Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Hedge funds pool investor capital and use flexible strategies across liquid and illiquid securities.

Hedge fund strategies may diversify portfolios, but they can carry high risk, fees, tax complexity and liquidity limits.

Qualified investors should evaluate hedge fund structure, manager experience, performance goals and portfolio fit with a financial professional.

Hedge funds are alternative investments that can help qualified investors diversify beyond traditional stocks, bonds and mutual funds. A hedge fund pools money from individuals and organizations, then invests across a wide range of liquid and illiquid securities. These strategies can pursue higher return potential and broader diversification, but they also carry added complexity, higher risk and eligibility requirements.

Hedge funds do not fit every investor. Rob Haworth, senior investment strategy director for U.S. Bank Asset Management, says, “These are more complex strategies, so investors have to be aware that in trying to ramp up returns, they may be taking on more risk.” He adds that “more assertive investors may benefit most,” making risk tolerance, investment goals and time horizon important starting points before considering a hedge fund allocation.

A hedge fund is an investment vehicle that pools money from multiple investors and invests across different securities and markets. Hedge funds first came into existence in the 1940s, when wealthy investors sought assets that did not closely track traditional investments.

“It’s important to recognize the large variation among hedge fund strategies. You should carefully assess your options and try to find the most appropriate strategy to fit your portfolio.”

Rob Haworth, senior investment strategy director, U.S. Bank Asset Management

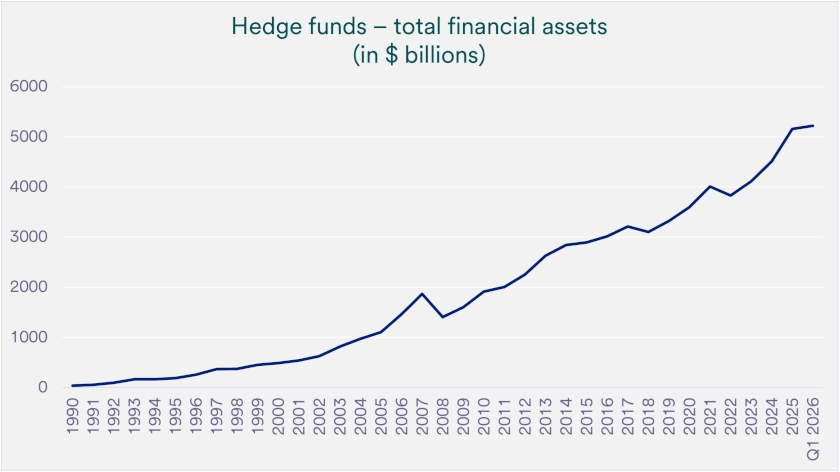

The industry has grown significantly, with more than $5 trillion invested as of March 31, 2026, according to HFR Global Hedge Fund Industry Report data.

Hedge funds fall under the broader category of alternative investments because managers often use more flexible strategies than traditional stocks, bonds or mutual fund managers. Until recently, hedge fund access largely belonged to pension plans, large institutions and investors with millions of dollars to invest. Regulatory changes have expanded individual hedge fund access, but hedge funds still require careful evaluation because strategies, risks and liquidity terms can vary widely.

Haworth says investors may find value in hedge funds but emphasizes the importance of selectivity. “It’s important to recognize the large variation among hedge fund strategies,” he says. “You should carefully assess your options and try to find the most appropriate strategy to fit your portfolio.”

Investors generally must meet eligibility requirements before investing in a hedge fund. These requirements vary by fund and follow Securities and Exchange Commission guidelines. Individual investors typically need a high net worth, a significant amount of investable assets or other qualifying characteristics before they can participate.

Eligibility alone does not make a hedge fund appropriate. Many hedge funds qualify as high-risk investments, and investors should understand both the potential benefits and the potential losses. “Hedge funds tend to be very complex, so it’s important to understand what you own and why you own it,” says Haworth.

A hedge fund manager, either an individual or a firm, directs the fund’s investment strategy and day-to-day operations. The manager decides how to allocate capital across securities, markets and trading strategies. Because hedge funds often give managers significant flexibility, experience, process discipline and risk management matter.

