Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

The U.S. job market slowed in June as employers added 57,000 jobs, while unemployment edged down to 4.2%.

Labor market data show steady demand, with 7.6 million job openings and low jobless claims.

Inflation remains the key investment risk shaping Federal Reserve interest rate decisions and investor expectations.

The June jobs report showed a slower U.S. job market, but not a broadly weakening labor market. U.S. employers added 57,000 jobs in June, and the unemployment rate edged down to 4.2%, according to the Bureau of Labor Statistics (BLS). Employment continued to grow in professional and business services, social assistance and healthcare, while leisure and hospitality lost jobs.

The headline numbers looked stable, but the details showed a cooler labor supply picture. The labor force participation rate fell to 61.5%, and the employment-population ratio slipped to 59.0%. Those measures suggest fewer people were working or actively looking for work in June, which can keep unemployment stable even when hiring slows.

June’s payroll gain followed stronger spring hiring, but revisions lowered the recent trend. The BLS revised May payroll growth down to 129,000 from 172,000 and April payroll growth down to 148,000 from 179,000. The latest numbers point to a labor market that is still expanding, though at a more moderate pace than earlier estimates suggested.

The job market remains important for investors because employment and income help drive household spending. When more people work and wages rise, consumers generally have more capacity to spend on goods, services, housing and travel. Consumer spending represents a large share of U.S. economic activity, so even modest changes in hiring can shape the broader growth outlook.

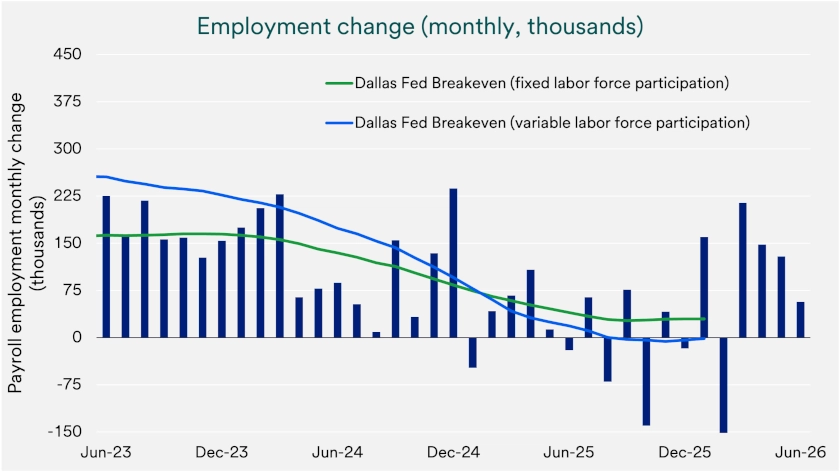

The Federal Reserve Bank of Dallas offers a useful lens for interpreting recent payroll numbers. Its March 31 analysis focuses on “break-even” employment growth, or the monthly job gain needed to keep the unemployment rate steady. The Dallas Fed estimates that this threshold has moved much lower because immigration flows and participation trends have slowed labor force growth.

In practical terms, the economy may not need the same monthly job gains it once needed to keep unemployment stable. The Dallas Fed estimated that break-even job growth peaked near 250,000 per month in 2023, fell to roughly 10,000 by July 2025 and moved near zero later in 2025. Against that backdrop, June’s 57,000 payroll gain looks constructive. 1

Wage growth continues to support household income, but inflation is absorbing part of those gains. Average hourly earnings for all employees rose 3.5% from a year earlier in June, based on the latest employment data. Recent consumer price data showed prices rose 4.2% in May from a year earlier, which means inflation continued to limit how much households benefited from higher pay.

“The June jobs report shows a labor market that is still growing, but in a more selective way. Investors should pay close attention to the mix of hiring, wages and labor supply because those details often tell the real story for the economy and markets.”

Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group

Even with headline inflation outpacing wage growth for many households, higher-frequency consumer spending measures remain solid. Johnson Redbook’s weekly retail sales figure rose more than 10% in the final week of June from the prior year period. Fiserv’s point-of-sale data indicated a nearly 7% increase in same-store sales in June.

“The June jobs report shows a labor market that is still growing, but in a more selective way,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group. “Investors should pay close attention to the mix of hiring, wages and labor supply because those details often tell the real story for the economy and markets.” For consumers, steady employment and rising wages support spending power, while persistent inflation limits the benefit to households of higher pay.

