Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Nearly $8 trillion in money market funds shows much cash remains on the sidelines, but excess cash can slow investors’ progress toward long-term goals.

Federal Reserve policy can quickly change cash yields, reinforcing the value of matching short-term holdings to near-term needs rather than market forecasts.

Align cash with near-term needs and specific goals, then invest remaining long-term assets according to your financial plan and rebalance regularly.

Higher interest rates and uneven markets have encouraged investors to hold sizable balances in cash equivalents and other short-term investments. The Investment Company Institute reported that money market fund assets reached nearly $8 trillion as of July 9, 2026. 1 These investments typically experience limited price movement, but holding too much money on the sidelines can make it harder to reach long-term financial goals.

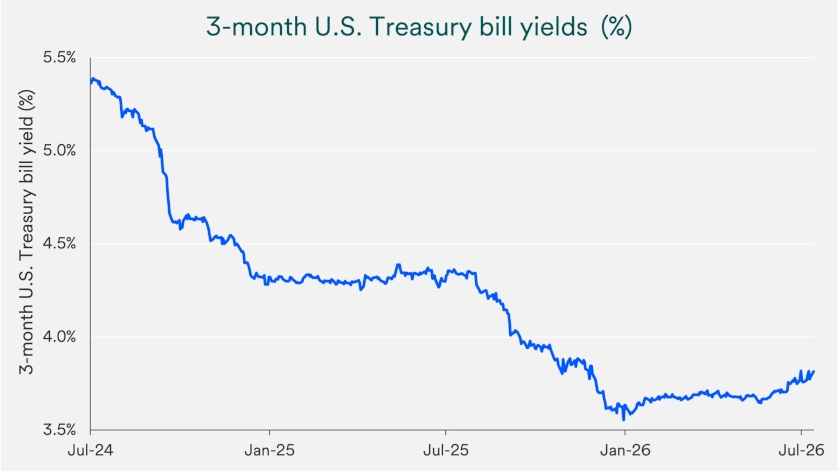

For years, money market accounts, certificates of deposit and U.S. Treasury bills offered yields that attracted little attention. That changed as interest rates rose. Three-month Treasury bill yields exceeded 5.5% in 2023 before moving into a 3.5% to 4.0% range. 2 The Federal Reserve (Fed) drove much of that shift by raising interest rates aggressively in 2022 and 2023, then cutting rates in 2024 and 2025. Cash still offers an appealing combination of liquidity and income, but investors should decide how much they need rather than let a temporary yield determine a long-term strategy.

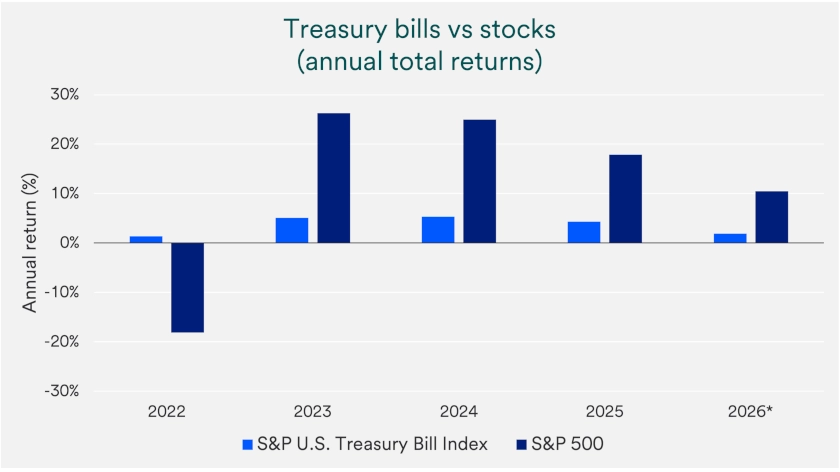

When markets decline sharply, many investors raise cash to reduce exposure to assets whose prices can fluctuate. In 2022, the Fed raised interest rates to slow the economy and curb inflation, while the S&P 500 Index fell 25% over 10 months. 2 That combination reinforced the urge to step away from stocks and pursue a flight to safety or flight to quality.

Cash can provide stability, but it also reduces participation when markets recover. From January 1, 2023, through July 10, 2026, the S&P 500 delivered a total return of more than 107%, far above the return available from cash-like holdings. “While people became comfortable with higher savings yields, over time, they’ll find they are likely better off diversifying into long-term assets such as investment-grade bonds and equities,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group. For investors with a time horizon measured in years rather than months, a diversified portfolio can offer more long-term growth potential than cash alone.

