Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

China economy growth has cooled, but remains central to global trade, supply chains and market sentiment.

China stock market performance improved in 2024 and 2025 but remains below its 2021 peak amid trade, property and energy risks.

Investing in China may fit best through diversified emerging market funds that spread exposure across countries, sectors and currencies.

China remains a major force in the global economy, even as growth has cooled from the rapid pace investors remember from the 2000s. China’s economy grew 5.0% in the first quarter of 2026 compared with a year earlier, an improvement from fourth quarter’s slowest annual pace in three years. 1 China still ranks as the world’s second largest economy after the United States, which keeps it central to global trade, supply chains and market outcomes. 2

Investors should not frame China’s economy as simply “up” or “down” in any single quarter. The more useful question is how China’s shifting growth pattern is influencing the rest of the world. When China buys less, sells more, or redirects supply chains, the effects can reach manufacturers, commodity markets, shipping routes, and corporate profits.

U.S.-China trade policy remains a major swing factor for business planning and investor confidence. President Donald Trump's administration reframed U.S.-China trade relations last year by imposing escalating tariffs on Chinese imports. After several rounds of negotiations, the two countries reached a one-year trade agreement on November 1, 2025 that helped stabilize trade relations deep into 2026, with the U.S. reducing certain tariffs and China resuming regular purchases of U.S. soybeans while pausing rare earth export controls.

At a highly anticipated two-day summit that concluded on May 15, 2026, President Trump and China’s President Xi Jinping did not jointly announce specific trade deals. They instead emphasized a shared vision for “strategic stability,” including agreeing that shipping through the Strait of Hormuz should resume. That message may help lower near-term uncertainty, but companies still face a changing trade landscape that requires ongoing supply chain adjustments.

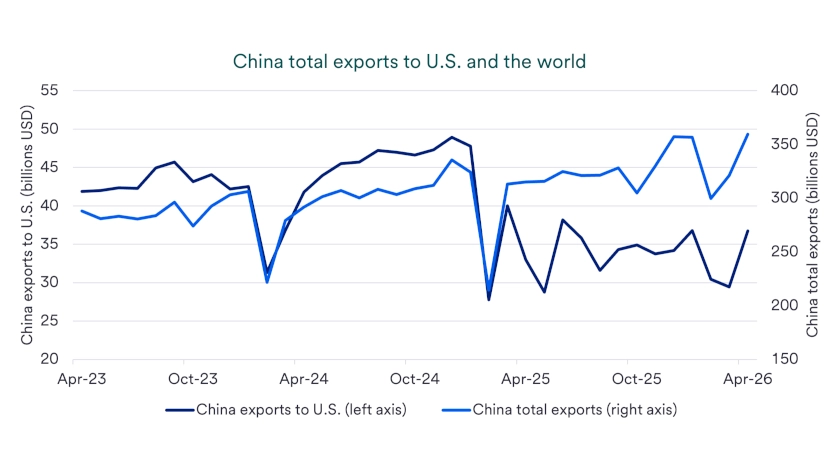

China built much of its modern economic rise on exports, pairing low-cost production with large infrastructure investment and a growing skilled workforce. Those strengths helped expand China’s middle class and supported years of faster growth, but they also left the economy sensitive to changes in trade access. Entering 2025, the U.S. was the largest customer for Chinese goods, which helps explain why shifts in U.S. demand and policy can quickly show up in shipping and factory activity. 1

Today, China is working to offset weaker U.S. demand by selling more to other regions, while also trying to protect jobs at home. “China hopes it can replace U.S. business by stepping up exports to other countries,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group. China increased total exports by 5% in 2025 versus 2024, as gains across Asia, Africa, Europe, and Latin America helped offset a 20% decline in exports to the U.S.

That trend has become more pronounced in 2026. China’s exports through April rose 14.5%, while exports to the U.S. contracted by another 10%. 1 For investors, the change points to a more complex global trade map, where China remains a major exporter but relies less on one large end market than it did in the past.

China’s property downturn began in 2021 and continues to pressure economic growth and consumer confidence. 1 Housing traditionally served as both a place to live and a major store of household wealth. Years of rapid building and easy credit created too much supply, pushed prices lower and slowed construction activity.

The property sector played an outsized role in China’s earlier expansion, accounting for nearly one third of economic growth. 3 A long adjustment period can therefore affect jobs, consumer spending and household wealth. Lower home prices can also make households more cautious, especially when families hold a large share of savings in property.

