Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

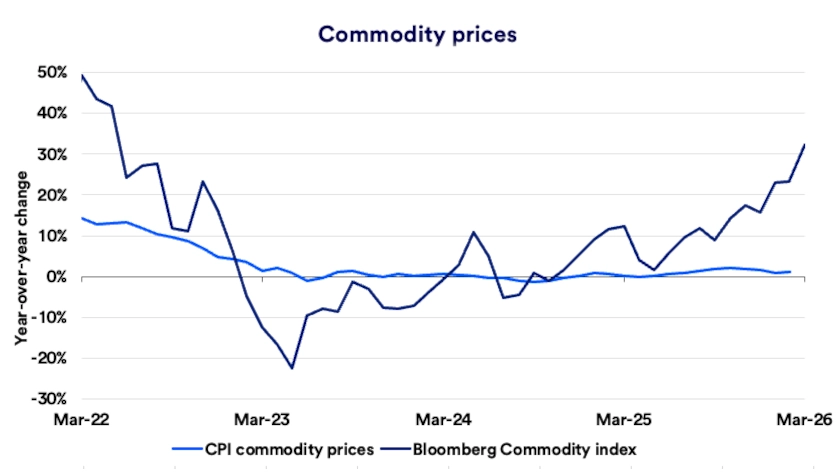

Commodities comprise more than one-third of the Consumer Price Index, a widely cited measure of inflation.

Rising broad commodity index prices haven’t spilled over to recent inflation readings yet due to how inflation indices are calculated.

Commodities may serve a tactical role in portfolios, but they can present challenges as long‑term investments.

Investors closely watch commodity prices because those moves can ripple into everyday costs and the inflation data that markets follow. In recent months, the Consumer Price Index (CPI) edged lower despite broader commodity index price gains. Energy prices, which represent just over 6% of CPI, rose modestly in 2025 and accelerated recently due to unseasonably cold weather and the Iran conflict. The CPI for energy commodities lost 2.9% in 2025 and fell further in January before rebounding in February. 1

Other commodities tell a slightly different story, with food prices gaining consistently over the past year. Food matters because families feel it quickly at the checkout line. Food price inflation in the CPI rose 3.1% year-over-year through February 2026, driven by higher beef and coffee prices tied to constraint supplies.1 Meanwhile gold and silver reached record highs in 2025 and helped lift broader commodity index gains, even though metals do not directly drive most CPI categories. 2 Together, these cross-currents leave a clear question: Will broad commodities continue rising in 2026, and how will they impact inflation?

Commodities make up 36% of the CPI, so broad price shifts can add up quickly. However, calculations for the CPI anchor mostly on energy and food prices, rather than broader, investable commodity indices, which include precious and industrial metals along with agricultural and energy commodities. After CPI peaked at 9.1% for the 12-month period ending June 2022, inflation declined significantly, and as of February 2026, stands at 2.4% for the previous 12 months. 1 While commodity cost in the CPI rose 1.3% for the same period, the Bloomberg Commodity Index, which captures a basket of consumer and industrial commodities, rose 16.7%, year-over-year through February and 27.1% through the end of March. 2

“The Iran conflict stopped nearly 20% of global oil supply from leaving the Strait of Hormuz, driving oil prices 50% higher in March. There’s significant concern for global oil importers getting sufficient oil to meet economic needs.”

Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group

In 2025, commodity prices reflected a mixed picture of demand, driving precious metals and livestock prices higher with ample supplies moderating energy prices and agriculture prices. In 2026, attention turned to the Iran conflict, which drove oil prices significantly higher, though precious metals prices sagged. Shifting investor sentiment likely pushed different commodity prices in distinct directions at the same time. “The Iran conflict stopped nearly 20% of global oil supply from leaving the Strait of Hormuz, driving oil prices 50% higher in March,” says Rob Haworth, senior investment strategy director for U.S. Bank Asset Management Group. “There’s significant concern for global oil importers getting sufficient oil to meet economic needs. However, geopolitical uncertainty did little to help precious metals, including gold and silver after strong rallies in 2025.”