The choice between cash and stocks is not an all-or-nothing decision. Cash can support near-term spending and provide a buffer during periods of market volatility. Stocks and bonds can serve longer-term goals by offering the potential for higher growth and income in exchange for greater uncertainty and price movement.

Investors who leave long-term, investable assets in cash for too long can allow short-term convenience to displace long-term progress. “Investors earn returns from taking on uncertainty or risk,” says Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group. “While short-term returns are not guaranteed, markets typically reward long-term patient investors for lending money to a business or government entity (bonds) or participating in a corporation’s future growth (equities).”

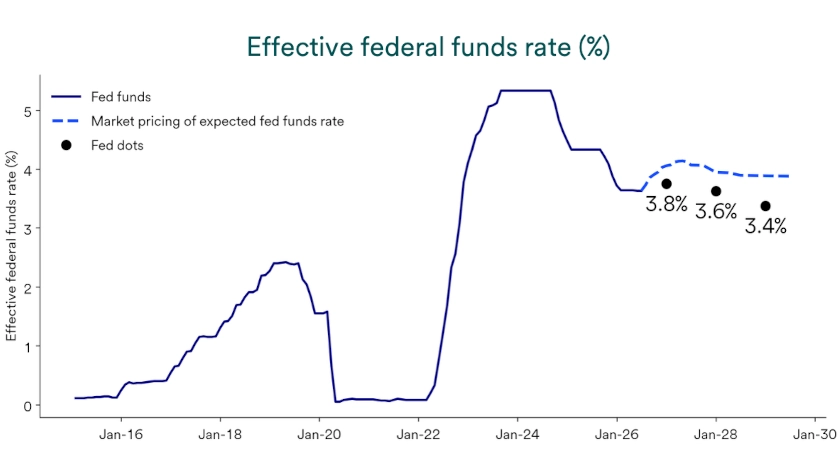

Investors with significant cash positions must focus on where interest rates may go next, not only where they have been. “Investors should be aware that as the Fed lowers interest rates, yields on cash-equivalent instruments fall,” Haworth says. “That results in an even bigger opportunity cost when leaving long-term money tied up in short-term investments.” The Fed cut its fed funds target rate by 1 percentage point in late 2024, followed by three 0.25 percentage-point cuts in 2025.

“Investors should be aware that as the Fed lowers interest rates, yields on cash-equivalent instruments fall. That results in an even bigger opportunity cost when leaving long-term money tied up in short-term investments.”

Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group

Three-month Treasury bill yields generally moved lower after mid-2024. More recently, resilient economic growth and persistent inflation have made investors less confident that the Federal Reserve will cut rates in 2026 and have raised the possibility of a rate increase. 3 Investors should watch inflation, employment and Federal Reserve policy because changes in those conditions can quickly affect yields on cash-equivalent investments.

Trying to identify the perfect time to invest can leave investors waiting indefinitely. “The unknown is always on the horizon and at no point will you be absolutely certain the time is right,” Hainlin says. “That’s why we recommend investing in alignment with your financial plan.” A plan-based approach can reduce reactive decisions that lock in losses or miss a market recovery.

Discipline also requires regular portfolio maintenance. “It’s important to regularly rebalance a portfolio to reflect how market performance has changed your asset mix and restore your intended allocation based on your risk tolerance, time horizon and goals,” Haworth says. Rebalancing brings a portfolio back to its target mix after market movements change the relative size of its investments. This process turns volatility into a planned decision rather than a response to the latest headline.

A practical cash management strategy assigns each dollar a specific purpose. First, reserve enough cash for current expenses and expected cash flow needs over the next year or so. Ready access to money takes priority when bills or planned purchases are close.

Second, set aside money for specific objectives, such as a down payment or another major purchase. Match the investment choice to the timing and importance of the goal. This two-bucket approach can reduce excess “just in case” cash while giving investors greater confidence to invest other assets for the long term.