Haworth notes that some managers have demonstrated meaningful value through their track records, while others have not established extensive or competitive histories. Investors should expect their financial professional to evaluate hedge fund sourcing, due diligence, stated risk targets and expected performance objectives. That review should also consider whether a fund fits the investor’s goals, constraints and overall portfolio strategy.

Manager research also requires ongoing monitoring. Financial professionals evaluating hedge funds need industry knowledge, dedicated resources and time to assess new fund launches, closures and strategy changes. That process helps investors look beyond headline performance and focus on manager discipline, risk controls and portfolio fit.

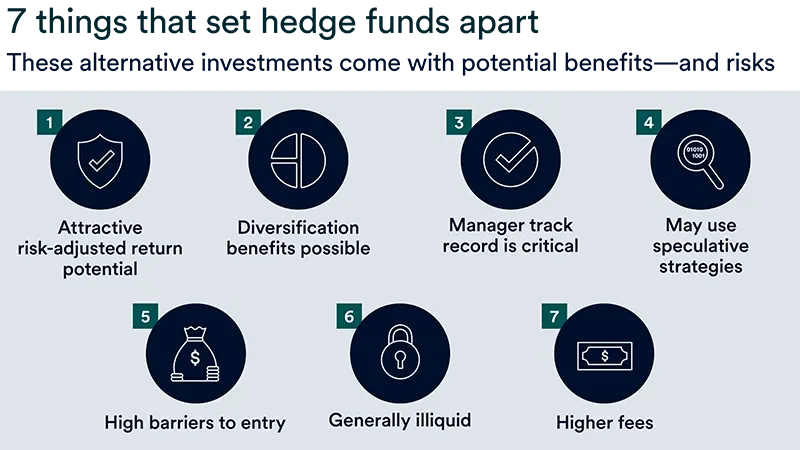

Hedge funds may offer attractive risk-adjusted returns, which means investors evaluate return potential relative to the amount of risk taken. Many hedge funds emphasize their ability to generate competitive returns while managing market volatility. For investors, the goal is not simply higher returns, but higher return potential with a risk profile that fits the portfolio.

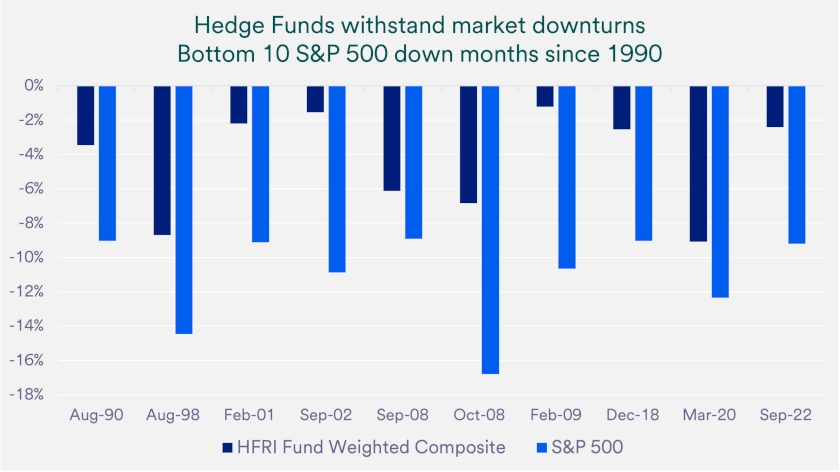

Hedge funds may also provide diversification benefits during down markets. The HFRI Fund Weighted Composite, a measure of hedge fund performance, has shown less severe declines than the broader stock market during some periods when the S&P 500 sustained significant losses. Past performance does not guarantee future results, but that history helps explain why qualified investors may consider hedge funds as part of a broader diversification strategy.

Hedge funds can adjust market exposure more flexibly than many traditional funds. Some strategies may seek to capitalize on a strong market by borrowing money to invest more than 100% of the portfolio in equity exposure, while others may hold less than full market exposure to help protect capital. This flexibility can help managers respond to different market environments, but it also increases the importance of understanding the strategy before investing.

Many hedge funds also use short selling, which allows a manager to seek gains when a security declines in value. Short selling can help a manager express a negative view on a stock, bond or other security. Some long/short mutual funds may also use short selling when their prospectus permits it. 1 The strategy can add flexibility, but it can also increase risk if the security rises instead of falls.

