Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

The stock market under President Trump has advanced more than 30% since the 2024 election, supported primarily by corporate earnings growth rather than rising valuations.

Consumer spending and broad business investment, including but not limited to artificial intelligence, continue to support company revenues and profits.

Geopolitical conflict, tariffs, inflation, Federal Reserve policy and federal deficits could change the outlook if they weaken demand, investment or profit margins.

The stock market under President Trump has advanced despite sharp swings and an unusually active policy and geopolitical backdrop. Since the November 5, 2024 presidential election, the S&P 500 generated a total return of more than 30% through July 21, 2026. 1 Investors experienced meaningful volatility along the way, including a nearly 20% decline in early 2025, but stocks recovered as the economy and corporate profits proved stronger than many investors expected.

“Investors have overcome concerns about geopolitical conflict and trade announcements and focused on fundamental strength, namely corporate earnings growth,” says Bill Merz, head of capital markets research for U.S. Bank Asset Management Group. The market’s advance has also broadened beyond its largest technology-oriented companies. Smaller-company stocks rose more than 72% from their April 2025 lows through July 21, 2026, while gains across most S&P 500 sectors indicate that investors see opportunities across more of the economy. 1

Stock prices ultimately depend on company earnings. Consumer spending and business investment support company revenues, while productivity and cost control influence profit margins. When revenues and margins grow, earnings can rise and provide fundamental support for stock prices.

Corporate profits provide the clearest explanation for the stock market’s performance under President Trump. S&P 500 first-quarter revenues increased 12% from a year earlier, modestly above initial expectations for 10% growth, while earnings increased 28%, more than double the forecast at the start of the reporting season.¹ Analysts expect that strength to continue in the second quarter, with projected revenue growth of approximately 12% and earnings growth of 23%.

The relationship between earnings and stock prices provides a useful framework for understanding the market. Consumer purchases generate revenue, while business investment generates revenue for companies that provide equipment, construction, technology and services. Revenue then flows through profit margins to earnings, which tend to drive stock prices over time.

The latest market advance has drawn more support from earnings growth than from investors simply paying higher prices for the same profits. “The equity market is still trending higher. That goes back to healthy fundamentals,” says Terry Sandven, chief equity strategist for U.S. Bank Asset Management Group. “Sustained earnings growth is crucial for supporting these valuations.” Companies still need to meet a high earnings bar because stock prices remain elevated relative to historical averages, leaving less room for disappointment.

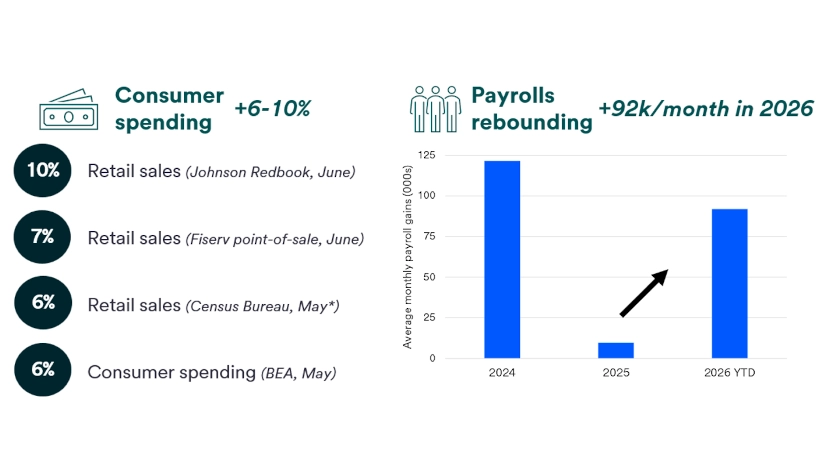

Consumer spending provides the first major source of support for earnings and the stock market under President Trump. U.S. consumer spending rose 6.3% in May from a year earlier, according to the Bureau of Economic Analysis. 2 Johnson Redbook’s weekly retail-sales measure and Fiserv’s point-of-sale transaction data also showed continued spending growth, with recent readings in the 6% to 8% range.

