Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

President Trump’s administration has sharply increased tariffs on most major U.S. trading partners.

Legal challenges may alter or overturn current tariff policies, with Supreme Court arguments beginning November 5.

Despite higher tariffs, U.S. equity markets and economic growth remain strong and resilient.

President Donald Trump is turning frequent tariff talk into tangible action. Throughout the summer and early fall, he implemented detailed tariff policies on U.S. imports from many nations, sharply increasing duties compared to longstanding trade practices. On October 10, U.S.-China trade tensions escalated as both countries imposed additional sanctions. China will restrict rare earth exports beginning December 1, while President Trump responded by threatening a 100% tariff rate and announcing software export controls starting November 1.

Higher tariffs’ full economic impact remains uncertain. Investors are questioning whether these changes will slow corporate profit growth, accelerate consumer inflation, weaken the labor market, or trigger a combination of effects. April’s initial tariff announcements caused a significant stock market decline, but equities have since rebounded. As the President clarifies his tariff plans by country and industry, markets have softened recently but remain near all-time highs, signaling continued confidence in the economy's overall direction.

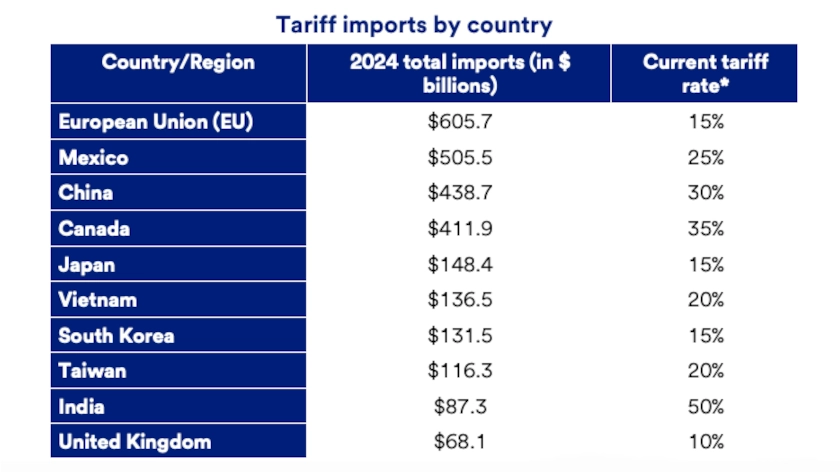

Most U.S. trading partners now face higher tariffs, including the largest exporters. Some tariffs are already in effect, but negotiators have not finalized all terms, and the administration could change agreements before they complete implementation and secure congressional approval in many cases. Nevertheless, America’s biggest trading partners now face much higher tariffs than before President Trump’s second term began.

Negotiations with three of the U.S.’s four largest trading partners, Mexico, China, and Canada, are ongoing, but the administration is already charging these countries higher tariff rates than in 2024. The U.S. continues talks with Taiwan, including a separate review of advanced semiconductors and electronics. The administration has resumed tariff negotiations with India after unilaterally raising rates to 50%, citing India’s continued Russian oil purchases and the administration’s desire to end the Russia-Ukraine war.

The U.S. and China continue to clash over trade negotiations. On October 9, China announced it will curb rare earth metal exports beginning December 1 and restrict battery manufacturing equipment starting November 8. These actions could harm U.S. manufacturers of computer chips, defense equipment, and battery technology. On October 10, President Trump threatened to impose new 100% tariffs on Chinese imports starting November 1. President Trump and President Xi of China intend to meet at the Asia-Pacific Economic Cooperation summit in Seoul on October 31–November 1 but escalating rhetoric may jeopardize their meeting.

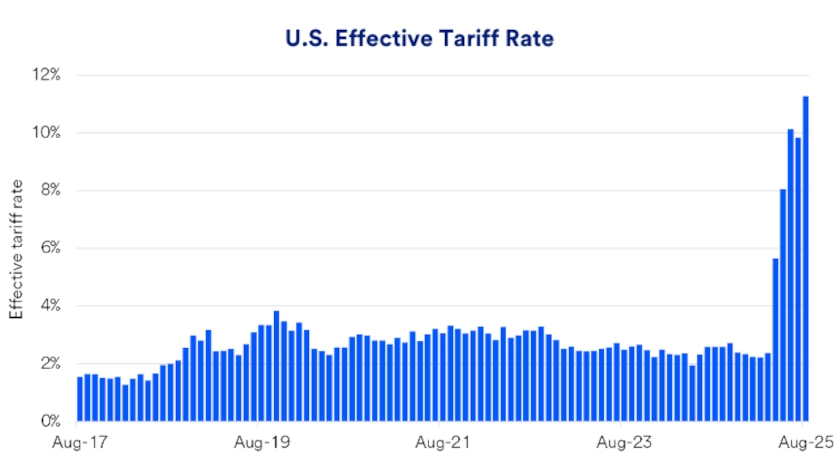

The administration continues to determine applicable tariff rates for countries and specific goods, but U.S. government tariff collections on imported goods have increased more than fourfold this year.

