Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Capital gains tax is a tax on any profit you make from the sale of a capital asset, such as property or equities.

Capital gains and/or losses may be either short-term (held less than one year) or long-term (held one year or more). When you have realized capital gains, the capital gain tax rate you pay depends on whether the gain is long-term or short-term, as well as on your income level.

Implementing strategies such as tax loss harvesting and planned charitable giving as part of your overall tax plan may help you lower your overall tax liability.

Even during times of market volatility, many investors will have taxable capital gains at year-end. What is capital gains tax? You have a taxable gain when you sell a capital asset—such as shares of a publicly traded company on a stock exchange—for more than your total cost basis (what you paid for it, plus or minus any adjustments).

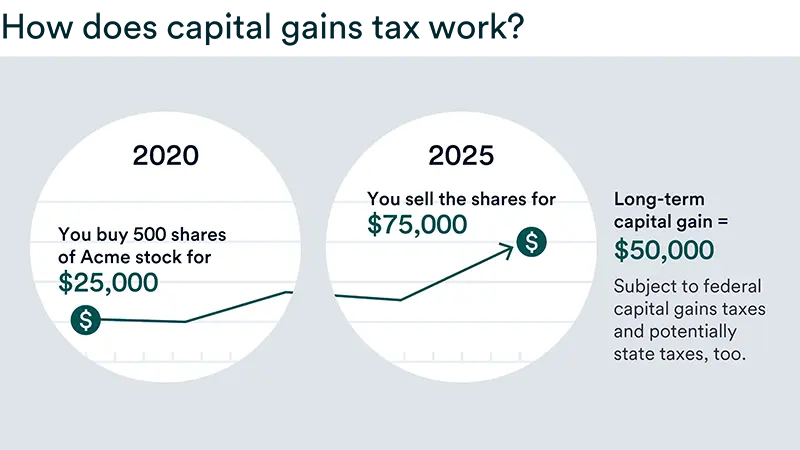

For example, if you bought 500 shares of Acme Co. stock in 2020 for $25,000 and you sold those shares in 2025 for $75,000, your long-term capital gain would be $50,000, assuming there are no related expenses. That $50,000 in profit will be subject to federal capital gains taxes, and depending on where you live, potentially state taxes as well.

“A financial professional can help you build a larger financial planning strategy that identifies risks and opportunities while mitigating your tax liability.”

Dan Willing, senior vice president and Wealth Strategist, U.S. Bank Private Wealth Management

Taxes on capital gains are by no means inconsequential. The federal government collected over $260 billion in capital gains tax revenue in 2025, according to a Tax Foundation analysis of Congressional Budget Office data.

Having a tax strategy and understanding your tax exposure is therefore an important part of any good investment plan. Specific to capital gains taxes, it’s important to evaluate both gains and losses that you may have accrued throughout the year and be aware of steps that you can take to reduce that tax liability before year-end.

While it’s important to discuss your tax situation with your accountant and/or tax attorney, you should also involve your financial professionals in your tax discussions throughout the year and particularly near year-end. “While we don’t provide tax advice, we can help you build a larger financial planning strategy that identifies risks and opportunities while mitigating your tax liability,” says Dan Willing, senior vice president and Wealth Strategist with U.S. Bank Private Wealth Management.

One of the first things to understand about capital gains is that the federal tax rate can vary depending on the circumstances. Even if you and your neighbor both sold the same number of shares of Acme Co. stock, the two of you may owe very different amounts in capital gains taxes. That’s because the federal capital gains tax rate is determined by two factors: your income bracket and the amount of time you held that asset.

Say you held that Acme Co. stock for one year or longer. The proceeds would be taxed at the long-term capital gains rate, which is lower than the tax rate for short-term capital gains, which is taxed at ordinary income tax rates. Depending on your tax bracket, you could owe 0%, 15% or 20% on capital gain, regardless of whether you own the asset for one year or 10.

If your neighbor held that Acme Co. stock for less than one year, the proceeds would be taxed the same as ordinary income, meaning that they could end up paying as much as 37% depending on their federal income tax bracket.

Gains from the sale of an investment also can trigger the net investment income tax (NIIT), a 3.8% federal tax that layers on top of federal capital gains taxes. Individuals who exceed a certain threshold of modified adjusted gross income, or MAGI ($200,000 for single filers and $250,000 for married couples filing jointly) are subject to NIIT on that gain.

Some states also charge capital gains taxes on top of what they owe the federal government. As an example, if the top individual income tax rate in Minnesota is 9.85%, that rate applies to W2 income and any short or long-term capital gains. In comparison, a state such as Florida has no income tax and no capital gains tax. So, for someone who lives in Minnesota and is planning to retire to Florida, it may be beneficial to wait to sell investments.

Long-term capital gains on investments held for more than a year are taxed at the rate of 0%, 15% or 20%, depending on your taxable income and tax filing status (individual or married couples filing jointly).

Short-term capital gains on investments held for less than one year are normally taxed at the same rate as your taxable income, ranging from 10% to 37%.

|

2026 Long-Term Capital Gains Tax Rate |

Single |

Married Filing Jointly |

|---|---|---|

|

0% |

<$49,450 |

<$98,900 |

|

15% |

$49,450-$545,000 |

$98,900-$613,700 |

|

20% |

>$545,500 |

>$613,700 |

2026 Long-Term Capital Gains Tax Rate

0%

Single

<$49,450

Married Filing Jointly

<$98,900

2026 Long-Term Capital Gains Tax Rate

15%

Single

$49,450-$545,000

Married Filing Jointly

$98,900-$613,700

2026 Long-Term Capital Gains Tax Rate

20%

Single

>$545,500

Married Filing Jointly

>$613,700

Individuals can take a variety of steps to reduce or offset capital gains. “Once again, it’s important to look at capital gains from a broader financial strategy perspective,” says Willing. “In some situations, it can even make sense to harvest gains now when there are opportunities to offset those gains with losses.”

When calculating capital gains taxes, there are different expenses that you may have paid over the hold period that can offset a gain. For example, you can include transaction fees or taxes paid on reinvested dividends to calculate the cost basis on the sale of an asset, which reduces the overall gain.

The sale of a home automatically includes a $250,000 exclusion on gain for an individual and $500,000 for a married couple filing jointly. If you net value above that cap, you could include a variety of factors in your cost basis outside of the original purchase price to help offset the gain. Some examples include money paid out for a realtor’s commission, qualifying renovations, repairs and improvements to the home.

“You never want taxes to be the tail that wags the dog on investment strategy,” Willing says. “Regardless of whether you’re selling investments for a gain or a loss, it needs to fit into a larger investment strategy.” He adds, however, that generating losses and carrying them forward can make financial sense for many investors.

“Tax laws are very complex, nuanced, and in some cases, downright odd. So don’t try to do it on your own,” says Willing. “It’s wise to work with your financial professional, accountant and tax attorney to create a tax strategy that makes sense for you.”

Learn how our approach to wealth planning can help you see a full view of your financial picture.