Consumer spending continues to grow across government, retail and point-of-sale measures, even though consumers do not all share the same experience. Higher-income households continue to spend strongly on travel, dining and other discretionary purchases, supported in part by rising asset values. Middle-income households remain active but have become more selective, while lower-income households face greater pressure from higher food, fuel and borrowing costs.

Aggregate consumer spending still carries broad economic significance because household purchases account for approximately two-thirds of U.S. economic activity. Consumer demand supports company revenues across industries ranging from retailers and restaurants to travel providers, financial institutions and manufacturers. Continued spending therefore provides an important link between household finances, economic growth, corporate earnings and stock prices.

Income and employment conditions help explain why consumers continue to spend. Average hourly wages rose 3.5% from a year earlier, while monthly payroll growth averaged approximately 92,000 through June 2026. 3 The pace of hiring has slowed from its longer-term average, but the economy continues to add jobs and unemployment remains low by historical standards.

Low layoffs provide another important source of support. Initial unemployment claims remain contained, indicating that employers have not broadly reduced their workforces. Continued employment and wage income give many households the capacity to keep spending, even when consumer-confidence surveys show concern about inflation, interest rates or the broader economy.

Consumer behavior therefore provides a more constructive signal than sentiment surveys alone. Households may express dissatisfaction with higher prices while continuing to make purchases because paychecks are still arriving and job losses remain limited. A meaningful increase in layoffs would weaken that support by reducing income and making other households more cautious about future spending.

Tax policy has supported household cash flow through two distinct channels. Federal income tax refunds ran approximately $58 billion above 2025 levels through the 2026 filing season, providing a near-term buffer as gasoline and other energy costs increased. 1 That refund increase represents a one-time adjustment rather than a source of recurring annual growth.

The One Big Beautiful Bill Act, or OBBBA, also included provisions with longer-lasting effects. Higher state and local tax and child-tax-credit deductions, along with new deductions related to tips, overtime, senior income and certain car loan interest, can support after-tax household income. Estimates point to a net $127 billion benefit for consumers, although the effect will differ across households. 4

These tax provisions do not replace the importance of wages and employment. Instead, they provide incremental support alongside labor income, particularly after the temporary increase in refunds passes. Investors will continue to watch whether that support helps households absorb higher costs without materially reducing spending elsewhere.

Business investment provides the second major source of support for the economy and corporate earnings. Capital spending among S&P 500 companies grew approximately 20% from a year earlier, reflecting investment in property, plants, equipment, technology and other productive assets.¹ Artificial intelligence represents a fast-growing component of that spending, but it does not account for the entire investment cycle.

Companies are also investing in factories, industrial equipment, power generation, grid capacity, software and supply chain infrastructure. Reshoring, which refers to moving production closer to the United States, and the broader shift toward electrification have added to demand for physical capacity. This investment extends across technology, industrial, energy, utility and service companies rather than remaining concentrated in a few large AI-related businesses.

Business investment affects economic activity in two ways. It creates current demand because one company’s spending on equipment, construction or technology becomes revenue for another company and can support jobs throughout the supply chain. It can also add capacity or improve productivity, which may support future revenue, profit margins and earnings growth.

The OBBBA also included business provisions intended to improve the after-tax economics of capital investment. Those provisions may encourage companies to invest in equipment, technology and productive capacity while supporting corporate cash flow. The potential benefits reinforce an investment cycle already supported by strong earnings and continued demand.

The same legislation also contributes to the longer-term federal debt debate. The Congressional Budget Office estimates that the law will increase federal debt by $3.4 trillion over the next decade. 4 Investors therefore must weigh the near-term support for household income, business investment and earnings against the possibility that additional federal borrowing eventually places upward pressure on interest rates.

That trade-off illustrates why presidential policies can influence markets without controlling them. Tax provisions can affect spending and investment, while their fiscal costs can influence Treasury borrowing and interest rates. The market outcome depends on how those competing effects ultimately influence economic growth, inflation and corporate earnings.

