Capitalize on today’s evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Housing market price growth has cooled as high mortgage rates pressure housing affordability and widen regional gaps.

Mortgage rates above 6% continue to pressure housing affordability, especially for first-time buyers.

Rising supply gives buyers more leverage, but stronger sales still depend on lower monthly payments.

Housing does more than provide shelter. Housing-related spending accounts for 15-18% of U.S. economic activity and remains a major part of household wealth, which is why shifts in home prices and mortgage rates can influence consumer spending and investor outlooks. 1, 2 The housing market has moved out of its rapid post-pandemic surge and into a slower, more selective phase shaped by borrowing costs, home prices, local supply conditions and the income buyers need to quality for a mortgage.

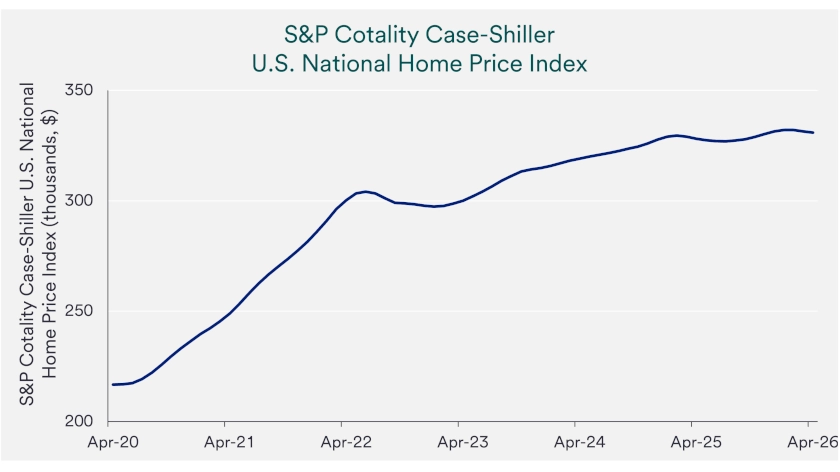

Home prices rose sharply from mid-2020 through mid-2022, but that pace has cooled. National measures now point to modest year-over-year gains, even as local markets continue to move in different directions. 3 For investors and households alike, the key question is no longer whether home prices are rising everywhere, but where demand can still support pricing as supply improves.

National home-price data now reflect a much slower pace of growth. The S&P Cotality Case-Shiller U.S. National Home Price Index gained 0.8% year-over-year in April 2026, down from 2.8% one year earlier, 3 while alternate measures such as Zillow suggest slightly softer national price growth in recent months. 4

The slower pace on a national level does not mean every market looks the same, because some cities continue to post solid gains while other formerly hot markets have moved lower. Midwest and Northeast markets have generally held up better, while several Sun Belt and Western markets have cooled after large pandemic-era gains. In practical terms, buyers and sellers now face a market where pricing power depends heavily on location, property quality and how many competing homes are available.

A slower housing market often adjusts through negotiation before it adjusts through large price declines. Homes can take longer to sell, sellers may offer repairs or closing-cost concessions, and buyers may gain more room to negotiate timing and price. That reset can cool activity and improve buyer leverage without producing a uniform national drop in home values.

