Is your financial strategy keeping pace with your life?

Connect with an advisor for clear answers and strategies that align with your ambitions.

First factor fees, commissions, capital gains tax and other expenses related to selling your home into your sale proceeds.

If you’re using the proceeds from the sale to purchase a new house, compare your current costs to past costs, and keep in mind that your new home may also have an inflated value.

If you’re using the profits from a house sale for something other than housing, your financial goals and objectives should guide your decision-making.

When you sell your home, especially if you’ve lived there for years, it can result in a windfall of money. So, what should you do with the proceeds?

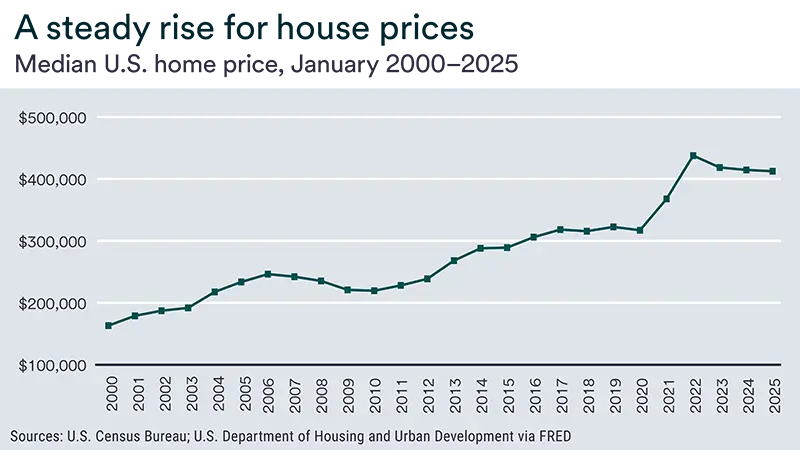

The real estate market has been booming for the past few years and more households are wrestling with this question. Over the past decade, the median home price in the U.S. has increased by roughly 40%. As a result, the average homeowner now has home equity of $313,000, according to Intercontinental Exchange, a mortgage technology company.

How you use the proceeds from the sale of a house can make a major impact on your future financial health, but there’s no one-size-fits-all answer to how you direct those funds.

Let’s review a few key factors that may help you determine the right approach for you.

How you use the proceeds from the sale of a house can make a major impact on your future financial health, but there’s no one-size-fits-all answer to how you direct those funds.

In the world of real estate, the terms “proceeds” and “profits” are sometimes used interchangeably. But it’s important to distinguish between the two.

When you close on the transaction, the home sale proceeds are the total amount of money you receive from the buyer. But it’s important to keep in mind that you almost certainly won’t get that entire amount in cash. Your profit from a home sale—or “net proceeds”—is the amount that’s left over after deducting your expenses, including your remaining mortgage balance.

To figure out the profit you’ll be left with after accepting a buyer’s offer, deduct any expenses for which you’re responsible in the transaction. These may include:

You may also have to pay capital gains taxes, unless you earned a profit of less than $250,000 ($500,000 if you’re a joint filer) or qualify for the home sale capital gains tax exclusion. Even though this amount isn’t automatically deducted by the settlement company at your closing, it reduces your net profits.

A tax professional can help advise you on how much you owe and whether you need to make an estimated tax payment to the IRS.

In most cases, the factor that’s going to have the biggest impact on how much you earn is your home’s sale price. And that can vary significantly based on the timing of your sale. You’ll potentially make more profit by listing your home during a seller’s market—when the number of available homes is relatively scarce in relation to demand—rather than a buyer’s market.

Depending on your circumstances, you may not be in control of when you list your property. For example, you might have to move for a new job or a workplace relocation. If your situation is a bit more flexible, however, timing your home sale when market conditions are more favorable to a seller can make a substantial difference.

Take an owner whose home can fetch $700,000 in a strong seller’s market. If their outstanding mortgage and other expenses total $400,000, they’ll walk away with $300,000 in net proceeds.

If they wait and market drops 10%, however, they’ll only get $630,000 for the home. Assuming the same costs, they will only come away with a profit of $230,000.

There are plenty of choices for what to do with the profit from a house sale. Common ways people spend the profits from a house sale include:

But before making that decision, it’s important to take a step back, weigh the pros and cons of different options, and consider how those home sale proceeds could affect your current and future finances.

Using the money you earned from your home sale to help purchase another home is often a wise choice, especially when interest rates are relatively high. The bigger your down payment, the smaller the loan you’ll have to pay off. With enough cash down, you may even be able to afford a 15-year loan so you’re not carrying a large mortgage into retirement.

With a sizable profit from your sale, however, it can be tempting to put it toward an even pricier property without realizing the long-term impact on your finances.

Even if the money you put down makes the loan payments reasonable, it’s easy to neglect other out-of-pocket expenses that come with it. For example, buying a bigger, more expensive home often means higher property taxes, utility bills, insurance costs and maintenance costs. Plus, you may need some of that money for moving and storage costs.

If you’re moving into a rental or downsizing, however, you may have more proceeds than you need for your next home. In that case, you might consider using the money to purchase a vacation home or rental property that may provide a steady source of income.

While buying a secondary property represents an exciting opportunity, make sure you can afford the payments on both homes even if you experience an unexpected event, like the loss of a job or a major medical bill.

Before using your sale proceeds on a new home, carefully assess your overall situation. If you have certain weak points in your financial plan, you may want to shore up those areas before putting the entire windfall toward your next property.

You could also use your net home sale proceeds to:

If you have a substantial amount of credit card or other high-interest debt, this can be a great opportunity to zero out your balances and free yourself up to focus on other financial goals.

Do you have enough in a savings or money market account to cover three to six months’ (or more) worth of expenses? If not, you might want to use some of your home sale profits to safeguard your finances against emergencies.

Take stock of how much you have saved for longer-term goals. A retirement calculator, for example, can help you assess your readiness for life after you exit the workforce. If you’re behind the curve, consider using some of your sale profits to get back on track.

Learn how we can help you go further on your path to achieving your financial goals.

If you have available cash, it could be tempting to pay off your mortgage. But there are other options and factors to consider before making such a big decision.

We can help you identify and prioritize your financial goals and design a plan to work toward them, making adjustments as your needs evolve.