy and transport costs elevated and increase the risk of broader economic and market volatility tied to inflation concerns. Markets would likely focus on whether higher energy prices begin to affect consumer spending, business margins or central bank policy expectations.

A high-impact case would involve significant disruption of shipping and regional oil infrastructure, allowing sustained higher energy costs to weigh more directly on consumer spending and business activity. Fertilizer constraints could also extend into the key southern hemisphere growing season, adding pressure to food prices. Across all three outcomes, markets will likely focus less on daily headlines and more on whether shipping and supply conditions normalize or deteriorate.

The fragile reopening supports the view that oil transportation constraints may begin easing in the near term, allowing markets to look through recently elevated energy costs. 4 The truce remains fragile, however, and a durable agreement could still take time to secure. Renewed conflict remains a real risk, which reinforces the value of portfolio discipline rather than rapid shifts based on headlines.

The war between Russia and Ukraine has continued for more than four years following Russia’s invasion of Ukraine, and ceasefire efforts have not produced a comprehensive agreement. The conflict remains relevant for markets because it intersects with trade policy, energy flows, and economic sanctions. Investors have adapted to recurring headlines, but the persistence of the conflict can still shape corporate planning, government priorities, and market risk assessments.

Oil prices surged in the immediate aftermath of Russia’s invasion in early 2022 as western nations moved to impose sanctions on a major energy supplier. That initial price spike proved short-lived, and later geopolitical events also produced sharp moves that did not always persist. 4 This pattern does not reduce the seriousness of the conflict, but it does show how markets often shift from fear to evaluation once investors can better judge the scope of economic disruption.

“Investors are navigating a lot of moving parts in 2026, adding geopolitical conflict to a change in Federal Reserve leadership and midterm elections,” says Terry Sandven, chief equity strategist with U.S. Bank Asset Management Group. “Inflation is kryptonite to stock valuations,” continues Sandven. “If energy prices rise and the price of other goods follow, higher borrowing costs could temper corporate earnings.”

In early January, the United States conducted a large-scale strike against Venezuela that captured President Nicolas Maduro and his wife and brought them to the United States to face criminal charges. Despite the dramatic headlines, markets experienced limited disruption, because investors viewed the engagement as short-lived and contained. The episode remains relevant because changes in governance and policy can affect energy investment and supply over time, even when markets treat the immediate event as temporary.

The broader lesson is that markets often respond most to conflicts that threaten supply routes, production capacity, or infrastructure that cannot be replaced quickly. When an event appears less likely to disrupt near-term supply, market reactions often fade as investors develop a clearer view of the economic impact. This distinction helps explain why energy-linked conflicts can create sharp moves that later reverse when supply remains available and transport routes remain functional.

Recent conflict episodes show that stock prices have often recovered once investors assessed the scope and likely outcomes, while oil prices have sometimes cooled after an initial spike. U.S. stock markets have remained resilient at times, supported by broadly steady economic data and persistently solid consumer spending. Those fundamentals can help anchor markets even when geopolitical headlines create short-term volatility.

Now may be an opportune time to connect with your wealth planning professional to discuss how your portfolio aligns with your goals, time horizon, and comfort with market swings. A thoughtful review can help you decide which risks deserve attention and which headlines deserve less weight in your long-term plan. Such discipline can help prevent short-term headlines from driving long-term missteps.

Geopolitics refer to events that influence the global landscape, including political or trade tensions and military conflicts. Such events often create economic uncertainty, which can lead to fluctuations in stock prices, interest rates, and currencies. Geopolitical conflicts frequently impact supply chains, such as Iran’s threats to halt oil shipments through the Strait of Hormuz. Wars in agricultural regions can also affect crop yields and deliveries. Events like these can cause supply-demand disruptions, resulting in higher prices.

Geopolitical issues aren’t always related to military conflicts. Problems like new trade barriers or the formation of alliances among previously unfriendly nations can also impact markets.

The emergence of new geopolitical conflicts often causes an immediate market reaction, frequently a negative one. If events are seen as disruptive to the global economy, investors may suddenly reduce portfolio risk and pursue a so-called “flight to quality.” This approach often results in a sell-off in stocks, with increased interest in bonds or “safe haven” assets like gold.

It is common for investors to overreact to initial shocks from geopolitical conflicts. Market declines are expected, but history shows that markets usually recover from these early negative impacts caused by major geopolitical events.

Oil prices can move quickly when investors fear disruption to shipping routes near major producers, even before supply is physically interrupted. When energy prices rise, markets may worry about higher inflation and slower growth, which can pressure stock prices in the short run. The impact often depends on whether higher prices persist long enough to influence household budgets and business costs.

The Russia-Ukraine war remains a persistent source of uncertainty because it intersects with trade policy, energy flows, and economic sanctions. Markets have adjusted to the ongoing conflict, but changes in sanctions, negotiations, or energy conditions can still influence prices and confidence. Investors often focus on whether developments change real economic activity or remain primarily a source of headline-driven volatility.

Geopolitical headlines can move markets quickly, but short-term swings do not always translate into lasting changes in the economy. Investors may benefit from reviewing how much risk they are taking and whether their strategy still fits their goals and financial plan. Talking with an advisor can help connect current events to a plan and keep short-term headlines from driving long-term decisions.

Investors are increasingly focused on how the administration’s policy changes are impacting markets and the economy.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.