Geopolitical conflict becomes more important to markets when it disrupts energy supplies, trade routes or transportation. The Iran conflict has drawn particular attention because approximately 21% of the world’s oil normally moves through the Strait of Hormuz. The United States enters this period from a stronger position than many energy-importing economies because domestic oil production remains high, but no economy is fully insulated from a sustained global energy price increase. 5

“The key market question is not whether conflict creates headlines. It is whether higher energy prices last long enough to slow growth, lift inflation, and change the path for interest rates.”

Tom Hainlin, national investment strategist for U.S. Bank Asset Management Group

Higher energy prices can weaken consumer spending and business activity at the same time. Households must devote more income to gasoline, utilities and food, leaving less available for other purchases. Businesses also face higher fuel, shipping and input costs, which can squeeze profit margins when companies cannot pass those increases to customers.

“The key market question is not whether conflict creates headlines,” says Tom Hainlin, national investment strategist for U.S. Bank Asset Management Group. “It is whether higher energy prices last long enough to slow growth, lift inflation and change the path for interest rates.” The conflict remains a factor in the market outlook, but it is not the only factor driving stock prices.

Inflation rose earlier this year as energy costs increased, but June data showed some improvement. Consumer prices rose 3.5% from a year earlier, down from 4.2% in May, while core inflation, which excludes volatile food and energy prices, slowed to 2.6%. 3 Core inflation still exceeds the Fed’s 2% long-term goal, which keeps the path for interest rates uncertain.

The Fed influences the economy and markets through the cost of borrowing. Higher interest rates can raise financing costs for households and businesses, slow capital investment and reduce the value investors place on future earnings. Lower rates can provide support, although the Fed must balance that support against its goal of restoring price stability.

New Fed Chair Kevin Warsh has signaled less reliance on detailed guidance about future policy and a continued focus on inflation. That approach may give investors less certainty about the timing of future rate changes. Markets will focus closely on inflation, employment and economic growth data as they assess whether the Fed needs to hold rates steady or tighten policy further.

Tariffs remain another variable for the stock market under President Trump. They can raise the cost of imported materials and finished goods, influence supply chain decisions and add pressure to consumer prices. The economic effect depends on the tariff rate, the products covered and how much of the additional cost businesses absorb rather than pass to customers.

The Supreme Court voided most tariffs imposed in 2025 under one legal authority, and the administration later announced a temporary 10% global tariff while considering other options. The administration has also explored tariffs using other legal authorities, including Section 301 of the Trade Act of 1974. Investors have focused less on each announcement in isolation and more on whether the resulting policies materially affect demand, inflation, company margins and earnings.

Tariffs can create different outcomes across industries. Companies with flexible supply chains or greater pricing power may absorb the effect more easily, while companies that rely heavily on imported inputs may face more pressure. The broader market effect will depend on whether tariff-related costs remain manageable or become large enough to slow consumer and business activity.

Federal debt totals approximately $39.2 trillion, but the headline number does not determine the market outcome by itself. Investors also assess the government’s income, its ability to service existing debt and the economy’s capacity to generate future growth and tax revenue. The yield on the 10-year Treasury note provides one market-based indication of the return investors demand for inflation, growth and fiscal risk.

Large and persistent deficits create real trade-offs. Interest expense competes with other federal priorities, and rising borrowing needs could eventually require higher yields to attract enough Treasury buyers. Higher Treasury yields would also raise borrowing costs across the economy and could reduce the valuation investors place on stocks.

The United States retains substantial borrowing capacity because of its large and diversified economy, deep capital markets, the dollar’s role in the global financial system and continued demand for Treasury securities. Those advantages do not eliminate fiscal risk, but they help explain why markets have not treated current debt levels as an immediate crisis. Investors should continue to watch whether Treasury yields begin signaling greater concern about the government’s longer-term fiscal path.

The stock market outlook under President Trump remains constructive, but the path will not move in a straight line. Consumer spending and business investment continue to support revenues and earnings, while tax provisions and earlier interest-rate cuts provide additional economic support. Broad earnings growth also indicates that the market’s advance extends beyond a small group of AI-related companies.

Investors should still watch for evidence that this underlying chain has weakened. Rising layoffs could slow household spending, tighter credit could restrict business investment and sustained cost increases could pressure company profit margins. A prolonged energy disruption, renewed inflation pressure or materially higher Treasury yields could affect several links at once.