The latest Job Openings and Labor Turnover Survey, known as JOLTS, showed steady labor demand in May. Job openings were unchanged at 7.6 million, hires held at 5.2 million, and total separations changed little at 5.1 million. Job openings measure positions employers want to fill, while hires show how many workers actually started new jobs during the month.

Quits remained at 3.1 million in May, and the quits rate held at 1.9%. Quits offer a useful read on worker confidence because employees usually leave jobs voluntarily when they believe they can find a better opportunity. A low quits rate points to a more cautious labor market, where workers may value job stability more than switching roles for higher pay or career advancement.

Layoffs and discharges were unchanged at 1.7 million in May, with the layoff rate little changed at 1.1%. That data does not suggest broad employer retrenchment, even though hiring has slowed. Taken together, openings, hires, quits and layoffs describe a labor market that is steady but less fluid than the very tight labor market investors saw earlier in the expansion.

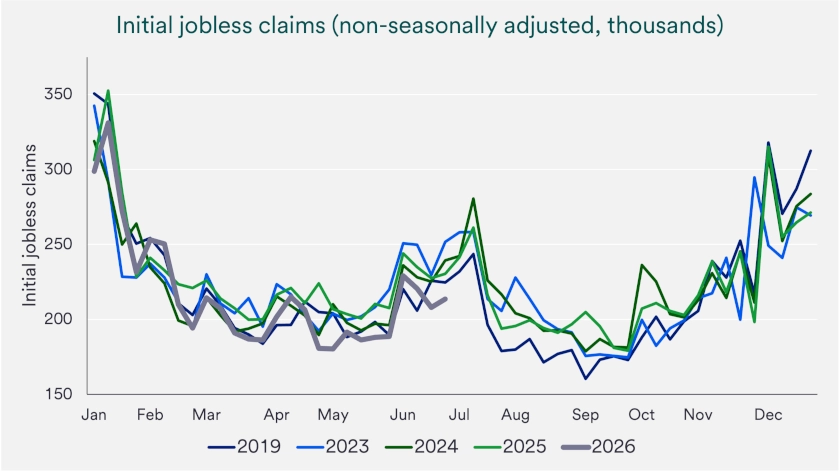

Weekly jobless claims still point to limited layoffs across the broader economy. Initial unemployment claims were a seasonally adjusted 215,000 for the week ended June 27, down 1,000 from the prior week. Continuing claims were 1.81 million for the week ended June 20, according to the Department of Labor, which remains consistent with an economy where employers are not cutting workers aggressively across the board. Investors should watch whether claims begin rising persistently, which would signal broader labor market cooling.

Challenger, Gray & Christmas reported that U.S.-based employers announced 45,849 job cuts in June, down 53% from May and 4% below June 2025. Through June, employers announced 443,604 job cuts, down 40% from the first half of 2025. Technology companies announced the most June cuts, with 15,503 in June and 139,156 year-to-date, and Challenger said artificial intelligence remained the leading stated reason for job reductions for the fourth consecutive month.

Investors should avoid treating AI-related job cuts as a simple recession signal. The June Challenger report showed announced layoffs cooled sharply from May, while the JOLTS and jobless claims data continued to show steady labor demand and contained layoffs. The data point to targeted restructuring, especially in technology, rather than broad labor market stress.

Investors watch jobs data closely because employment and inflation both shape Federal Reserve policy. Slower payroll growth can support the case for lower interest rates if it signals weakening demand. Persistent inflation can push the Fed in the opposite direction, especially when consumer prices remain above the central bank’s long-term 2% goal.

“The labor market remains strong enough to support economic expansion and consumer spending. Recent payroll gains and above-target inflation reduce the Federal Reserve’s incentive to cut rates,” says Bill Merz, head of capital markets research for U.S. Bank Asset Management Group. If inflation remains elevated and the labor market continues to show limited stress, policymakers may keep interest rates higher for longer than investors previously expected.

Markets have begun to reflect that uncertainty. Interest rate expectations tracked by CME Group showed markets assigning meaningful odds of a possible increase in the federal funds target rate by year-end as of July 6, 2026. 2 The Federal Reserve Summary of Economic Projections from its June 17 meeting also indicated one likely quarter-point rate hike this year. 3 Investors should watch upcoming jobs and inflation releases for signs that could shift the Fed’s policy path.

The June jobs report supports a balanced investor view. The economy continues to create jobs, unemployment remains low and wage gains still support household income. Those trends help limit near-term recession risk and support consumer spending, even as higher prices reduce some of the benefit from rising pay.