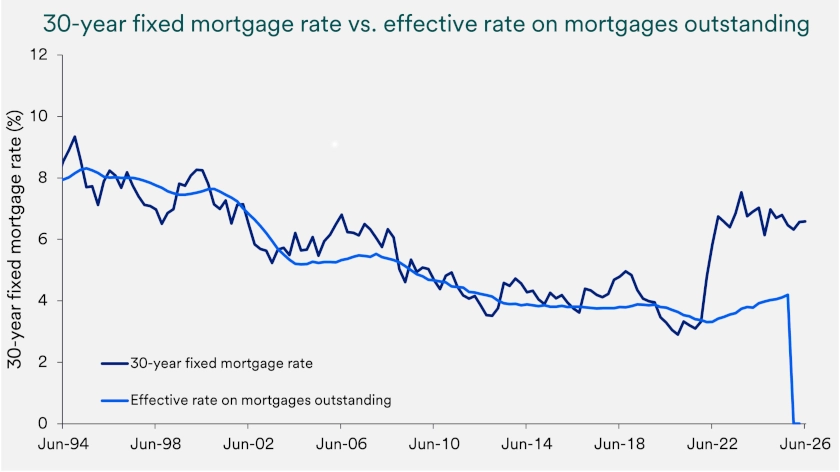

Mortgage rates continue to drive housing market activity because they directly affect the monthly payment buyers must carry. Even small rate moves can quickly change what buyers can afford, especially when home prices remain elevated. Many households now budget around the payment first and the home price second, which keeps sales activity sensitive to rate volatility. Freddie Mac’s survey showed the average 30-year fixed mortgage rate reached as low as 5.98% on February 26, 2026, before rising to 6.49% on June 25. 5

Rates also affect supply, not just demand. Many current homeowners still hold mortgages with lower rates than today’s market offers, so moving can mean giving up favorable financing and taking on a higher monthly payment. “The supply of existing homes on the market has gradually risen in recent years to more normal levels, partially as a function of homes taking longer to sell,” says Tom Hainlin, national investment strategist with U.S. Bank Asset Management. “Some current homeowners remain unwilling to trade their lower-rate existing mortgage for a higher-cost new mortgage.”

Affordability remains especially difficult for first-time buyers. The National Association of Realtors’ affordability framework uses 100 as the point where a typical household has enough income to qualify for a mortgage on a median-priced home, and recent first-time buyer readings remain well below that threshold. When wage growth does not keep up with rates and home prices, more households delay buying even if they still want to move.

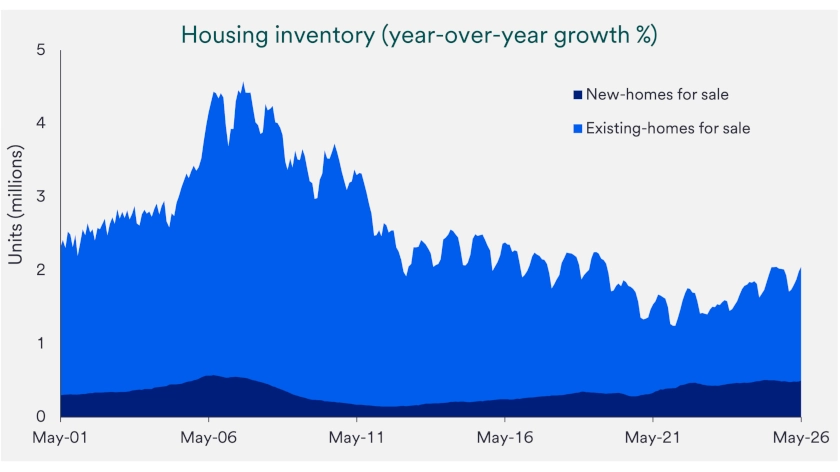

The resale market improved in May, but it still shows the effect of higher borrowing costs. Existing-home sales increased 3.2% from April and 3.2% from a year earlier to a seasonally adjusted annual rate of 4.17 million, according to the National Association of Realtors. Total existing-home inventory rose 3.3% from April to 1.55 million units, equal to 4.5 months of supply, while the median existing-home price rose 1.3% from a year earlier to $429,300. 6

Those figures point to a housing market that is thawing rather than accelerating. More listings give buyers more choice than they had during the tightest part of the market, but higher payments still limit how many households can close on a purchase. The May sales gain therefore looks encouraging, but stronger and more durable activity likely still depends on lower monthly payments or faster income growth.

New construction has added supply, but demand remains uneven. Sales of new single-family homes fell 7.3% in May to a seasonally adjusted annual rate of 580,000 and were 6.8% below the May 2025 pace, according to the U.S. Census Bureau and the Department of Housing and Urban Development. 7 New houses for sale totaled 496,000 at the end of May, representing 10.3 months of supply at the current sales rate.

Builders continue to respond with price flexibility and incentives. The NAHB/Wells Fargo Housing Market Index fell two points to 35 in June, while current sales conditions declined to 38, sales expectations held at 45 and prospective-buyer traffic remained weak at 25. 8 NAHB also reported that 35% of builders cut prices in June, with an average reduction of 6%, and 62% used sales incentives.

