Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Buy-and-hold means staying invested for the long term instead of trading on market timing. It can help you capture market recoveries and the market's best days as well as recover faster from losses and compound growth and dividends.

Over the past 35 years, the U.S. stock market posted positive annual returns in nearly eight of every 10 years.

Buy-and-hold works well for long-term investors, retirement savers and beginners who want a steady, low-maintenance approach.

Buy-and-hold is a passive investment strategy where you buy stocks or funds and keep them for years, regardless of short-term market swings. Instead of timing the market, you stay invested to capture long-term growth, compound returns and reinvested dividends.

Timing the market is challenging because you'd need to predict both the right moment to buy and the right moment to sell, which almost no one can do consistently. Plus, you must be right twice. Once when you buy and again when you sell.

It’s hard enough to time things correctly on one end, let alone getting the timing right on both ends. Especially when bond and stock markets tend to offer more years of positive returns than negative. Every trade can also trigger brokerage fees and taxes, which quickly reduce your net returns on both the purchase and the sale.

Instead of trying to time the market, focus on time in the market.

Buy-and-hold investing, a form of passive investing, means holding your broad asset-class investments for the long term regardless of short-term market moves.

Market timing requires you to predict both when to buy and when to sell, which is difficult to do consistently. Buy-and-hold keeps you invested through the market's best days, which often drive a large share of long-term returns.

A key to buy-and-hold investing is a willingness to build wealth gradually. Such investors don’t try to profit from market timing or short-term market fluctuations. The most common approach is owning funds that track broad market indexes, such as the S&P 500 or the MSCI All-Country World Index.

Active investing relies on real-time buying and selling to chase short-term gains. An active investor, or portfolio manager, watches the stock market closely and trades shares when they identify opportunities. However, this does involve more timing risk, higher costs and the chance of being in or out of the market at the wrong moment.

The takeaway: Buy-and-hold investing prioritizes consistency and patience. Active investing prioritizes timing, which is difficult to get right repeatedly.

A buy-and-hold strategy works because of how markets behave over time. Here are five reasons it holds up.

While market volatility can be intimidating, history shows the market recovers. While past performance is not a guarantee of future returns, the U.S. stock market has rebounded from declines and provided patient investors with a positive return on long-term investments. In fact, over the past 35 years, the market has posted a positive annual return in nearly eight of every 10 years. 1

Missing the market's best days can quietly wreck your returns. Historically, a large share of the stock market’s gains and losses occur in just a few days of any given year. As shown in this chart, even missing a handful of the best performance days over time can be costly.

That's the risk of market timing. Step out at the wrong moment, and you may miss the rebound. A buy-and-hold approach keeps you positioned for those high-performance days.

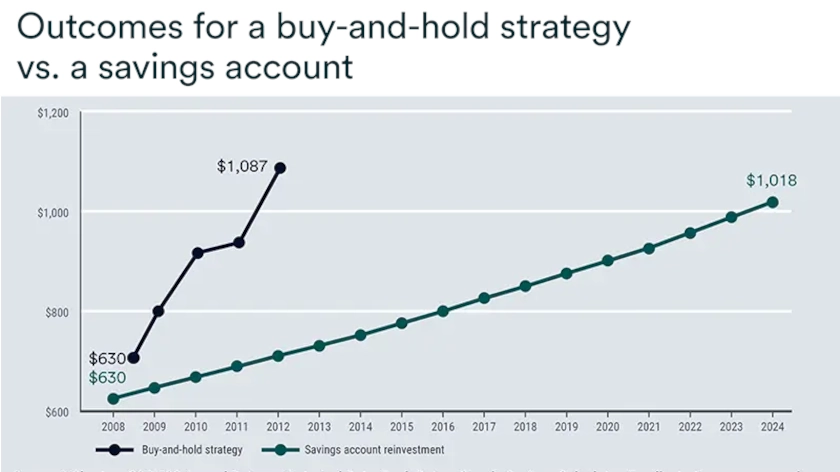

Buy-and-hold can speed up loss recovery, even after a bear market.

As an example, let’s say you invested $1,000 in the S&P 500 on January 1, 2008. That year, the index dropped 37%, leaving the investment worth about $630. 2 With a buy-and-hold strategy, you would have recovered your losses by 2012 without adding another dollar.

Moving that same $630 into a savings account earning 3% interest, compounded monthly, would take roughly 16 years to cross the $1,000 threshold.