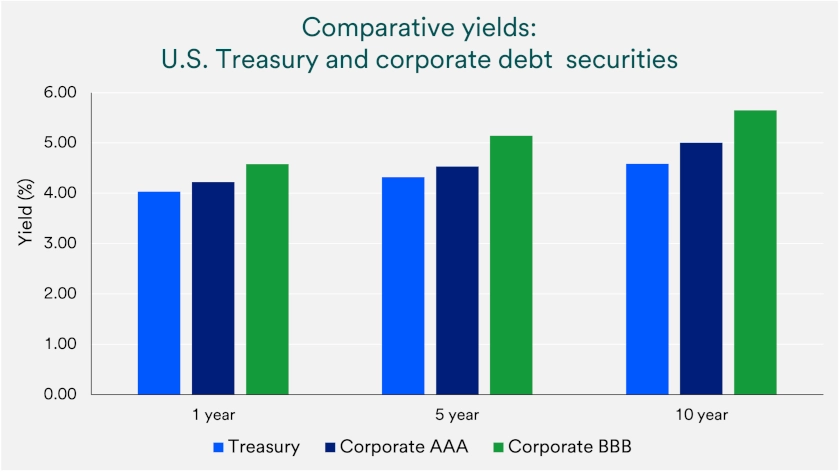

Money that supports a defined goal but does not need to remain fully liquid may fit investments that offer higher yields with modest tradeoffs in access and price stability. Potential choices include money market funds, Treasury bills and short-term bonds. Each option carries different risks, so investors should compare the need for liquidity, principal stability and income before investing.

Determining the proper role for cash in an investment portfolio can be challenging. It’s often a “tug-of-war” between the short-term certainty of cash and the long-term purchasing power that may be achieved through stock or bond investments. Cash can be appealing, particularly in volatile or uncertain times, as it is considered a “risk-free” asset in terms of nominal value. Stocks and bonds are subject to price variations but also typically offer growth in purchasing power that more than offsets inflation over time.

There are several primary roles for cash in an investment portfolio. Some investors hold cash to meet current or near-term expenses. In some circumstances, investors hold cash to temper potential market volatility in their portfolios. In other cases, cash can play a modest role in a long-term portfolio as a diversifier within an equity-heavy asset mix.

Cash as an investment portfolio component provides some benefits but also drawbacks. Among the benefits are protection against market volatility, the security of a stable value, and the flexibility to have liquid assets available to invest or spend as opportunities arise. A key drawback is the loss of purchasing power, as cash returns have historically not kept pace with inflation. Cash is not an effective long-term wealth-creation vehicle.

Three reasons to keep money on the sidelines in cash are liquidity, stability, and optionality. Maintaining a portion of your portfolio in highly liquid assets (i.e., Treasury bills, money market funds) gives you access to cash for unexpected spending. Stability means the principal of your cash investments is preserved. Optionality leaves you in a position to deploy capital in investments or other spending at a later date, in essence, keeping your options open.

Keeping investable money on the sidelines to protect against short-term market volatility can be detrimental in the long run. The opportunity cost of holding cash is the loss of compound interest from stock and bond returns. Because it is difficult to predict when markets generate their largest returns, those trying to “time the market” by holding cash risk missing some of the market’s best days.

A key factor in determining portfolio construction is your investment time horizon. When it comes to cash, that horizon determines whether it serves as a safe harbor or a wealth inhibitor. Money that may be needed in the next two years should be heavily weighted toward cash to maintain liquidity and protect principal value. However, farther out on your time horizon, money should be increasingly allocated to more variable investments such as equities and bonds.

As part of your financial plan, investors should seek the proper balance between cash and investments. Cash plays a role in your plan by meeting near-term liquidity needs and providing some cushion against market volatility in a longer-term investment portfolio. The appropriate allocation to cash is determined on an individual basis, often related to the investor’s age and primary objectives.

The central decision remains straightforward: align cash with near-term needs and invest long-term dollars to support long-term objectives. Review cash balances, portfolio allocations and upcoming spending needs regularly rather than allowing investors’ money to accumulate without a defined purpose. A wealth professional can help coordinate cash investing decisions with a broader financial plan and long-term investment strategy.

Note: The Standard & Poor’s 500 Index (S&P 500) consists of 500 widely traded stocks that are considered to represent the performance of the U.S. stock market in general. The S&P 500 is an unmanaged index of stocks. It is not possible to invest directly in the index. Past performance is no guarantee of future results.

With the stock market up, how should investors position their portfolios to capitalize on potential opportunities, while guarding against risks?

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.

The S&P 500’s recent rollercoaster performance has investors wondering what lies ahead for the stock market.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.