Builder incentives can help some buyers bridge the affordability gap, but they do not fully solve the market’s payment problem. A high months-of-supply reading in new homes signals that builders need to manage inventory carefully, especially in regions where demand has cooled. It also suggests buyers may have more negotiating power in new construction than they did during the tightest period of the post-pandemic housing market.

The next phase of the housing market depends on whether demand can absorb improving supply without forcing broad price cuts. Stable employment and wage growth can help, because buyers need income to qualify for mortgages and feel confident making large purchases. Lower mortgage rates would likely provide the fastest relief, but a durable rebound also requires listings, prices and household budgets to line up in more local markets.

“Investors were looking to the 2026 spring selling season as a critical test for housing demand, but so far activity has remained subdued due to elevated mortgage rates.”

Bill Merz, head of capital markets research for U.S. Bank Asset Management Group

“Fed rate cuts would help bring mortgage rates lower, supporting housing demand, although interest rate markets indicate investors believe this is unlikely this year,” says Bill Merz, head of capital markets research for U.S. Bank Asset Management Group. “Investors were looking to the 2026 spring selling season as a critical test for housing demand, but so far activity has remained subdued due to elevated mortgage rates.” For investors, housing still matters because homeowners hold substantial equity and housing continues to shape consumer balance sheets and spending patterns.

For investors, housing still matters because homeowners hold substantial equity and housing continues to shape consumer balance sheets and spending patterns. The opportunity set also extends beyond homeownership itself. Residential mortgage-backed bonds may offer attractive yields in some cases, especially when supported by strong homeowner equity and sound lending standards.

Mortgage-backed bonds are pools of home loans that pay investors from borrower payments, and non-agency mortgage bonds are not backed by a government agency. That distinction can create more risk, but it can also offer additional yield when the underlying borrowers and collateral remain strong. In this environment, investors should focus on credit quality, borrower equity and durability of cash flows rather than assume another sharp rise in home prices will drive returns.

Interest rates help determine how expensive it is to finance a home purchase. When rates rise, monthly payments increase, and many buyers can afford less home than they could before. When rates fall, financing becomes more manageable for more households, which can support demand and improve activity across the housing market.

Higher mortgage rates raise the monthly cost of buying a home, even if the purchase price stays the same. That can force buyers to lower their price range, delay a purchase, or reconsider how much of their budget they want to commit to housing. Over time, higher borrowing costs also increase the total amount paid over the life of a loan.

Lower rates can support home prices by improving affordability and bringing more buyers into the market. Price gains, however, also depend on other factors such as housing supply, job growth, household income, and local market conditions. Lower rates often help demand, but they do not guarantee the same outcome in every market.

Many homeowners already hold mortgages with lower rates than what is available today. Selling a home and buying another one could mean taking on a much higher monthly payment, which discourages some owners from listing their homes. That dynamic can keep the supply of existing homes tight even when buyer demand slows.

The housing market usually adjusts over time rather than all at once. Mortgage rates may change quickly, but buyers and sellers often need longer to respond as they revisit budgets, pricing decisions, and moving plans. Because transactions take time to complete, the broader effect of a rate move often shows up gradually over several months.

The Federal Reserve does not directly set mortgage rates. It influences short-term interest rates and broader financial conditions, which can shape where mortgage rates move over time. Mortgage rates also reflect bond market trends, inflation expectations, and investor views about growth and risk.

In many areas, the housing market is becoming more favorable for buyers because listings have increased faster than active demand. Redfin estimated there were 46% more sellers than buyers in April, 9 which often gives buyers more room to negotiate on price, repairs, or timing. Even so, this shift mainly helps households that can still manage today’s monthly mortgage payment.

A slower pace of home-price growth does not automatically make homes affordable. Monthly payments remain high because mortgage rates still sit well above the very low levels many buyers and sellers became used to before 2022. That is why sales can stay soft even when national home-price gains look modest.

Mortgage rates remain the most important signal because they directly shape affordability and buyer activity. Investors should also watch inventory and completed sales together, since more listings only matter if buyers can close on homes at current payments. Labor-market strength also matters, because steady job and wage growth help support the income needed to qualify for a mortgage.

Growth slowed late last year as the government shutdown weighed on activity, while consumer spending, hiring and income trends remained broadly supportive.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.