Financial guidance and support, tailored for you.

Explore the benefits of working with a dedicated wealth team.

Longer life expectancies mean your retirement savings may need to last 20 to 30 years or longer.

If you’re near or in retirement, bonds, annuities, and income-producing equities can offer additional retirement income beyond Social Security, a pension, savings and other investments.

A financial professional can help you determine the most appropriate retirement income strategy for your circumstances

A key focus in retirement is determining how your investments can generate sufficient income to support the lifestyle you choose. Yet that is only part of the challenge. Given today’s longer life expectancies and the realities of higher living costs over time, the income stream you generate today will most likely not meet your future income needs.

Consider that the average life expectancy for a person who reaches age 65 in the U.S. is roughly 85 years.1 Many will live far longer. Today, about one out of every three 65-year-olds will live until at least age 90, and about one in seven will live until at least 95.1

This means if you plan on retiring in your 60s, as many people do, your retirement savings might need to last for three decades.

You also need to keep in mind that over time, living costs will increase. Consider what happens to a person who withdraws $50,000 from savings and investments to fund retirement’s first year. If inflation averages 3% per year, after 30 years, close to $118,000 would need to be withdrawn to maintain the same living standard. That’s a lot of pressure to place on a traditional retirement account.

Social Security retirement benefits, which tend to play a more important role for lower wage earners, will replace only about 40% of pre-retirement earnings for people who earn less than $100,000 a year. Higher earners will receive only 33% of their pre-retirement earnings. You will likely need to supplement this income.

Social Security retirement benefits will replace only about 40% of your pre-retirement earnings. You'll need to supplement your benefits with a pension, savings or investments.

One option is to work after retirement. Retirees seek employment for all kinds of reasons, including the financial and mental benefits of staying active and involved in their communities.

However, having a plan in place for generating additional income during your retirement can help ensure your future income streams can keep pace with rising living costs. You’ll need to supplement your benefits with a pension, savings or investments.

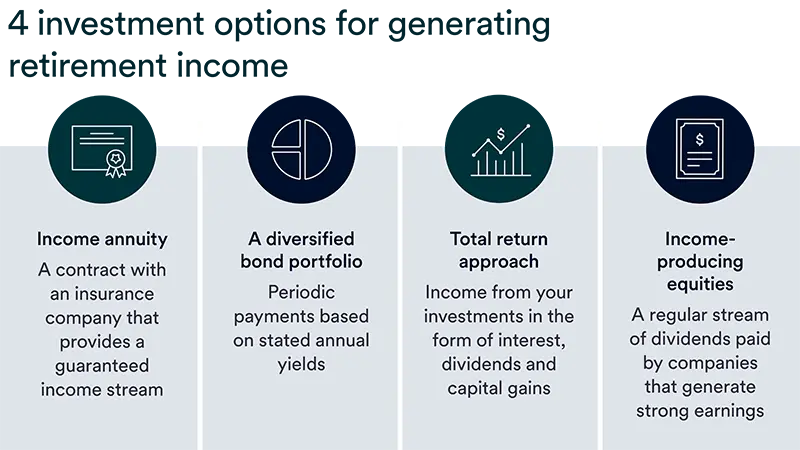

Here are four common investment options to help you generate income in retirement. Everyone’s risk tolerance is different, so these options are listed from lower to higher risk.

An income annuity is a contract between you and an insurance company where you pay a sum of money, either all at once or monthly, in exchange for regular income payments. While the insurance company holds your contributions, that money has the potential to accrue on a tax-deferred basis.

Annuities can help you set up a guaranteed income stream that is designed to last for a certain period or for the rest of your life. This income can also be paid throughout your life or through both your and another person’s lifespan (for example, your spouse). Since annuities provide income guarantees, they're often considered a form of insurance against the risk that you will outlive your retirement savings.

When you start taking disbursements, typically after you turn 59 ½, you can choose to receive a specific dollar amount regularly or payments that are adjusted for inflation. A financial professional can help you determine which type of annuity best fits your needs. “Annuities should be evaluated based on your specific circumstances,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management. “You must determine if it can sustainably generate sufficient income to meet your needs over time.”

Retirees often use annuities to supplement other guaranteed sources of income (such as Social Security) to offset non-discretionary expenses.

Benefits of annuities:

Challenges of annuities:

Bonds are available in many forms. You can invest directly in individual bonds, including:

This is where bond diversification is important. Yields will vary based on the credit quality of the issuing entity, the duration of the bond (how long before it matures) and current market conditions. Many investors choose to invest in bond mutual funds, a professionally managed, diversified portfolio of bonds from different issuers.

