Capitalize on today’s evolving market dynamics.

With markets in flux, now is a good time to meet with a wealth advisor.

Fed rate cuts and fiscal stimulus have boosted stocks and supported corporate earnings.

Defensive sectors have lagged this year, while technology and utilities have posted strong gains.

Interest rates and inflation trends will continue to shape equity market performance.

Interest rates directly shape bond markets, but their influence also extends to equity markets. They determine borrowing costs for the government, consumers and businesses. When borrowing costs rise, corporate profitability can suffer, potentially slowing corporate earnings growth and reducing returns. Conversely, lower interest rates and borrowing costs typically support stronger stock market returns.

Investors closely monitor interest rates and the Federal Reserve (Fed) because these factors impact stock market earnings. The Fed sets short-term interest rates through its target Federal Funds rate, which impact longer-term interest rates and borrowing costs throughout the economy. Changes in these rates can quickly ripple through both bond and equity markets.

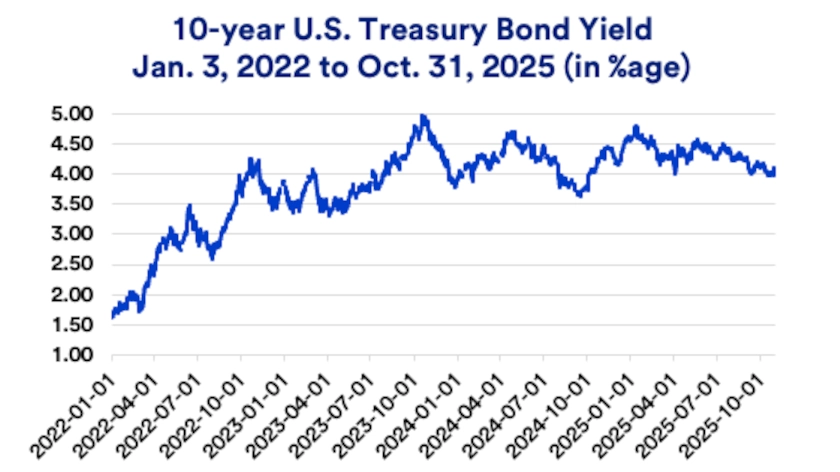

Interest rates remained elevated compared to the past decade but have declined in recent weeks as investors anticipate multiple Fed rate cuts. For the past two years, the 10-year U.S. Treasury note yield has moved within a broad trading range from 3.6%-5%. 1 “Despite the highest interest rates in a decade, solid corporate earnings growth supports equity prices,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group. The S&P 500 recently reached new all-time highs, rebounding from early-year volatility when stocks dropped nearly 20%. 2

Currently, the 10-year U.S. Treasury yield remains near 4%, 1 and Terry Sandven, chief equity strategist with U.S. Bank Asset Management Group, notes that steady to somewhat lower rates benefit stocks. “Relatively stable inflation, rangebound to lower interest rates and rising corporate earnings support stock prices,” says Sandven. By late October, the S&P 500 hit new all-time highs again this year. 2

Fiscal stimulus from the recent “One Big Beautiful Bill Act” provides gives stocks an extra boost. The legislation improves the corporate earnings outlook by increasing deductions and lowering corporate taxes, while individuals could see lower taxes in 2026. These changes, combined with lower borrowing costs as the Fed reduces interest rates, help support corporate profits.

The Fed has actively reduced the federal funds target rate, cutting it by 1% in late 2024 and by 0.25% in both September and October 2025. The fed funds target rate now stands between 3.75% to 4.00%. “Investors anticipate one more 0.25% rate cut at the Fed’s December meeting and three more cuts in 2026. Rate cut expectations have lifted stocks and pushed bond yields toward the lower end of their recent range,” says Bill Merz, head of capital markets research for U.S. Bank Asset Management Group.

"Investors anticipate one more 0.25% rate cut at the Fed’s December meeting and three more cuts in 2026. Rate cut expectations have lifted stocks and pushed bond yields toward the lower end of their recent range.”

