Want retirement help or a second opinion on your plan?

Connect with a wealth specialist for a free no-obligation consultation.

An annuity is a contract between you as an investor and an insurance company and generates regular income payments in retirement.

A fixed annuity guarantees you a fixed rate of return for a specific period of time, while a variable annuity is tied to the market and can bring greater returns—and greater risk.

A financial advisor can help you determine what type of an annuity may be right for your retirement portfolio and even complete and submit the application on your behalf.

After you retire, you’ll need an income plan to pay your living expenses and maintain your lifestyle. Social Security can provide one income stream, as can a company-provided pension plan, if you have access to one.

While retirement savings vehicles such as IRAs and a 401(k) can supplement these income sources, another option is to purchase an annuity investment. Annuity accounts complement other retirement income vehicles and can provide guaranteed income through retirement, similar to how a pension plan works.

An annuity is a contract between you, as an investor, and an insurance company. You pay a lump sum or a monthly premium in exchange for regular income payments that can begin immediately or can be scheduled to start at a future date.

Annuities are similar to a pension or Social Security in that they can provide lifetime income guarantees and can help keep you from running out of money in your retirement years.

Annuities operate in two phases:

There are two main types of annuities: fixed and variable.

Fixed and fixed index annuities are generally used as tax-deferred accumulation vehicles and are typically more conservative. As long as the funds remain in the annuity until the end of the surrender period and interest rate duration, the holder of that product can't lose principal.

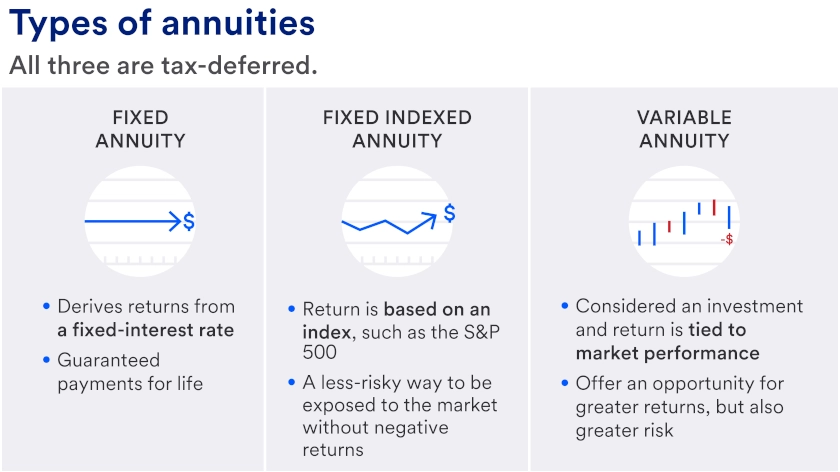

A traditional fixed annuity derives its return from a fixed-interest rate paid by the insurance company. It provides a declared interest rate for a specified period, very similar to a CD.

A fixed index annuity has a return based on an index less dividends, such as the S&P 500. This provides more upside potential, with downside protection that the return cannot be negative.

Variable annuities, on the other hand, are tied to the market and provide an opportunity for greater returns similar to mutual funds. However, because the market can go down, they also introduce risk.

Fixed annuities are purely insurance contracts, while variable annuities are filed with the Securities and Exchange Commission and are considered investments.

Both fixed and variable annuity products have insurance guarantees and can be converted to a guaranteed stream of lifetime income. However, variable annuities can lock in higher-income payments that are guaranteed throughout your lifetime. This is accomplished by adding a lifetime income rider for an additional fee.

Fixed annuities generally don't have fees; money grows in the investment without annual charges or investment fees. Variable annuities, however, are filed as securities and have investment charges similar to mutual fund fees. They also include insurance, mortality and expense charges.

If you take money out of your annuity before the surrender period, which is the period you must wait before withdrawing funds without penalty, you will generally incur a surrender charge. However, most annuities have a provision that allows you to access a percentage of your money without surrender charges. If you become terminally ill or need to move into a nursing home, all your money may become available penalty free.

Once the surrender schedule has expired, you can freely access your money. Like other retirement vehicles, if you withdraw money before you are 59½ you may be charged a 10% tax penalty on any gains.

Fixed and variable annuities may have provisions called “riders,” which allow you to access a guaranteed amount of income from the annuity every year regardless of the performance of the annuity investments or the remaining contract balance.

There are specially designed fixed and variable products, called immediate or deferred income annuities. With an immediate annuity, income payments will begin within the first 12 months of the contract. A deferred income annuity has an income stream that begins one year or later in the future.

Annuities are taxed similarly to a traditional IRA; the investment gains aren’t taxed while it accumulates. Once you withdraw money, you’re responsible for paying taxes on the growth.

The advantage of tax-deferred growth is that your dividends, interest and market gains are reinvested into the annuity. The growth on annuities and other retirement accounts is often taxed at lower rates than non-retirement investments because people are generally in a lower tax bracket in retirement than in their working years.

There's also a special rule for non-qualified annuitized contracts called an exclusion ratio. A portion of your payment is your principal coming back to you, so you're not taxed on that part of the payment.

Annuities offer the benefit of providing a guaranteed form of income that can help you manage costs over your lifetime, especially in retirement. Fixed annuities also offer a guaranteed rate of return, which provides protection for conservative investors who don’t want to accept the risk of uncertain markets. In addition to income guarantees, there are also death benefit guarantees.

However, with certain annuity protections and guarantees there may be costs, restrictions and perhaps, limitations of growth. Like other retirement accounts, a drawback of annuities is they are generally not liquid. You’re allocating money to annuities with the intention of taking it out at some later point in life. And with variable annuities, you have the additional risk of losing money in a down market.

Annuities are similar to a pension plan or Social Security in that they can provide lifetime income guarantees and some protection that other investment products can’t. They can help keep you from depleting your assets and running out of money in your retirement years.

When considering an annuity, it’s important to understand your goals and the level of protection you want. If you’re looking for a steady return, a fixed or fixed indexed annuity may be a good choice. If you’re looking for a market-type investment, you’ll want to consider a variable annuity.

The best way to know if an annuity would be a good addition to your retirement portfolio is to talk to a tax or financial advisor who understands your financial situation from an income and taxation perspective. A financial advisor can help you buy an annuity, completing the paperwork and submitting the application to the insurance company on your behalf.

Learn how we can help you design your retirement income strategy.

Customize your retirement income with these common investment choices.

Our planning services and professional guidance can help you work toward a more secure and fulfilling retirement.