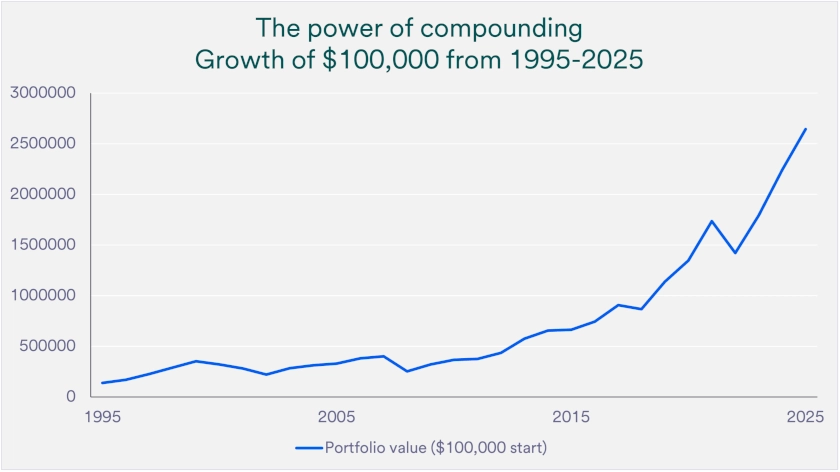

Time is a long-term investor's greatest asset. Compound growth lets your earnings generate their own earnings, building momentum the longer you stay invested.

While past performance is not a guarantee of future returns, the S&P 500’s inflation-adjusted annual average return is about 7%. 3 At that pace, $100,000 invested in 1995 more than tripled to $327,000 in 10 years. After 30 years, ending in December 2025, it grew to more than $2.6 million. 3 These gains accumulate over time and can provide an advantage to those who invest early and let their money continue to accumulate.

Don’t underestimate dividends. More than 30% of the S&P 500's total gains have come from dividends and their reinvestment. 4 Many investors choose to automatically reinvest dividends, buying more shares that earn more dividends. That’s compounding in action.

There are potential downsides to this approach. Reinvested dividends in a taxable account are still taxed in the current year, and that money can't go toward other opportunities.

If you're nearing retirement, you might switch dividends to cash to support living expenses. Before then, reinvesting dividends can help maximize your long-term gains.

To start a buy-and-hold strategy, define your time horizon and risk tolerance, then invest either a lump sum all at once or smaller amounts on a regular schedule through dollar-cost averaging.

You invest a large amount all at once. This might come from a bonus, an inheritance, the sale of company stock or an insurance payout. The sooner you invest, the sooner compounding starts working for you.

You invest a fixed amount on a regular schedule, regardless of price.

For example, say you put $300 into an index fund each month. When stock prices rise, your $300 buys fewer shares. When prices fall, it buys more. Over time, this can lower your average cost per share and smooth out the impact of volatility. It's a practical option if you're investing smaller amounts steadily.

The takeaway: Lump-sum investing puts your money to work immediately. Dollar-cost averaging spreads risk over time. Your choice depends on your cash, goals and comfort with volatility.

Buy-and-hold suits investors focused on long-term growth rather than short-term trades. It tends to fit three groups especially well:

Oftentimes, emotions can sabotage a buy-and-hold passive investment strategy. Overconfidence might lead you to trade too frequently, while fear of loss might cause you to hang on to investments that no longer support your goals or earn a sustainable return.

However, when you invest more regularly and focus on the long-term, you can feel confident that you’re steadily working toward your goals.

For most investors, yes. Market timing requires you to predict both when to buy and when to sell, which is difficult to do consistently. Buy-and-hold keeps you invested through the market's best days, which often drive a large share of long-term returns.

Passive investing still carries market risk. Your portfolio can lose value during downturns, and there's no guarantee of future returns. The strategy also requires patience, since growth builds gradually. The upside: it reduces timing errors, lowers trading costs and historically rewards investors who stay the course.

It depends on your situation. Lump-sum investing puts your money to work right away, which can help if markets rise. Dollar-cost averaging spreads your investments over time, reducing the risk of investing everything at a market peak. If you have a large amount to invest and a long time horizon, lump-sum often wins mathematically. If you prefer to ease in or invest smaller amounts regularly, dollar-cost averaging adds discipline.

Generally, several years to decades. The strategy is designed to ride out short-term volatility and capture long-term growth. The longer your time horizon, the more compounding can work in your favor.

Often, yes, especially while you're building wealth. Reinvesting dividends buys more shares that generate more dividends, fueling compound growth. Keep in mind that reinvested dividends in taxable accounts are still taxed in the year you receive them. Near retirement, you may prefer to take dividends as cash for income.

Staying invested can help you position yourself to capture market recoveries, the market’s best days, compound growth and dividends, all while avoiding the costs and risks of constant trading.

Start by defining your time horizon and risk tolerance, then choose between lump-sum investing or dollar-cost averaging. Whether you're saving for retirement or making your first investment, a disciplined, long-term approach can help you build wealth with confidence.

Learn how we approach your long-term investing success.