Hedge fund managers can pursue opportunities across bear markets and bull markets, which refer to falling and rising market environments. They may invest across security types, economic sectors and geographic regions using specialized strategies. This broad opportunity set can help managers seek returns from multiple sources rather than relying only on broad stock market gains.

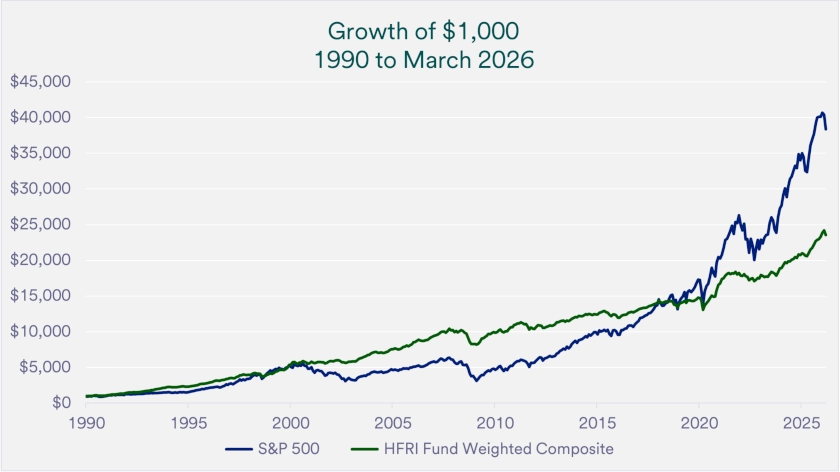

From 1990 to 2026, hedge funds generally tracked with equity markets while managing portfolio risk that helped mitigate losses, based on HFR and FactSet Research Systems data. During major stock market declines, including the early 2000s dotcom bubble, the 2008 financial crisis and the 2020 COVID-19 correction, hedge funds produced more stable performance than broad equities in the data reviewed.

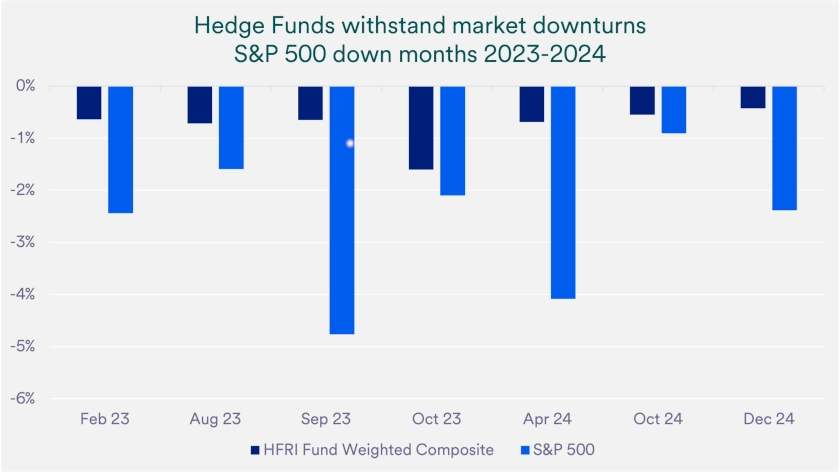

Performance results from 2023 and 2024 provide a more recent example of how hedge funds may limit the impact of down months. Stocks performed well overall during that period, but equities still declined in seven different months. In each of those months, hedge funds, represented by the HFRI Fund Weighted Composite Index, limited losses relative to broader stock market declines.

A long-term comparison of $1,000 invested in hedge funds, represented by the HFRI Fund Weighted Composite, and $1,000 invested in the S&P 500 Index illustrates how performance leadership can shift across market cycles.

Hedge funds outperformed stocks until 2020, while the S&P 500 later gained ground after posting total returns above 25% in both 2023 and 2024. Hedge funds did not keep pace during those unusually strong equity years, but they may be better positioned for periods when volatility rises and market leadership narrows.

This comparison highlights a key trade-off. Hedge funds may help reduce the impact of some down markets, but they may trail broad stocks during periods of strong equity performance. Investors should evaluate hedge fund performance in context, including the strategy’s purpose, risk level, fees, liquidity terms and role within the broader portfolio.