The Yale Budget Lab estimates that consumers could eventually face an average effective tariff rate of nearly 18% on imported goods – the highest effective U.S. tariff rate since 1934 1 – based on what’s been announced so far by the Trump administration.

Unlike traditional trade agreements, administration officials are negotiating deals that directly implement tariffs on trading partners without seeking Congressional ratification. While Congress has delegated some tariff-setting authority to the executive branch, states, importers, small businesses, and advocacy groups have challenged the legality of President Trump’s tariffs in court.

President Trump cites the International Emergency Economic Powers Act (IEEPA) to justify bypassing Congressional approval for many new tariff plans. In late August, a Federal Circuit appeals court upheld the Court of International Trade’s May decision that certain tariffs exceed the President’s authority, but the tariffs remain in effect during the appeal process. The Supreme Court has agreed to hear the administration’s appeal, consolidating two separate tariff lawsuits. Oral arguments begin November 5, and the court will ultimately rule on President Trump’s unilateral tariff strategy.

If the Trump administration loses its Supreme Court appeal, it may pursue alternative legal options, including:

“While President Trump’s approach faces legal challenges, the current administration will likely retain tariffs in some form,” says Bill Merz, head of capital markets research with U.S. Bank Asset Management Group.

From February through April, investors expressed significant concern about the new tariff policy’s economic ramifications. Stocks declined, but equity markets quickly recovered, and by mid-summer, the S&P 500 hit a series of new all-time highs. Stocks dropped after President Trump criticized China’s trade stance and proposed higher tariffs on October 10, but they remain close to record highs. 5

“Since April, investors have moved away from the idea that tariffs would have a particularly detrimental impact on economic growth and corporate earnings,” says Merz. “Investor sentiment shifted to a much more positive stance in a short period.”

After a modest decline early in the year, the U.S. economy grew at a robust 3.8% annualized rate in the second quarter, as measured by Gross Domestic Product. 6 The unemployment rate remains low at 4.3%, as of August, as the on-going government shutdown delayed the September employment report. While inflation remains above the Federal Reserve’s 2% target, August’s 2.9% year-over-year pace matches the start of 2025. 7

“Since April, investors have moved away from the idea that tariffs would hurt economic growth and corporate earnings.”

Bill Merz, head of capital markets research for U.S. Bank Asset Management Group

Meanwhile, strong corporate earnings growth continues to drive equity market momentum. Since reaching its 2025 low on April 8, the S&P 500 has risen more than 33%. 8

Resilient consumer spending and business investment benefit equity markets, and major companies continue to report strong profit growth. Investors remain concerned that higher tariffs could slow global activity and cause economic weakness, but so far, tariffs have not produced negative economic effects. Market fundamentals appear well-positioned for ongoing growth in the near-term pending Washington policies.

This may be an opportune time to connect with your wealth planning professional. Discuss your comfort level with your current portfolio in relation to ongoing economic changes, your personal objectives and your risk appetite.

Tariffs, also called import duties, are government-imposed levies on goods that enter the country from abroad. U.S. officials collect these tariffs when goods clear customs. The government sets tariff rates based on the product type and the country of origin. Often, the U.S. applies tariffs to specific products or countries to help domestic producers compete more effectively.

In international sales, the buyer or importer pays the tariff directly to their government. Importers may then raise the domestic price of the product to cover this cost, which can lead to higher consumer prices. As prices rise, consumer demand may change.

President Trump actively uses tariffs to address what he sees as unfair conditions for U.S. interests. During his first administration (2017–2021), he imposed tariffs, especially on China. In his second term, he has expanded tariffs to most trading partners, with rates ranging from 10% to 50%. This approach marks a clear departure from previous administrations, which favored open international trade.

Tariff actions and proposals in 2025 have visibly increased market volatility. For example, the S&P 500 saw a correction (a drop of 10% or more from its peak) over about three weeks. If the U.S. adds new tariffs and other countries retaliate, investors may worry about slower global economic growth. As Bill Merz of U.S. Bank Asset Management Group notes, “We know some tariffs will persist, but we don’t know how much is real, how much is negotiation, or when we’ll understand the full impact on consumer demand.” While markets await further tariff clarity, strong economic momentum continues to support higher trending equity prices.

The S&P 500’s recent rollercoaster performance has investors wondering what lies ahead for the stock market.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.