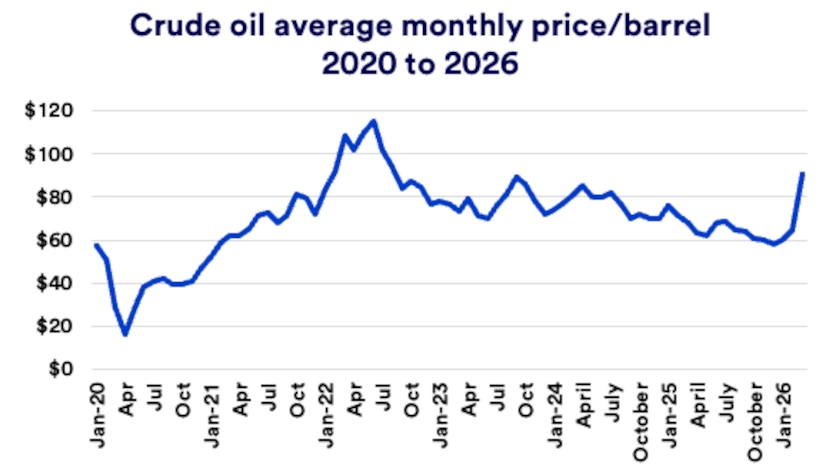

Energy prices often swing with headlines because global events can change supply and demand quickly. Since 2020, crude oil ranged from a low of just above $10 per barrel early in the COVID-19 pandemic to as high as $120 per barrel after Russia’s 2022 invasion of Ukraine. 3 “Lately, prices have again spiked above $100 per barrel after U.S. strikes on Iran, after touching the mid-$50’s in December,” says Haworth.

The central market issue is the effective disruption of shipping through the Strait of Hormuz, a critical energy corridor with limited near-term alternatives. The U.S. Energy Information Administration (EIA) estimates that roughly 20% of global oil supplies and global liquefied natural gas (LNG) transited the strait in 2024. 4 The Bab el-Mandeb strait adds another layer of risk because it carries about 12% of global trade and can amplify transportation costs and delivery delays if disruption spreads. 5

Markets have responded quickly to the surge in energy prices. The recent equity selloff reflects sharp moves in oil and natural gas, with WTI crude oil and wholesale gasoline prices up more than 70% from the start of the year. Those price gains have renewed investor concern that inflation could reaccelerate just as growth slows.

The Strait of Hormuz also matters beyond oil and natural gas. Fertilizer shipments that move through the region affect agricultural input costs, and the Fertilizer Institute (TFI) reports that nearly 50% of nitrogen-based fertilizer exports originate from countries west of the strait and typically travel through this route. When shipping slows, fertilizer availability can tighten, raising farming costs and contributing to food price inflation over time, especially in import-dependent regions.

Agriculture and livestock prices jumped 4.7% in March, according to the Bloomberg Agriculture and Livestock Commodity Index, reflecting higher fertilizer costs and supply fears as we enter a key growing season in the Northern Hemisphere. Persistence of higher costs implies food inflation is likely to remain stubbornly elevated.

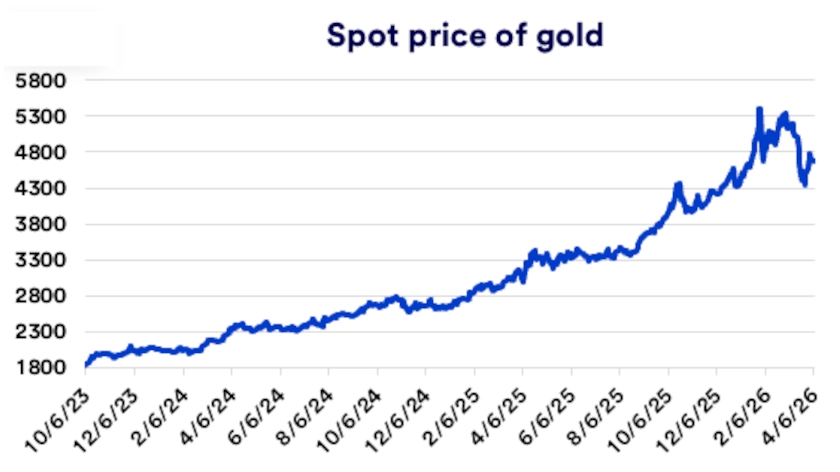

A doubling in silver prices and a 62% gain for gold helped drive a 15.7% increase in the Bloomberg Commodity Index in 2025. 2 Broad index gains continued into February and accelerated during the Iran conflict in March, despite reversals in gold and silver prices, leaving many investors to wonder whether precious metals offered a chance to invest – or a warning sign. By the end of March, gold fell nearly 20% from its January record high while silver dropped 40%, highlighting how quickly enthusiasm can turn into volatility. 2

Gold climbed steadily over the course of 2025, starting just over $2,600 per troy ounce and closed out 2025 around $4,320 per ounce. In 2026, gold surged to more than $5,418 on January 28 before speculation faded and prices slipped below $5,000. 2 A key driver of rising gold prices in 2025 was investor inflows much higher than previous years. Larger investor participation can also result in higher volatility as investor sentiment shifts as we saw in early 2026.

