Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

REITs can diversify an investment portfolio with liquid access to residential and commercial real estate.

REIT investing may offer higher income than broad equity indexes, with more modest growth potential.

Healthy occupancy, slower property supply growth and lower debt support many REIT categories, though office properties face ongoing challenges.

Real estate investments can help diversify your stock and bond portfolio, but owning property directly requires significant capital, time and management. Real estate investment trusts, or REITs, offer another way to invest in residential and commercial real estate through publicly traded companies, funds or private vehicles. REITs can provide current income, potential long-term price appreciation and exposure to property types that may behave differently from stocks and bonds.

“REITs offer investors a compelling mix of income, price appreciation and diversification.”

Bill Merz, head of capital markets research, U.S. Bank Asset Management Group

REITs can also help investors add portfolio income through real assets such as apartments, warehouses, telecommunications infrastructure, healthcare facilities, retail centers and data centers. According to Bill Merz, head of capital markets research for U.S. Bank Asset Management Group, “REITs offer investors a compelling mix of income, price appreciation and diversification.”

Investors should still weigh REIT risks carefully, including interest rate sensitivity, tenant demand, property values and the financial health of the companies or funds they choose.

REITs are companies that own, finance or manage real estate-related assets. Their management teams make decisions about which properties to buy or sell, how to finance those properties and how to manage tenant relationships. Unlike developers that build properties mainly for resale, many REITs own and operate properties as part of a long-term business strategy.

To qualify as a REIT, a company must meet three specific real estate and income requirements:

A healthcare REIT offers a simple example. When you invest in one, you may gain indirect exposure to hospitals, senior living facilities, medical offices or assisted care properties. You do not manage those properties yourself, but you may receive a share of the income they generate through rent and related real estate cash flows, net of operating and other business expenses.

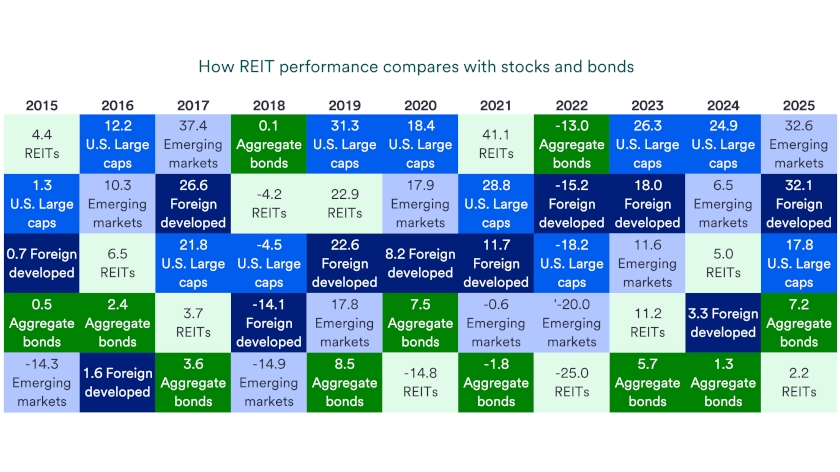

REITs have historically delivered total returns slightly below equities, while outperforming traditional fixed income indexes. Investors typically receive higher income from REITs than from a broad equity index like the S&P 500, though REITs generally offer more modest growth potential than stocks. This income can complement bonds in a diversified portfolio, while potential rent growth and property appreciation may support total returns over time.

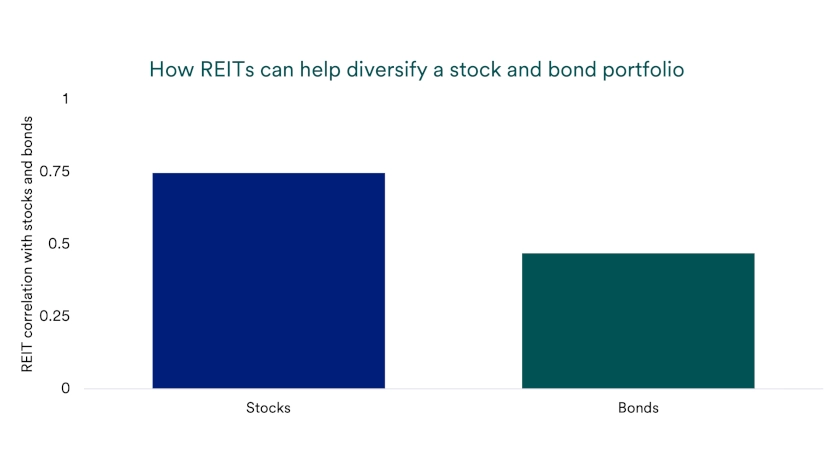

REITs also give investors exposure to return drivers that differ from traditional stocks and bonds, helping diversify stock and bond portfolios. Over the last decade, REITs showed a 0.75 correlation with stock prices and 0.50 correlation with bond returns. Correlation measures how closely two investments move together, and a reading below 1.0 suggests REITs may add diversification because their returns do not perfectly match either stocks or bonds.