Hedge funds are widely viewed as high-risk investments, and investors should understand the risks before committing capital. Managers often have broad flexibility in how they structure portfolios, which can lead to speculative strategies. Short selling, leverage and derivatives can all increase risk, even when managers use them with the goal of managing or moderating risk.

Hedge funds also tend to carry higher fees than many traditional investments. Many funds charge a management fee of 1% to 2% annually, regardless of performance, plus performance fees that often range from 15% to 20% of annual profits. “You want to be selective in choosing a hedge fund to include in your portfolio and be certain you are being adequately compensated in terms of return potential for the costs you bear,” says Haworth.

Hedge funds generally work best as long-term investments because they may limit investor access to capital. Common liquidity restrictions include lockup periods, withdrawal gates and side pockets. Lockup periods can prevent investors from liquidating shares, withdrawal gates can limit or halt redemptions during certain periods, and side pockets can restrict access to certain holdings until managers can value or sell them appropriately.

These liquidity tools can become especially important when investor redemption terms do not match the liquidity of the fund’s underlying securities during periods of market stress. Investors should understand how quickly they can access their money, what conditions may limit withdrawals and how those terms affect portfolio planning. Liquidity risk deserves close attention because hedge funds can differ meaningfully from mutual funds or exchange-traded funds that typically offer daily liquidity.

Tax reporting can also become more complicated with hedge funds. Money held in taxable accounts may face short-term or long-term capital gains taxes or other investment tax considerations. Hedge fund investors also receive a Schedule K-1 each year, and those forms often arrive after the standard April 15 tax filing deadline, which may require investors to file a tax extension.

Haworth says investors should recognize that hedge fund tax reporting can differ from what they may know from traditional investments. “It’s important that investors are aware hedge fund tax reporting can be more complicated than what they’ve become accustomed to with more traditional investments,” he says. Investors should consult tax and legal advisors when assessing how hedge funds fit their personal tax situation.

Hedge funds use many investment strategies, so due diligence plays a central role in evaluating whether a fund belongs in a portfolio. Investors should look for a strategy with a strong performance and risk management record, but they should also determine whether the approach fits their specific investment objectives. Six broad hedge fund strategy categories include equity sector hedge, long/short credit, event driven, relative value, global macro and managed futures.

This is the most common strategy and comprises of equity long/short funds. It involves buying undervalued stocks (long positions) and selling stocks considered to be overvalued (short positions). By using hedging strategies, a fund can often limit volatility compared with its competitive stock index. “Sector hedge fund strategies may look particularly appealing based on recent performance,” says Haworth. “We’re seeing a wide dispersion in performance among stocks within sectors such as information technology and health care.” That dispersion, which means a wider gap between stronger and weaker performers, can create opportunities for long/short managers to profit from winners and losers within the same sector.

Long/short credit funds take both long and short positions in the bond market. Returns can come from coupon payments, capital appreciation in long positions or capital depreciation in short positions. These strategies invest across credit quality levels, maturities, collateral types and levels of a company’s capital structure, which refers to the mix of debt and equity a business uses to finance operations and growth.

Haworth says some managers pursue complex credit strategies that have added value to portfolios. “What’s attractive is that they not only buy credits but have the flexibility to ‘short’ against them as well,” he says. That flexibility can help managers express both positive and negative views within credit markets, but it also raises the need for careful manager evaluation.

Event driven funds take equity or fixed-income positions based on an event that’s expected to increase a security’s value. Events can include company mergers, a firm spinning out a subsidiary unit or a company’s capital restructure. Often referred to as “special situations,” these events are key in determining a stock or bond’s value.

Relative value funds seek to profit from pricing differences between related financial instruments. These strategies typically have less exposure to stock and bond markets than equity hedge and long/short credit strategies. Examples of relative value strategies include credit arbitrage where traders target mis-pricings between bonds and default swaps, and convertible bond arbitrage which simultaneously purchases a convertible bond and sells short the issuer company’s stock.

Global macro hedge funds have the broadest mandate among common hedge fund strategies. They can invest across asset classes, markets and investment types as managers assess the global economic landscape. These managers seek to profit from imbalances or dislocations tied to macroeconomic and geopolitical events.

