Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Rising interest rates can pressure stocks by raising borrowing costs, slowing demand and reducing the value investors place on future earnings.

Higher bond yields give investors more income and compete with stocks, although strong corporate earnings can support equity prices even when rates remain elevated.

Federal Reserve policy, tariffs and energy prices shape the 2026 rate outlook, while broader sector leadership expands potential stock market opportunities.

Interest rates influence nearly every link between the economy and the stock market. Consumers earn and spend, banks lend, businesses borrow and invest, and companies turn that activity into revenue and earnings. Over time, stock prices tend to follow earnings, while rate changes can accelerate or slow the process through monthly loan payments, business financing costs, bond income and stock valuations.

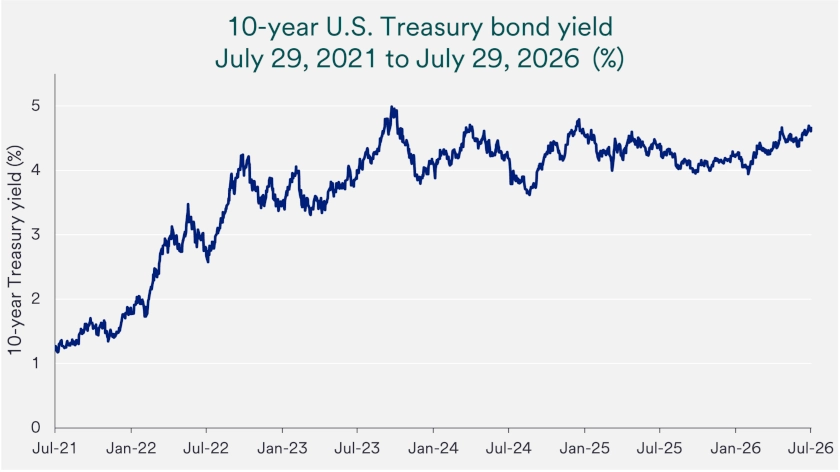

Investors watch both the Federal Reserve (Fed), which sets short-term policy rates, and the 10-year U.S. Treasury note yield, which responds to inflation, economic growth and government borrowing. At the market close on July 31, 2026, the S&P 500 stood at 7,489 near a record high, the 10-year Treasury yielded 4.71%, and the fed funds target range stood at 3.50% to 3.75%. Near record-high stocks alongside elevated rates reinforce a key point: higher rates can restrain economic activity and stock valuations, but rising corporate earnings can outweigh that pressure. 1

Rising interest rates can slow consumer spending by increasing monthly payments on mortgages, auto loans and credit cards. Softer demand can reduce sales for businesses tied to housing, vehicles and other financed purchases. Higher rates also increase corporate interest expense, leaving less cash for hiring, equipment, research and expansion and potentially slowing earnings growth.

“Despite higher interest rates, solid corporate earnings growth supports equity prices.”

Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group

Higher rates also make bonds more competitive with stocks. Treasury securities and other high-quality bonds can offer more income with less uncertainty than stocks, prompting investors to demand greater potential returns before accepting equity risk. Investors may therefore pay less for the same stream of expected corporate earnings.

Higher interest rates can reduce stock valuations even when a company’s earnings outlook remains unchanged. Investors compare future profits with returns available today, and higher market rates reduce the current value of earnings expected many years from now. Growth-oriented companies whose profits lie farther in the future can face greater valuation pressure, although strong earnings can offset some of the impact. “Despite higher interest rates, solid corporate earnings growth supports equity prices,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group.

The Fed held the federal funds target range at 3.50% to 3.75% on July 29 after reducing rates by 1 percentage point in 2024 and 0.75 percentage points in 2025. Three Federal Open Market Committee members dissented, highlighting different views about the balance between inflation and employment. As energy costs and persistent inflation complicate the outlook, investors have shifted from expecting rate cuts in 2026 to considering possible rate increases.

The federal funds rate and the 10-year Treasury yield do not always move together. The Fed directly controls an overnight lending rate, while longer-term Treasury yields reflect market expectations for inflation, economic growth and government borrowing. Stocks can still advance as Treasury yields rise when stronger growth and earnings outweigh higher financing costs and more attractive bond income.

Inflation influences interest rates because the Fed pursues both maximum employment and stable prices. Today’s solid labor market allows policymakers to focus more heavily on their inflation mandate. Current inflation remains above the Fed’s 2% target. Persistent inflation could keep rates elevated or prompt the Fed to raise them, while sustained progress toward 2% would give policymakers more flexibility.

Tariffs add another source of inflation uncertainty. New Section 301 duties of 10% to 12.5% took effect July 24 on goods from 60 trading partners, replacing the temporary 10% global tariff. Companies may absorb the cost, change suppliers or pass part of it to customers, leaving investors to assess the effects on consumer prices, profit margins and Fed policy.

The Iran conflict affects interest rates primarily through energy prices. Restricted oil flows can raise transportation and production costs. But draws from existing oil reserves and inventories, growing oil production, alternate shipping routes and changes in demand have helped the market absorb the disruption and keep oil prices elevated but contained for now. If those offsets weaken while restrictions persist, a longer-lasting oil price increase could renew inflation pressure, slow consumer spending and weigh on corporate profits.