Recent consumer trends show that caution remains in place. Retail sales grew 2.4% in the first quarter of 2026 compared with a year earlier, up from the prior quarter’s 0.7% growth pace but well below the 11% average since 2000. 1 “Stimulus measures are boosting consumer spending, but savings are also rising,” says Haworth. “Even though the economy isn’t accelerating, it is still growing.”

Other indicators point to a slower pace of activity. Consumer inflation rose 1.2% year-over-year in April, while 10-year government bond yields stood at 1.75% as of May 18, 2026. 1 Low inflation and low bond yields often align with softer growth expectations because they suggest muted demand and investor caution.

Investors also face limits in assessing China’s economy, because some economic data are not consistently available to the public. Youth unemployment is one example, and gaps in key data can make it harder for investors and businesses to assess conditions in real time. When important indicators are missing or delayed, investors need to rely on a broader set of signals to judge where China’s economy is strengthening and where pressure remains.

China’s stock markets have faced a difficult stretch for much of the 2020s. The MSCI China Index posted a three-year losing run from 2021 to 2023 before rebounding in 2024. A weaker U.S. dollar then helped lift 2025 returns by increasing the value of China equity market gains when translated back into dollars. 1

“Any investor who puts money to work in a broad, emerging market index owns a meaningful position in Chinese stocks.”

Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group

China’s stock market has come under renewed pressure in 2026. As of May 18, the market declined 5.99% as the US-Iran conflict and the closure of the Strait of Hormuz highlighted China’s dependence on imported Middle Eastern oil. Even after the 2024 and 2025 rebound, China’s equity market remains 17% below its February 2021 peak. 1

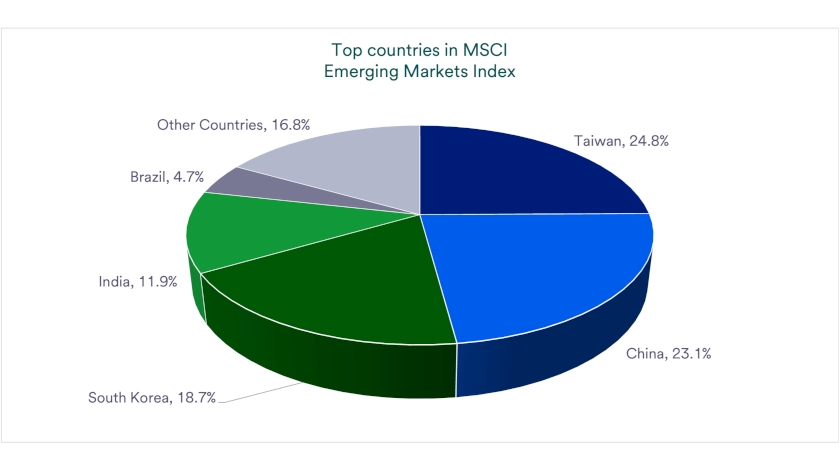

China also remains hard to avoid in many global portfolios because of its weight in widely used emerging market benchmarks. Investors still classify China as an emerging market, and the country holds the second-largest single-country share in the MSCI Emerging Markets Index at 23%. 4 “Any investor who puts money to work in a broad, emerging market index owns a meaningful position in Chinese stocks,” says Haworth.

Emerging markets have recently delivered stronger performance relative to developed international markets. In 2024, the MSCI Emerging Markets Index returned 7.5% including dividends, nearly double the return of the MSCI EAFE developed markets index over the same period. Emerging markets still trailed U.S. stocks that year, as the S&P 500 gained 25.0%. 1

Performance broadened further in 2025 and into early 2026. Emerging markets gained 33.6% in 2025 compared to 17.9% for the S&P 500. Year-to-date through May 18, 2026, emerging market stocks are up 19.2%, helped by strong technology demand, compared with a 8.6% gain for the S&P 500. 1

This broader performance backdrop gives investors more ways to think about international diversification. China remains a large part of the emerging market exposure, but it is no longer the only story. Taiwan, South Korea, India, Brazil and other countries also contribute to the opportunity set, which can help investors spread risk across different economies and industries.

International stocks can strengthen diversification because they may not move in lockstep with the U.S. market. “Global stocks offer an attractive investment opportunity to manage risk from elevated U.S. equity values and trade uncertainty,” says Haworth. This approach focuses less on predicting short term headlines and more on spreading exposure across different economies, currencies and business cycles.

