Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Iran-related market volatility creates an opportunity to review your plan, not abandon it.

Ask whether your portfolio still fits your goals, risk level, cash needs, and diversification targets.

If you hold extra cash, a phased investment plan may help you re-enter markets without trying to time the bottom.

The Iran conflict has raised oil prices and inflation concerns as investors watch shipping disruptions around the Strait of Hormuz. About 20% of global oil supply normally moves through that route, and a longer disruption can pressure global fuel and fertilizer costs, business expenses and consumer budgets. Even so, the broader backdrop still includes resilient consumer spending, rising incomes and solid earnings growth, which makes this a useful moment to review your long-term financial plan rather than react to every headline.

A conversation with a financial advisor can help turn uncertainty into a practical review. Instead of trying to predict every market move, investors can focus on whether their portfolio still matches their goals, risk tolerance, liquidity needs, and time horizon. Rob Haworth, senior investment strategy director for U.S. Bank Asset Management Group, notes, “You can’t always position your portfolio for the daily news cycle. Instead, evaluate current events within the broader context of economic and market trends.”

Market swings change how much of your portfolio sits in stocks, bonds , cash and other holdings, even if you have not made any trades. After several years of strong stock returns, many investors may be carrying more risk than their financial plan projected. Rebalancing brings a portfolio back to its intended asset class mix, helping it continue to reflect your long-term goals and comfort with risk.

Volatile markets can reveal a gap between the risk investors expect to tolerate and the risk they actually hold. Your risk profile depends on both your willingness to accept market swings and financial ability to absorb them over time. Tom Hainlin, national investment strategist for U.S. Bank Asset Management Group, sees value in these swings. “Staying invested, staying diversified and making measured adjustments helps investors remain focused on outcomes tied to their long-term goals.”

Cash plays an important role in a financial plan, but it works best when it has a clear purpose. Cash and cash equivalents can support liquidity, stability and emergency reserves. A common rule of thumb is that cash may make up roughly 2% of an investment portfolio, while separate emergency reserves often cover three to six months of income. In a period when higher oil prices can add uncertainty, this question helps separate useful liquidity from cash that may be sitting idle for too long.

Diversification becomes especially important when one area of the market stops carrying performance. A broader mix of investments can help because inflation, interest rates and geopolitical shocks do not affect every asset class in the same way. This is also a useful time to ask whether your portfolio depends too heavily on a narrow group of holdings when a broader mix may provide better balance.

Oil prices are one reason many investors feel pressure to make quick decisions. Higher energy prices create the most strain when they last long enough to affect household budgets, business costs and inflation expectations more broadly. “Investors watch inflation closely because of the impact on their personal budget, making Middle East conflict-related impacts a significant topic,” says Bill Merz, head of capital markets research for U.S. Bank Asset Management Group.

Many investors build cash when headlines get louder, but waiting for a perfect moment can be costly. Investing on a regular schedule, often called dollar-cost averaging, can reduce the pressure of trying to choose one exact entry point. It may not produce the highest return in every market, but it can help investors move forward with more discipline and less regret.

This question shifts the discussion beyond defense. A diversified portfolio can draw from a wider set of return drivers, including global equities, infrastructure, higher-income bond sectors and other areas that may behave differently from large U.S. stocks. Reviewing opportunities becomes especially useful when market volatility changes prices, leadership and relative value across asset classes.

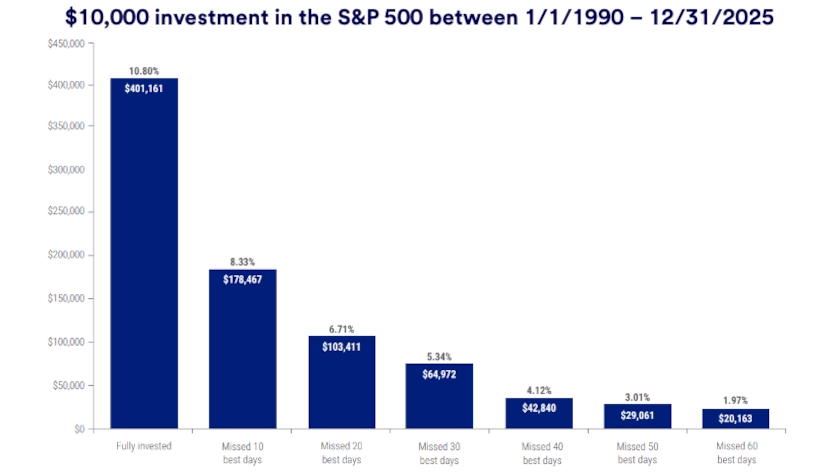

Market history shows that investors often pay a price for reacting to fear. Missing the market’s strongest days has had a major effect on long-term returns, and stocks have often finished years with gains even after meaningful declines during the year. That does not mean investors should ignore risk. Instead, they are often better served by reviewing all elements of their plan carefully than by making an all-or-nothing shift based on one event.

“The equity market is still trending higher. That goes back to healthy fundamentals. Most importantly, consumer and corporate technology spending remain strong, corporate margins remain robust, and inflation doesn’t appear problematic.”

Terry Sandven, chief equity strategist for U.S. Bank Asset Management Group

It also helps to remember what is still supporting markets underneath the headlines. “The equity market is still trending higher. That goes back to healthy fundamentals. Most importantly, consumer and corporate technology spending remain strong, corporate margins remain robust, and inflation doesn’t appear problematic,” notes Terry Sandven, chief equity strategist for U.S. Bank Asset Management Group. That does not remove short-term risk, but it does explain why many investors focus on fundamentals, earnings and diversification rather than assuming every conflict-driven selloff changes the long-term outlook.

That perspective is especially useful when markets become more sensitive to energy prices and inflation. Sandven frames the risk clearly, “Inflation is kryptonite to stock valuations. If energy prices rise and the price of other goods follows, this might force the Federal Reserve to raise interest rates, which could temper corporate earnings.” For investors, that is another reason to focus on balance, discipline and portfolio fit instead of reacting to one stretch of volatility in isolation.

Not necessarily. Geopolitical conflict can push oil prices higher and create short-term market swings, but that does not automatically mean your long-term plan is broken. A better first step is to review whether your portfolio still fits your goals, time horizon and risk tolerance before making major changes.

It can be, especially if recent market moves have changed your stock, bond or cash mix more than you expected. Rebalancing is one of the clearest ways to respond to volatility without trying to predict what happens next. It helps restore your portfolio to the level of risk and diversification that fits your plan.

Start by separating short-term needs from long-term investing money. Cash can support liquidity and peace of mind, but too much cash can reduce long-run growth if markets recover while that money stays on the sidelines. If the balance is truly excess cash, a phased investment approach may help you move it into the market without relying on perfect timing.

Diversification and asset allocation do not guarantee returns or protect against losses. Past performance is no guarantee of future results.

A fresh look at managing cash and investments in today’s changing interest rate environment can help support your pursuit of the goals that matter most to you.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.