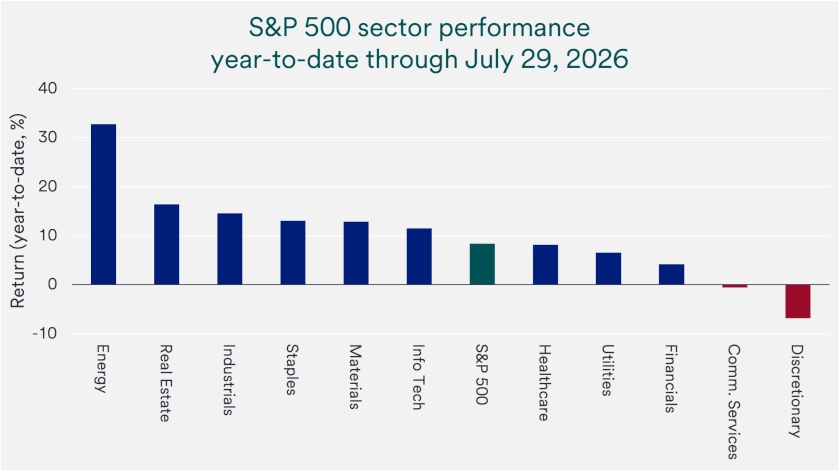

Stock market leadership broadened in 2026 as investors responded to changing rates, the Iran conflict and company earnings. All 11 S&P 500 sectors generated positive year-to-date returns through July 31, according to U.S. Bank Asset Management Group research and Bloomberg data. Energy led the market, while industrials, information technology, and real estate also posted meaningful gains, extending the advance beyond a small group of large technology companies.

Each sector has drawn support from different forces. Higher commodity prices and supply constraints have helped energy companies, while stronger capital spending and infrastructure demand have supported industrials. Real estate has advanced despite elevated rates, and information technology continues to benefit from investment in artificial intelligence infrastructure, including data centers, semiconductor chips, software and cloud-computing capacity.

Utilities benefit from rising electricity demand tied to data centers, electric vehicles and expanded U.S. manufacturing, though higher interest rates often weigh on the capital-intensive sector. Healthcare offers a separate set of long-term opportunities across pharmaceuticals, biotechnology, medical devices, diagnostic tools and life sciences, although company results vary widely. Broader participation can make the market more durable by reducing its dependence on one sector, investment style or interest-rate outcome.

For investors, the practical question extends beyond whether rates will rise or fall to whether potential returns justify the risks. Higher Treasury yields set a higher bar for stocks, while differences in earnings growth, financial strength and valuation create opportunities across sectors and investment styles. A diversified portfolio can combine stock market growth potential with bond income without relying on a single forecast for the Fed’s next decision.

The 2026 outlook remains constructive, although tariffs, inflation, geopolitical tension and elevated valuations can create volatility. Resilient consumer spending, strong business investment and rising corporate earnings continue to support stocks, while the oil market’s adaptations have contained part of the Iran conflict’s economic impact. “Relatively stable, though elevated, inflation, and rising corporate earnings continue to support higher stock prices, despite recently higher interest rates,” says Sandven.

Interest rates influence stocks through business costs, consumer demand, and investor preferences. Many companies borrow to expand operations, so higher rates can raise interest expenses and reduce profits available for hiring, equipment, and new projects. When rates move lower, borrowing costs can ease, which may support business investment and future growth plans.

Consumer behavior matters as well because many large purchases depend on financing. Higher rates often increase monthly payments on loans, which can reduce demand for durable items such as homes, appliances and vehicles, and weaken sales for related businesses. Higher rates can also draw money toward bonds and away from stocks as investors may prefer the surety of income from bonds relative to uncertain returns on stocks. Higher rates can also reduce what investors are willing to pay today for profits expected further in the future.

Stock markets often respond quickly when the Federal Reserve raises or cuts interest rates. Rate hikes can slow parts of the economy by raising borrowing costs, and they can increase the appeal of investments like CDs and bonds that offer interest income. Companies may also face higher debt costs, which can reduce spending on expansion or replacing old equipment and pressure profits.

Rate cuts are designed to support economic activity by lowering the cost of borrowing. Lower loan costs can encourage consumer spending and make it easier for companies to finance growth initiatives. When interest rates are lower, some investors may shift assets toward stocks in search of higher long-term return potential.

Investors often compare potential stock returns to what they can earn in U.S. Treasury securities, where interest and principal payments are backed by the U.S. government. When rates rise, Treasury yields can become more competitive, which may reduce demand for stocks. When rates fall, Treasury yields can decline, which can make stocks comparatively more attractive for investors seeking growth.

Investors also consider how rate levels change the market’s focus between near-term results and longer-term growth. When rates are low, investors often place a higher value on companies expected to grow profits more in future years. When rates are high, investors may place more emphasis on companies generating profits today, including those that pay dividends, rather than relying primarily on future earnings growth.

Yes, inflation matters because it often shapes the path of interest rates and corporate margins. If inflation stays high, the Federal Reserve may have less room to cut rates, and companies may face more pressure from higher input and wage costs. In 2026, tariffs and higher oil prices tied to the Iran conflict kept inflation in focus even as other parts of inflation were more stable.

Higher-rate environments do not automatically rule out strong stock performance. In 2026, investors favored sectors with stronger pricing power, steadier demand, or direct exposure to higher energy prices, including energy, industrials, materials, and utilities. Technology and healthcare can also continue to offer opportunities when powerful long-term trends such as artificial intelligence, aging populations, and medical innovation support earnings growth.

The Federal Reserve held its target federal funds interest rate in the 3.50%-3.75% range at its July meeting, a decision broadly anticipated by investors.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.