“This jobs market update should reassure investors that the economy still has support from employment and income growth,” says Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group. “It should also remind them that steady job gains and persistent inflation can keep interest rates range-bound until the path becomes clearer.” In practical terms, stock and bond markets may continue to react to each new labor or inflation release.

For investors, the labor market reinforces the value of staying balanced rather than reacting to one data point. Steady employment supports consumer spending and corporate revenue, while inflation and Fed policy can still influence bond yields, borrowing costs and stock market leadership. If you are weighing how labor market trends affect your investment plan, consider working with a financial professional to align portfolio decisions with your goals, time horizon and risk tolerance.

The labor market is a major driver of economic health in an economy where consumer spending comprises more than two-thirds of economic activity. When employment is high, consumer incomes are usually rising, supporting consumer confidence and typically leads to increased spending on goods and services. This accelerated spending often leads employers to add workers to satisfy growing goods and services demand. While the economy can experience periods of slower growth, the long-term trend is an expanding economy, which results in long-term job and income growth.

A strong employment environment often boosts incomes which often drives rising consumer spending. Consumers are considered the driving force of economic growth. According to the U.S. Bureau of Economic Analysis, consumer spending represents more than two-thirds of U.S. economic growth. When individuals are employed and earning solid wages, healthier economic growth often follows. Full-time employment provides households with predictable cash flow, making it easier to make long-term commitments that require financing, such as home and auto purchases.

Structural changes tied to fundamental shifts that affect how work is done often influence labor market trends. For instance, in the past, there was a structural shift from agricultural work to factory work as society became more industrialized. More recently, technology advances sparked an upturn in jobs tied to technology, or jobs that use technology to complete tasks. Today, many economists expect artificial intelligence advances to again create structural labor market changes and expand productivity. This could affect the types of jobs available and labor supply trends.

Labor force participation, a measure of the share of the population working or actively seeking work, has declined from its previous peaks. This decline is due in large part to workforce demographics, specifically the nation’s aging population and immigration changes. According to U.S. Bureau of Labor Statistics data, the labor force participation rate peaked at 67.2% in 2001 and now stands below 62%. Nearly one-quarter of the nation’s workforce is age 55 or older, and the “exit rate” due to retirement outpaces the entry rate of younger generations.

Technological advancements often create anxiety about the labor market impact. Technology and job requirements are constantly changing. Recent artificial intelligence (AI) advancements make this issue even more topical. In previous periods, technological advancements often involved automation replacing certain physical tasks. Today, AI may augment cognitive tasks, possibly changing skill demand in the economy.

Labor market signals can be a guide to current or forthcoming economic conditions. In other situations, labor data may not provide clear guidance. For example, when job growth appears strong, the numbers could be deceptive because hiring may be concentrated in narrow sectors of the economy or in less productive roles. If unemployment remains steady but hiring numbers are sluggish, it could indicate that companies are “hoarding” employees if it becomes challenging to replace them, while adding few new hires.

These data points should not be considered in isolation. Hiring and layoffs should be assessed together. Rising layoffs may raise alarms. Low layoff rates may reflect companies' reluctance to lose staff or indicate a challenging hiring environment. Hiring numbers and job openings reflect labor demand, but they may be lower even in a solid economic environment if companies retain staff and take a more cautious approach to adding overhead. The quit rate is a strong barometer of worker sentiment. A high quit rate reflects worker confidence that other jobs are readily available.

The job market is a key economic indicator, but it should be assessed alongside other indicators. The labor market and inflation are closely connected. If wages rise considerably, it’s important to assess that increase on an after-inflation basis to determine how much workers are benefiting from the wage environment, which translates to spending growth potential. Strong employment numbers typically signal a healthy economy.

The job market connects people looking for work with employers searching for talent. A strong job market signals a healthy, growing economy, as companies add jobs and compete for workers. When unemployment rises and job growth slows or declines, it often points to an economy that’s losing momentum.

The U.S. Bureau of Labor Statistics tracks the unemployment rate every month, giving us a clear view of the nation’s economic health. A lower unemployment rate usually means the economy is strong. This rate draws close attention because it shows how many people are actively seeking work. However, it doesn’t count those who have stopped looking or consider themselves out of the workforce.

When unemployment rises, it signals that the economy may be weakening. People often cut back on spending if they worry about losing their jobs, which can slow the economy even more. On the other hand, low unemployment typically reflects a robust and expanding economy.

The S&P 500’s recent rollercoaster performance has investors wondering what lies ahead for the stock market.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.