Bill Merz, head of capital markets research for U.S. Bank Asset Management Group

In January, 10-year Treasury bond yields reached 4.8% but have not exceeded 5.0% since 2007. President Donald Trump’s higher tariff proposals and the U.S. government’s rising debt levels contributed to bond market volatility. However, by mid-year, rates settled into a trading range mostly between 4.0% and 4.5%. 1

“The 10-year Treasury yield acts as a signal for equity investors,” says Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group. “A rate near 4% reflects shifting expectations, and currently, lower bond yields result from anticipated rate cuts amid rising growth forecasts,” he notes. “Falling interest rates and bond yields can also indicate a slowing economy if economic data were to deteriorate, which isn’t favorable for stocks. But we don’t foresee a slowing economy right now.” According to Hainlin, at yields of 5% or higher, bonds compete more strongly with equities and higher borrowing costs can weigh on stock prices.

Sector performance has varied this year. Early in the year, stocks that dominated markets in the previous two years, including information technology, communication services and consumer discretionary, all fell into negative territory. In contrast, energy, healthcare, consumer staples, utilities, and real estate stocks outpaced the broader market.

Year-to-date returns paint a slightly different picture. Communication services, information technology and utility sectors have performed best, each posting 20% or higher gains so far in 2025. Meanwhile, traditionally defensive categories like healthcare and consumer staples have lagged. 3

“Typically, falling interest rates help income-oriented, defensive sectors such as utilities, energy and real estate perform well,” says Sandven. “Notably, utility stocks performed well so far in 2025, but other interest rate sensitive sectors have lagged.” Sandven attributes strong utility performance largely to burgeoning data center development, which drives rapid power demand growth with positive investor sentiment accruing to utilities companies serving those power needs.

Interest rates remain a crucial factor for equity investors. “The Fed doesn’t plan on returning to the pre-2022 ‘zero interest rate’ environment,” says Haworth. “Inflation may stabilize at a higher level, around 2.5% to 3.0%, which could lead the Fed to ultimately set the federal funds target rate close to 3.0% compared to the current rate of 3.75% to 4.00%.” Given present interest rate trends, Haworth believes solid economic fundamentals and strong corporate earnings keep equities well positioned for growth.

As you review your portfolio, prepare for possible short-term stock price fluctuations. Stocks should remain a key component of any long-term investor’s diversified portfolio. “Stocks are an important contributor to long-run portfolio returns, and can help investors keep pace with inflation,” says Haworth.

Talk with your wealth professional about your comfort level with your portfolio’s current investment mix. Discuss whether any changes are appropriate in response to evolving capital market conditions, consistent with your goals, risk appetite and time horizon.

Note: The Standard & Poor’s 500 Index (S&P 500) consists of 500 widely traded stocks that are considered to represent the performance of the U.S. stock market in general. The S&P 500 is an unmanaged index of stocks. It is not possible to invest directly in the index. Past performance is no guarantee of future results. The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index and is representative of the U.S. small capitalization securities market. The Russell 2000 is an unmanaged index of stocks. It is not possible to invest directly in the index. Past performance is no guarantee of future results.

Interest rates directly influence investor decisions in the stock market. When rates rise, investors often shift their money into bonds because these now offer more attractive yields than before. As a result, companies must work harder to deliver stronger earnings to keep investors interested, and higher borrowing costs can reduce profits, which may lead to lower stock prices.

When the Federal Reserve raises the short-term federal funds target rate (as it did in 2022 and 2023), stocks often face immediate challenges. A higher interest rate environment tends to slow business activity and can negatively impact the economy. As corporations experience lower revenues and earnings, their stock prices may decline in response.

Stock market movements do not directly determine the direction of interest rates. Instead, economic conditions and inflation play a much larger role in determining the direction of interest rates. When stock prices fall, investors may seek safer investments like bonds, increasing demand for bonds and allowing issuers to offer debt at lower interest rates.

The S&P 500’s recent rollercoaster performance has investors wondering what lies ahead for the stock market.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.