Haworth says global macro strategies can benefit from higher volatility. “We’ve been in a period of greater potential volatility, which can create better opportunity for funds like these to add value,” he notes. Because global macro managers have significant flexibility, investors should evaluate how each fund defines its opportunity set and controls risk.

Managed futures hedge funds focus on trading futures and forward contracts across different assets. Their objective is to generate returns that do not closely track stock and bond markets. These strategies often rely on computer-driven algorithms that seek to identify asset price trends, and managed futures rank among the more liquid hedge fund offerings.

Hedge funds can offer meaningful potential benefits, but they also introduce meaningful risk. “It’s important to work with a professional to consider whether specific hedge fund managers can add enough value to your portfolio for the risk you take on,” says Haworth. That evaluation should consider the manager, strategy, fees, liquidity terms, tax reporting and how the hedge fund may support the investor’s broader objectives.

Investors should discuss hedge funds with a financial professional before deciding whether to invest. The conversation should cover how hedge funds work, expected returns, potential risks, fees and tax considerations. A financial professional can help determine whether hedge funds could enhance a portfolio, support diversification and align with the investor’s long-term investment objectives.

Learn how we approach your long-term investing success.

Based on our strategic approach to creating diversified portfolios, guidelines are in place concerning the construction of portfolios and how investments should be allocated to specific asset classes based on client goals, objectives and tolerance for risk. Not all recommended asset classes will be suitable for every portfolio. Diversification and asset allocation do not guarantee returns or protect against losses.

Indexes shown are unmanaged and are not available for direct investment. The S&P 500 Index consists of 500 widely traded stocks that are considered to represent the performance of the U.S. stock market in general. The HFRI Fund Weighted Composite Index is a global, equal-weighted index of over 1,400 single-manager funds that report to HFR Database. Constituent funds report monthly net of all fees performance in U.S. dollar and have a minimum of $50 million under management or a 12-month track record of active performance. The HFRI Fund of Funds Composite Index consists of over 800 constituent hedge funds, including both domestic and offshore funds. Fund of Funds invest with multiple managers through funds or managed accounts. The strategy designs a diversified portfolio of managers with the objective of significantly lowering the risk of investing with an individual manager. The Fund of Funds manager has discretion in choosing which strategies to invest in for the portfolio. The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

Accredited investor: For individuals, the requirement is generally met by a net worth that exceeds $1 million (excluding primary residence and any related indebtedness), income in excess of $200,000 (individually)/$300,00 (jointly with spouse) in the two most recent years with an expectation of the same in the current year, or individual has a Series 7, 65 and/or 82 securities license(s). (Relying on joint net worth or income does not mean securities must be jointly purchased.) For entities (including trusts, non-profit corporations exempt under s. 501(c)(3), LLCs, LLPs, corporations, etc.), the requirement is generally met with if the entity has assets in excess of $5 million (assuming the entity was not formed for the specific purpose of acquiring the securities offered), or when all of the entity owners are accredited investors. Please refer to Rule 501 under the Securities Act of 1933 for the complete definition. Qualified Client: The requirement is generally met if the investor has at least $1.4M under investment with the fund manager, the investor has a net worth of more than $2.7 million (excluding primary residence and any related indebtedness), or the investor is a Qualified Purchaser (see below). Please refer to Rule 205-3 under the Investment Advisers Act of 1940 for the complete definition. Qualified Purchaser: For individuals, the requirement is generally met when the investor owns (individually or jointly) $5 million or more in investments. [Relying on joint ownership of investments does not mean securities must be jointly purchased.] For entities (including trusts), the requirement is generally met if the entity owns $25 million or more in investments; the entity owns $5M or more in investments AND it is owned by two or more natural persons who are related as siblings/spouse; or all beneficial owners of the entity are each Qualified Purchasers. Please refer to Section 2(a)(51) of the Investment Company Act of 1940 for the complete definition.

It’s easy to get caught up in the excitement surrounding IPOs. Review these common misconceptions before investing.

IPOs can be exciting new choices for investors, but not all of them perform equally. Review these common misconceptions before investing in initial public offerings.