Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Tax-loss harvesting means selling securities below their cost basis to offset realized capital gains.

You can use it while rebalancing your portfolio, converting to a Roth account, or working to stay in a lower tax bracket.

The strategy is nuanced, so guidance from a financial and tax professional matters.

Tax-loss harvesting is the practice of selling an investment for less than you paid for it, then using that loss to offset capital gains you've realized elsewhere. Done strategically, it can lower your tax bill while keeping your long-term plan on track.

Tax-loss harvesting works by selling securities at a price lower than their cost basis, which is the original purchase price. That sale creates a capital loss. You then apply the loss against gains you've realized from other investments, such as real estate, a business, or other significant assets.

How losses match up to gains depends on how long you held the assets:

Tax-loss harvesting is the practice of selling an investment for less than you paid for it, then using that loss to offset capital gains you've realized elsewhere.

Short-term capital gains come from assets you held for 12 months or less, and they're typically taxed at your ordinary income rate. Long-term capital gains come from assets held more than a year, and they usually get a lower federal tax rate. That gap is why the holding period matters so much when you harvest losses.

If you have more losses than gains, short-term losses can offset long-term gains and vice versa. Beyond that, you can apply up to $3,000 of leftover losses against your ordinary taxable income ($1,500 if you're married filing separately). Any remaining losses carry forward to future tax years.

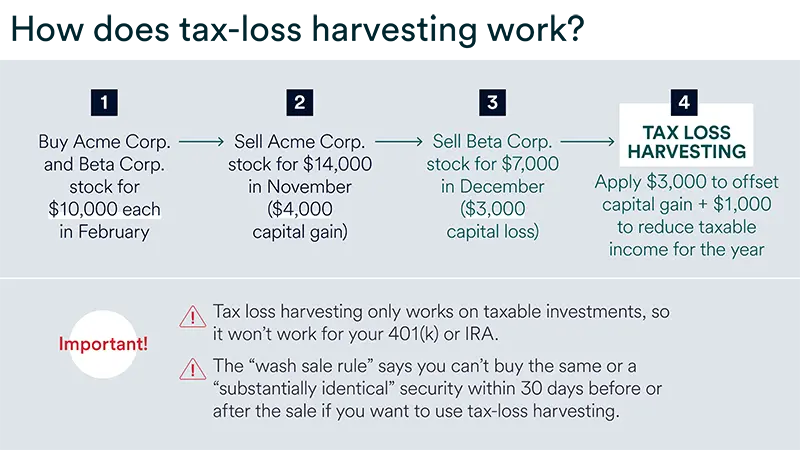

Consider this scenario. You own shares of Acme Corp. and Beta Corp., both held for less than 12 months. Selling Acme Corp. stock at a profit triggers short-term capital gains tax, which is typically higher than the long-term rate. To soften that hit, you sell Beta Corp. for less than you paid.

The short-term loss from Beta Corp. first offsets the short-term capital gain from Acme Corp. Any excess can then be used to reduce your ordinary taxable income or carried forward for future use.

Two important items of note:

Tax-loss harvesting can deliver real benefits, depending on your situation. It can lower your capital gains tax, reduce your adjusted gross income, help you stay in a lower tax bracket, and make portfolio rebalancing more tax-efficient. Over time, keeping more of your returns can support your retirement goals.

Here’s when it tends to make the most sense.

Rebalancing in an up market often generates capital gains. Harvesting losses lets you sell weaker positions to offset those gains, potentially easing the tax impact of the rebalance.

If you hold wealth across investments, a business, and property, harvesting losses becomes a useful tool for balancing gains across all of it. Applying losses against gains helps you stay tax-efficient as your holdings grow.

In a down market, converting a traditional IRA or 401(k) to a Roth account can mean lower taxable income on the conversion. Pairing that move with harvesting losses can trim the tax bill further, which is especially valuable if you have a long time horizon for growth.

Taking losses strategically can lower your adjusted gross income (AGI), which is the figure the IRS uses to set your tax bracket. A lower AGI may keep you in a lower bracket and could allow eligibility for Roth IRA contributions or other deductions.

If you’re approaching retirement with a lot of company stock, combining tax-loss harvesting with net unrealized appreciation (NUA) planning can reduce what you owe. For example, you might sell certain positions while identifying other assets with recorded losses to keep the overall picture balanced.

The wash sale rule is an IRS rule that blocks you from claiming a tax loss if you buy the same, or a substantially identical, security within 30 days before or after the sale. Instead of writing off the loss, you add it to the cost basis of the replacement shares. The rule exists to stop investors from selling purely for a tax break while keeping the same position.

If you sell a security at a loss in a taxable account and buy an identical one in your IRA within the disallowed window, the loss is permanently disallowed. Unlike an ordinary wash sale, it isn't added to any cost basis, so the deduction disappears entirely.

There are a few practical ways to steer clear of a wash sale:

Tax gain harvesting is the intentional sale of appreciated investments to realize long-term capital gains while your income sits low enough to qualify for a reduced federal capital gains rate. It's the mirror image of tax-loss harvesting. Rather than selling at a loss to offset gains, you deliberately recognize gains when the tax cost is minimal.

For 2026, single filers with taxable income up to $49,450, and married couples filing jointly up to $98,900, pay 0% federal tax on long-term capital gains. If your income falls in that range, you may be able to sell an appreciated position, recognize the gain at no federal tax cost, and repurchase it to reset your cost basis higher. A higher cost basis means less taxable gain when you eventually sell for good.

Both strategies use the timing of sales to your advantage, but they work in opposite directions. Here's how they compare.

Because the wash sale rule applies only to losses, tax gain harvesting carries one built-in advantage: you can sell an appreciated position to capture the gain and buy it back the same day, resetting your cost basis with no waiting period.

You can harvest tax losses at any time, but many investors do it near the end of the year, once they have a better read on portfolio performance and start planning their tax return. Starting in October or November is recommended to avoid the crunch of December’s tight deadlines.

Tax-loss harvesting has the potential to offer meaningful benefits, though the process is nuanced. Consulting qualified financial and tax professionals is essential to decide whether the strategy fits your situation.

It's selling an investment at a loss on purpose, then using that loss to reduce the taxes you owe on gains from other investments. Any unused loss can lower your ordinary income by up to $3,000 a year or carry forward to future years.

Tax-loss harvesting tends to help investors who have realized capital gains in taxable investment accounts and want to reduce their current tax bill. It can also be useful for investors who are rebalancing a portfolio, managing a large gain, or looking to offset up to $3,000 of ordinary income with net capital losses.

The strategy is generally most valuable when you have taxable gains to offset and enough flexibility to avoid a wash sale.

Yes. You can apply losses freely against capital gains, but you can only deduct up to $3,000 of net losses against ordinary income each year ($1,500 if married filing separately). Anything beyond that carries forward to later years.

No. Tax-loss harvesting is only relevant for taxable brokerage accounts. It doesn't apply to tax-advantaged retirement accounts, such as a traditional IRA, Roth IRA, or 401(k), because transactions within these accounts aren't subject to capital gains taxes.

Tax-loss harvesting sells positions below their cost basis to offset gains. Tax gain harvesting sells appreciated positions to realize gains while you're in a low or 0% capital gains bracket. One reduces taxable gains now; the other locks in gains at a low tax cost and resets your cost basis higher.

Ready to see how a tax strategy fits your bigger financial picture? Learn how our approach to investment management can help support your financial goals.

Explore how common investments are taxed, including when income, capital gains and withdrawals may be subject to taxes across different investment vehicles and accounts.

Let us help you craft a portfolio that reflects your goals, time-horizon and values.