Haworth favors taking China exposure through broad emerging market funds rather than trying to pick narrow slices of the market. Broad funds can reduce the risk of concentrating too heavily in one country while still recognizing China’s size in the global system. They can also give investors exposure to a wider set of industries, manufacturing and technology exporters that have grown outside the United States.

“Today, compared to the past, we find more manufacturing and technology exporters across emerging market economies,” says Haworth. “Many of these manufacturers outside of China may benefit from U.S.-China trade fallout.” The practical takeaway is to match any change to your goals, time horizon and comfort with risk, and to work with your U.S. Bank wealth professional to confirm whether emerging market stocks, including China exposure, fit your plan.

China’s economy is often described as a “socialist market economy.” China has added more free-market elements in recent decades, but the central government still controls large parts of China’s economy through many state-owned enterprises. China also has a large private sector that has grown rapidly in recent decades, sometimes with government support. In past decades, China’s economy, as measured by Gross Domestic Product (GDP), often grew by 10% or more per year. Growth remains solid, but GDP expansion has slowed more recently to the 5% range. 1

China significantly influences Asian markets because it is the region’s largest economy. China, Taiwan and India are among the most prominent emerging market countries and carry large weights in many emerging market equity indices. From a global perspective, China has the second largest economy after the United States. It accounts for nearly one-fifth of the global economic output, as measured by GDP adjusted for differences in purchasing power.

China’s market influence has expanded rapidly in recent decades and continues to draw investor attention. Many global businesses have increased their focus on selling to Chinese consumers and businesses, which links China’s economic health to corporate earnings for international firms. From an equity market perspective, China represents nearly one-quarter of the MSCI Emerging Market Index’s market capitalization. China also produces roughly one-third of the world’s manufactured goods. Because the country consumes large amounts of industrial metals and other raw materials, shifts in China’s growth often influences commodity prices.

China’s economic growth has been rapid in recent decades, but the sources of that growth have changed over time. For many years, the government invested heavily in housing, roads, rail systems and other large projects. China now places greater emphasis on high-tech manufacturing, including electric vehicles, solar energy materials and lithium-ion batteries. At the same time, the property sector remains a challenge because years of overbuilding resulted in large amounts of vacant space. That excess supply has weighed on prices, rents and credit quality tied to real estate. China also continues to rely heavily on exports, while domestic consumer spending plays a smaller role in economic expansion.

China’s economy continues to evolve. Beginning in the 1980s, China’s rise depended heavily on assembling consumer goods, including electronics, at very low prices and shipping large volumes abroad. That new source of low-cost industrial production helped fuel a long period of low global inflation. More recently, some low-cost production has shifted to other countries, China’s exports now focus more on advanced sectors, including electric vehicles, telecommunications equipment and solar infrastructure. This shift could give China more influence over global supply chains, business investment and trade relationships.

Global economic trends can shift quickly, but larger economies usually change more slowly. In economies as large as the U.S., China, or the European Union, major structural transitions can take decades. Several factors can extend the transition period, including the shift to new energy sources, the useful life of existing equipment, supply chain limits and the need to train workers for new roles. These constraints do not prevent change, but they often shape the pace of change. For investors, gradual transitions can create both risks and opportunities as industries, companies and countries adapt at different speeds.

Note: Investing in emerging markets may involve greater risks than investing in more developed countries. In addition, concentration of investments in a single region may result in greater volatility. International investing involves special risks, including foreign taxation, currency risks, risks associated with possible differences in financial standards and other risks associated with future political and economic developments.

Global economies are closely connected, and many U.S. companies rely on products or components that come from China. When China’s economy slows sharply or faces disruptions, supply chains can tighten and that can pressure profits for companies that depend on those inputs, as the COVID 19 period illustrated. China also influences global markets because it is the world’s second largest economy, and trade tensions such as tariffs can add uncertainty that investors may quickly price into U.S. stocks.

China is the world’s second largest economy, trailing only the United States. Some forecasters expect China could eventually surpass the U.S. in total economic output, but that is not certain and depends on future growth. One way to compare living standards is output per person, and the International Monetary Fund estimates that in 2025 China’s GDP per capita was $13,870 versus $89,680 for the U.S. 2

International stocks can play an important role in long term diversification because different countries can lead at different times. “Given today’s market risks, it makes sense to allocate a portion of equity assets into non-U.S. stocks, including emerging market stocks,” says Haworth. For many investors, a broad fund that includes China alongside other emerging markets can provide exposure while also spreading risk across multiple countries rather than relying on a single market.

The S&P 500’s recent rollercoaster performance has investors wondering what lies ahead for the stock market.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.