Investors can respond more effectively through discipline than prediction. A practical approach starts with reviewing whether a portfolio still matches long-term goals, time horizon and comfort with market fluctuations. Investors may also consider rebalancing when market movements push allocations away from their targets and investing extra cash gradually rather than attempting to identify the perfect entry point.

Presidential policies can shape taxes, trade, regulation and the economic backdrop, but they do not control market returns. Earnings, interest rates, inflation and investor expectations continue to exert broader influence over time. A thoughtful review with a U.S. Bank Wealth Management professional can help investors separate temporary market noise from developments that truly change the long-term outlook.

Investors often look at the stock market as a report card on a president, but that view is too narrow. Presidential policy can influence returns through taxes, trade, regulation, and public messaging. Over time, economic growth, inflation, interest rates, corporate profits, and the stage of the business cycle usually matter more than politics alone.

The White House can shape the backdrop, but it does not control stock prices. Investors value stocks based on what they expect companies to earn over time, and those expectations depend much more on profits, growth, and competition than on a single policy headline. Presidents appoint the Fed Chair but do not have the power to fire Fed officials over policy disagreements. The Fed also sets monetary policy independently, and Congress still must turn many proposals into law.

Markets usually follow a core group of long-term drivers. Interest-rate trends affect borrowing costs and stock prices, inflation affects household buying power and rate expectations, and corporate earnings help determine how much investors are willing to pay for shares. Productivity growth and demographic trends also matter because they shape long-term economic output.

The S&P 500 generated a total return of 81.3% during President Trump’s first term from 2017 to 2021. That ranked fourth for investor returns over a four-year presidential term since 1980. 1 The number is strong, but it still reflects the full economic environment of that period, not White House policy alone.

Corporate earnings growth has been the predominant factor driving stock markets to new all-time highs, although market performance during Trump’s presidency also reflects policy choices. In early 2025, proposed tariffs helped trigger a sharp selloff, with the S&P 500 falling nearly 20% by early April 2025, while investors later responded more positively to tax relief and Federal Reserve rate cuts. 1 Together, tariffs, tax policy, and interest rates shaped the market more than any single headline.

Politics often drives headlines, but broader economic forces usually do more to shape market outcomes. Investors continue to watch economic growth, inflation, and Fed policy because those forces influence company profits, borrowing costs, and stock prices across the market. Investors are also weighing whether advances in artificial intelligence can support stronger long-term productivity and growth.

Markets rarely move for just one reason. A policy shift, a war headline, or a major economic report can move prices in the short run, but longer periods reflect the combined effect of growth, inflation, earnings, interest rates, and investor expectations. That is why investors usually make better decisions when they focus on the broader economic picture instead of linking every market move to one event.

The stock market under President Trump has produced gains despite sharp swings. Since the November 5, 2024 election, the S&P 500’s total return climbed more than 30% as of July 21, 2026. 1

The stock market under President Trump has stayed resilient because profits and consumer demand have held up. Consumer spending is still growing, earnings expectations remain strong, and tax relief and lower interest rates continue to support the economy. Those supports have helped offset pressure from tariffs, oil-price spikes, and geopolitical conflict.

Shifting trade policies and fluctuating tariffs triggered volatility in the early months of President Trump’s second term, though markets have since recovered. In 2025, the S&P 500 generated a total return of 17.9%. Year-to-date through July 21, 2026, the S&P 500 is up 10.39%. During the primary years of former President Biden’s four-year term (2021-2024), the S&P 500 generated a 66.3% total return. Trump’s first term (2017-2020) saw an 81.3% total return. Since 1980, Trump’s first term ranks fourth for investor returns over a four-year presidential term. The top three terms were: Ronald Reagan (1985-1988, 91.8%), Bill Clinton (1993-1996, +88.6%), and Clinton again (1997-2000, +88.6%). 1

Investors should focus on discipline, not fast reactions. Review risk tolerance, rebalance if allocations have drifted, address diversification gaps, and consider phased investing if you are holding excess cash. That approach helps keep portfolios aligned with long-term goals even if volatility continues.

A look at historical equity market performance around midterm elections.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.