Economic conditions still influence REIT performance, just as they influence other stocks and businesses. Economic growth can support tenant demand, rent increases and property values, while recessions can pressure occupancy and income.

Inflation can affect REITs by raising the value of in-place properties and buildings. Owners may also seek higher lease rates as compensation for cost increases, such as higher borrowing expenses.

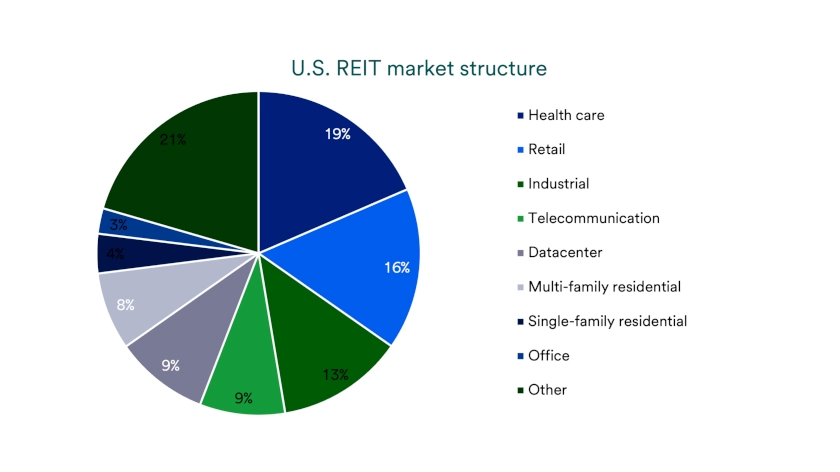

Broad REIT indexes include many types of real estate, each with different risks and opportunities. Healthcare, retail, industrial, and telecommunication-related companies make up about half of the U.S. REIT market. Other REIT categories include residential properties, data centers, self-storage, offices and hotels.

This variety can help investors diversify across real estate sectors tied to different parts of the economy. Industrial REITs may benefit from e-commerce and supply chain demand, while residential REITs depend heavily on housing costs and rental demand. Data center REITs can gain from artificial intelligence and cloud computing growth, while healthcare REITs often draw support from rising demand for medical services.

Geography also plays an important role in real estate investing. A strong rental market in one region may offset weakness in another, and local employment trends can influence property demand. REIT funds and exchange traded funds can help investors spread exposure across property types and locations instead of relying on a single company or building.

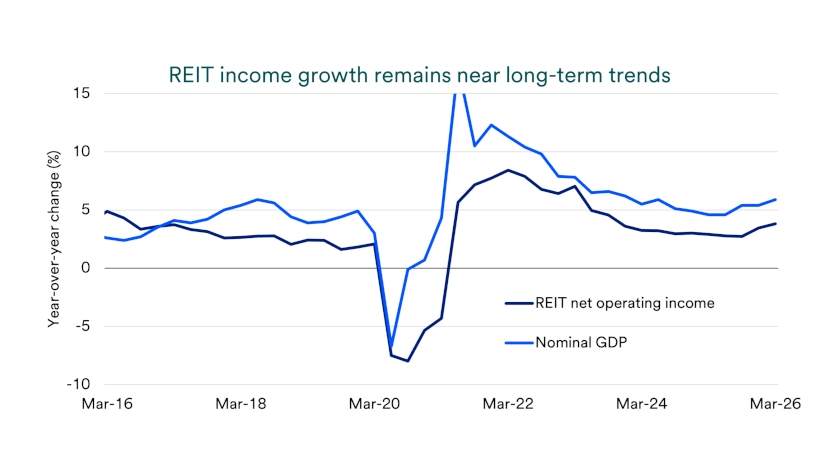

Several core factors shape REIT opportunities, including income growth, tenant demand, new property supply and borrowing costs. Net operating income, or NOI, measures real estate earnings after normal operating costs and helps investors evaluate a property’s core income power. Broad REIT allocations have historically generated 2.9% annual NOI growth, closely tracking economic trends, while several large property categories have recently outpaced the average.