As far as how you receive income from bonds, you receive periodic payments from the bond issuer based on the stated annual yield effective at the time you invest. You can choose to hold the bond to maturity, at which time the issuing entity will repay the principal. Alternatively, you can choose to sell bonds on the open market before maturity.

In this case, the market value of a bond may vary from its face value, depending on the interest rate environment and the remaining bond term.

This raises an important point that investors often overlook: Bonds, while often considered a lower-risk investment, can fluctuate in value.

Benefits of bonds:

Challenges of bonds:

A total return approach provides income from your investment portfolio in the form of interest, dividends and capital gains. This type of portfolio invests in a balanced and diverse mix of stock and bond funds.

In this context, “total” return means you spend a portion of the average annual rate of returns — income and appreciation — over a longer period (10 to 20 years), rather than focusing on specific annual return rates or just drawing income generated by holdings in your portfolio. The aim is that this total return meets or exceeds your withdrawal rate.

“This is a way to grow a retirement portfolio to assure that it continues to meet the needs of people preparing for a retirement that could last 20 to 30 years or longer,” says Haworth. “It may offer a way to generate a superior total return compared with other investment approaches traditionally pursued in retirement.”

A note of caution about this approach: some assets you hold will be subject to fluctuation. Structure your portfolio in a way that the assets liquidated for purposes of generating income maintain stability regardless of market conditions. You want to avoid liquidating assets that are losing value.

In terms of withdrawal rate, a total return approach follows a “systematic withdrawal” strategy, in which you take a certain percentage of your investment as a distribution each year. The distribution amount generally ranges between 3% and 5% of the total value of the portfolio.

Benefits of a total return approach:

Challenges of a total return approach:

While people primarily invest in stocks to generate capital appreciation in a portfolio, some equities provide income in the form of dividends. Not all stocks pay dividends, and of those that do, certain stocks tend to pay higher dividends than others.

Companies typically pay dividends on a quarterly basis. They occasionally pay a “special dividend” due to unusual circumstances, but those are uncommon and not something you should count on. Unlike most bonds, stock dividends can vary with each payout period, and sometimes companies discontinue dividend payments. You need to be prepared for a degree of uncertainty with dividend payouts.

If your primary focus is to invest in a stock for income, it’s important to review its dividend-paying history. Stocks with a reliable history of consistent or steadily increasing dividend payouts are likely to be the most attractive to consider for this purpose. However, depending on the market environment, dividend-paying stocks may not generate total returns comparable to other types of stocks.

Utility stocks and REITs tend to be attractive to investors who want to generate income from an equity position. Both can help further diversify a portfolio made up primarily of stocks and bonds.

Publicly traded REITs are listed on major stock exchanges, so you can buy and sell this type of REIT as easily as you can trade stocks. Note that prices fluctuate daily.

“This price fluctuation is a consideration for investors, because it isn’t just the underlying value of the assets held in the REIT that affects the price,” Haworth says. “What you pay for a REIT or the price you receive when you sell a REIT may be affected by outside factors that affect the broader investment environment.”

Benefits of income-producing equities:

Challenges of income-producing equities:

There are a variety of ways this can occur. Among the strategies to consider are:

You may want to utilize one or a combination of these strategies to meet your retirement income needs.

Given life expectancies today, you need to consider that your retirement may last 20 years or longer. It’s important to protect yourself from the potential impact of inflation. With an average inflation rate of 3%, your living costs will double in less than 25 years. Therefore, you need to structure a portfolio that includes a portion of the portfolio dedicated to growth. That way, you’ll be in a position to have your retirement savings generate a growing stream of income to keep pace with rising living costs.

Just as when you were younger and accumulating savings to meet future needs, the idea of owning a diversified portfolio makes sense. Investing in a portfolio of income-generating bonds won’t provide sufficient inflation protection to meet higher living costs as you grow older. Only owning stocks means your savings may be subject to too much fluctuation, which can be costly to your long-term financial security if markets suffer periods of extreme volatility. Likewise, choosing to only put money to work in annuities may make you too dependent on a single source of income that may not include inflation protection. It’s important to structure a retirement income solution that meets your income needs while accounting for your risk tolerance and the potential of a long life expectancy. A financial professional can help you better understand your options and determine the most appropriate for your retirement income strategy.

The investment options you select in retirement should take into account your time horizon and risk tolerance level. A financial professional can help you better understand these options and determine if one or more are appropriate for your retirement income strategy.

Taking the time to understand your options and overall financial picture can better equip you to head into (or continue in) your retirement years with confidence.

Learn how we can help you plan your retirement income strategy.

You probably have big dreams for retirement. That’s why comprehensive retirement income planning – for the short, medium and long term – is so important.

Our planning services and professional guidance can help you work toward a more secure and fulfilling retirement.