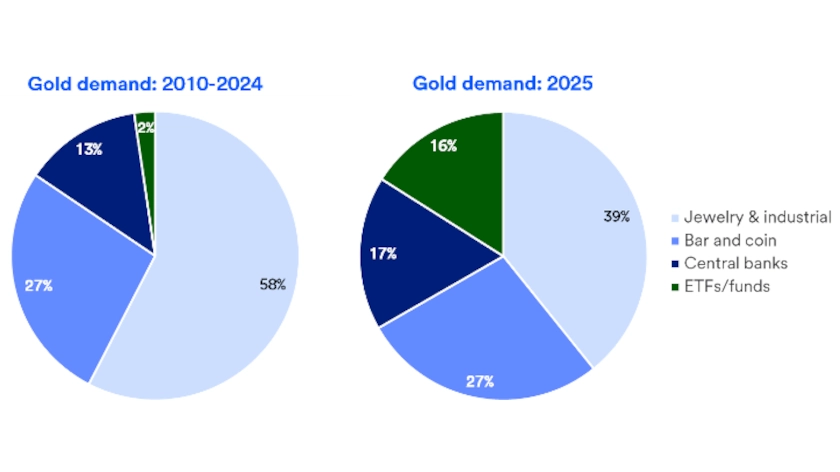

In 2025, gold demand shifted from its historical pattern. Global central bank and investor demand from exchange-traded products increased significantly. 6 A key question for future price gains is whether these investors will continue to pursue additional gold holdings at prices 90% higher than where they started in 2025.

Silver moved even faster. After faltering in early April, silver surged past its 1980 all-time high of $50 per troy ounce in October, closed the year above $70/oz for a 140% annual gain, then neared $120/oz at the end of January before sliding 40% over the next week as the speculative furor ebbed. 2

Commodities can play a role in a broader plan, but the path can be uncomfortable when prices jump around. “The challenge,” according to Haworth, “is that when you invest in a specific commodity, you have to get both decisions right – buying it cheap enough and having the ability to sell it at a higher price.” He also notes that investors are not “paid” in the form of income while they wait for price appreciation, which is one reason he views commodities as more effective for tactical use than a long-term portfolio centerpiece. “It’s difficult to earn a durable return with direct investments in commodities or commodity futures,” Haworth admonishes.

Investors should prepare for frequent changes – both higher and lower – in commodity prices, especially when trade uncertainty, supply constraints, and shifting demand dynamics compete for attention. “While precious metals prices can rise in conjunction with inflation, the recent upturn in the face of slowing inflation reflects a spike in speculative demand as investors face risks such as trade uncertainty and elevated equity market valuations,” says Haworth. For silver, he also points to supply concerns and stronger demand from electric vehicles and data centers, while noting that large drawdowns often require time before prices attract more fundamental demand.

Talk with your financial professional about the appropriateness of a commodities position in your portfolio.

Commodities represent a wide range of assets, including everything from energy and agricultural products to precious and industrial metals. Prices of different commodities can vary, though all tend to be affected by factors such as production levels (supply) and consumer and business demand. Economic factors also tend to come into play. For instance, during global economic recessions, energy demand tends to subside, often driving prices lower.

Typically, changes in commodity prices can drive inflation trends. According to the U.S. Bureau of Labor Statistics, commodities make up 36% of the Consumer Price Index, the most watched inflation measure. When inflation began to surge in 2021 and 2022, higher commodity prices, such as for food and gasoline, played a big role. When inflation numbers improved after peaking in mid-2022, declining energy prices and slowing food costs also played an important role.

Investors sometimes consider including commodities in a portfolio to hedge the impact of higher inflation. But it can be difficult to earn a durable return with direct investments in commodities or commodity futures. Investors must be aware that commodities tend to be a volatile asset class, and it is difficult to choose the right time to invest when prices can shift significantly in a short period of time. One effective way to capitalize on today’s commodities market is through investments in infrastructure. This includes companies involved in oil pipelines, airports, cell towers, toll roads and other forms of infrastructure. Along with capital appreciation potential, these investments also tend to provide a regular income stream.

There are multiple ways to invest in commodities, but the risks are high and the returns are unpredictable.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.