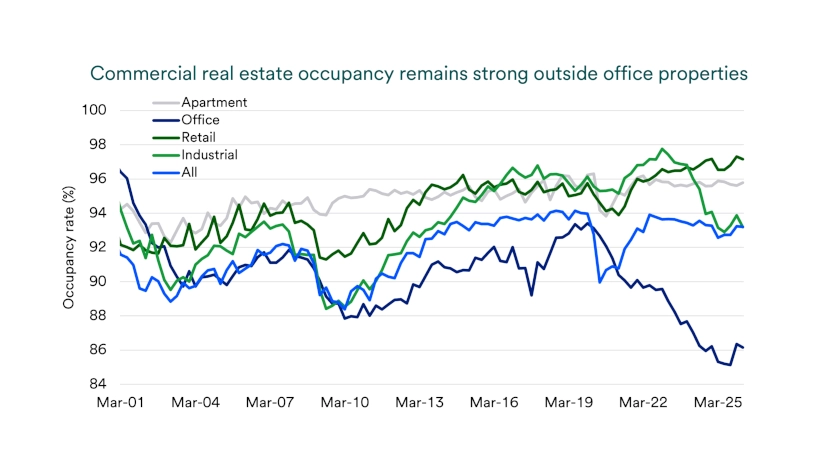

Occupancy rates provide another important signal. They measure how much leasable space currently generates rental income, which helps investors evaluate the potential for rent growth as well as underlying occupant demand. Industrial, retail and apartment properties currently show occupancy rates above 93%, while office properties remain weaker at roughly 86%, near the low end of their range over the past two decades.

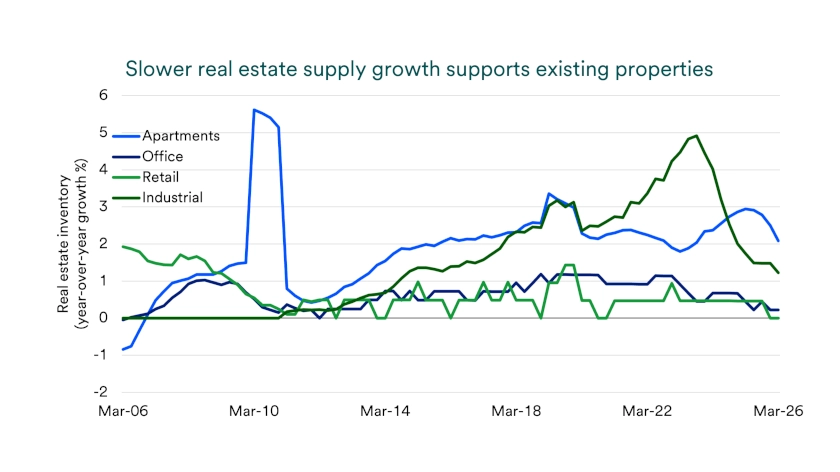

Property supply also affects REIT fundamentals. Real estate inventory growth slowed from 2022 through 2025 as higher borrowing rates, rising material costs and labor constraints increased development costs. Slower supply growth can support existing property values when tenant demand remains healthy, especially in areas such as apartments and industrial real estate.

REITs often borrow against their properties, so interest rates play a major role in REIT performance. When bond yields rise, commercial mortgage costs often rise as well, which can pressure profits and reduce the appeal of real estate income. Federal Reserve (Fed) interest rate cuts in 2024 and 2025 supported REITs, while the potential for rate hikes in 2026 adds uncertainty for investors.

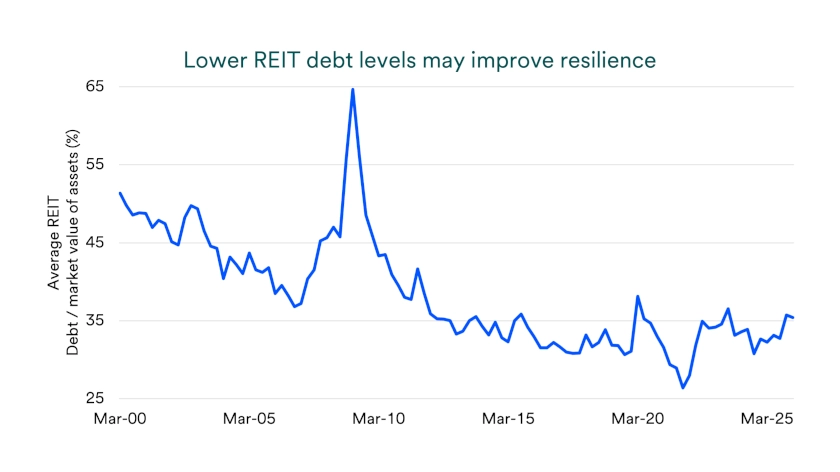

REIT balance sheets look stronger than they did before the global financial crisis. Since 2008, REITs have reduced debt levels and now average about 32% of asset value over the last ten years, compared with more than 40% in the five years before the crisis. Lower debt can improve resilience during economic downturns, although it may also limit upside during periods of faster growth.

While pockets of the real estate market like office properties still face headwinds from low occupancy rates and stagnant NOI growth, broader real estate market fundamentals remain sound. Diversified exposures to REITs that span property types continue to generate positive income growth, with strong occupancy rates, manageable debt levels, and can benefit from stable, to potentially lower, borrowing costs ahead.

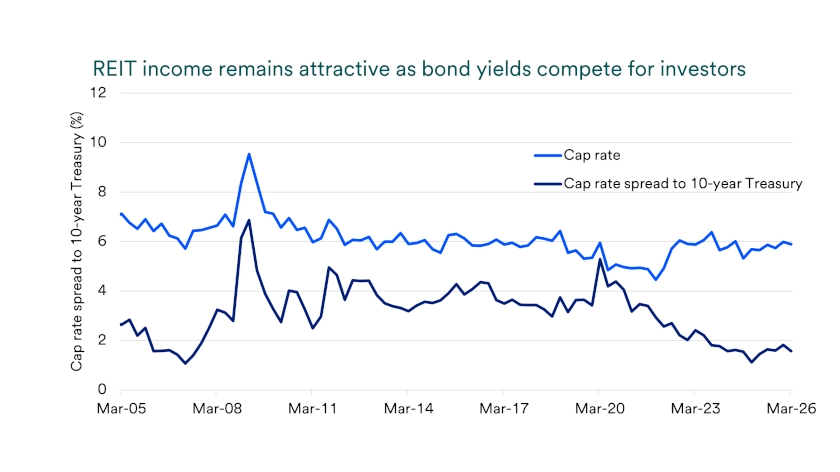

Investors also compare REIT income with bond income. A capitalization rate, or cap rate, measures annual property income as a percentage of property value and helps investors evaluate real estate income potential. Broad REIT allocations currently offer a 5.9% cap rate, close to the 20-year average of 6.1%, while office properties carry higher cap rates to compensate for weaker fundamentals.

REITs currently offer about 1.5 percentage points of additional income over 10-year U.S. Treasury yields. That premium is narrower than the 20-year historical average of 3.2 percentage points, which means investors receive less extra income than usual for taking real estate risk instead of owning Treasury bonds. Even so, REITs can still offer reasonable return potential when property income grows and investors maintain a long-term view.

Current REIT opportunities vary widely by property type. Office properties continue to face pressure from remote work, low occupancy and slower income growth. Some buildings have sold at steep discounts to prior valuations, but selective opportunities may develop as prices adjust and tenants continue to favor high-quality office space in desirable locations.

Data centers show a very different profile. Demand has surged as companies build artificial intelligence and cloud computing capacity, which has supported higher valuations and lower cap rates in the category. Investors still need to evaluate data center REITs carefully because technology can change quickly, and expectations for AI-related demand can shift stock prices.

Healthcare real estate benefits from long-term demographic demand. This category includes senior housing, assisted care properties, medical offices, clinics and hospitals. Healthcare properties now represent the largest U.S. REIT category, and their lower cap rates compared with some other large property types reflect investor recognition of long-term demand tied to an aging population.

Investors can access REITs in several ways. Publicly traded REITs trade on exchanges like individual stocks, which gives investors liquidity and the ability to choose specific companies. REIT exchange traded funds and mutual funds offer broader exposure across property types, companies and regions.

Private real estate vehicles may also fit certain investors, especially those seeking targeted strategies. These vehicles may focus on specific opportunities, such as office market dislocations or value-add multifamily properties in undersupplied markets. Private investments often carry different liquidity, transparency and suitability considerations, so investors should evaluate them with a financial professional.

REITs can play a useful role in a diversified investment portfolio, but they work best when investors understand both the income opportunity and the risks. Property type, interest rates, debt levels, tenant demand and valuations all influence performance.

U.S. Bank Asset Management Group views modest allocations to REITs and real estate as potential contributors to a diversified portfolio, and investors can speak with a wealth advisor to determine whether REITs fit their goals, risk tolerance and time horizon.

Rather than trying to time the market, consider holding on to stocks and other securities regardless of market fluctuations.

Bonds are a common investment in times of economic uncertainty, but they also play an important role in diversifying your portfolio.