Start investing today with U.S. Bancorp Advisors.

Investment products and services are: Not a deposit | Not FDIC insured | May lose value

Saving and investing are both important financial strategies, but they serve different purposes. The main difference is that saving is for short-term goals and emergencies, while investing is aimed at growing your wealth over the long-term.

Savings accounts offer lower risk with more stable returns, while investing involves higher risks but the potential for greater returns over time.

Understanding the differences between saving and investing can help you make informed decisions about how to allocate your money to meet both immediate needs and future financial goals.

There are some key differences between saving and investing. Both strategies help you set aside money for future use, but they don’t carry the same level of risk. How you determine when to save and when to invest will depend on your budget and financial goals.

Fortunately, you can do both at the same time, based on your goals and timeline.

Saving usually makes sense if you need the money within five years. Investing is typically better suited for long-term goals.

Saving usually makes sense if you need the money within five years, such as planning for a vacation or buying a house. Investing is typically better suited for long-term goals, such as retirement or a college fund for your children or grandchildren.

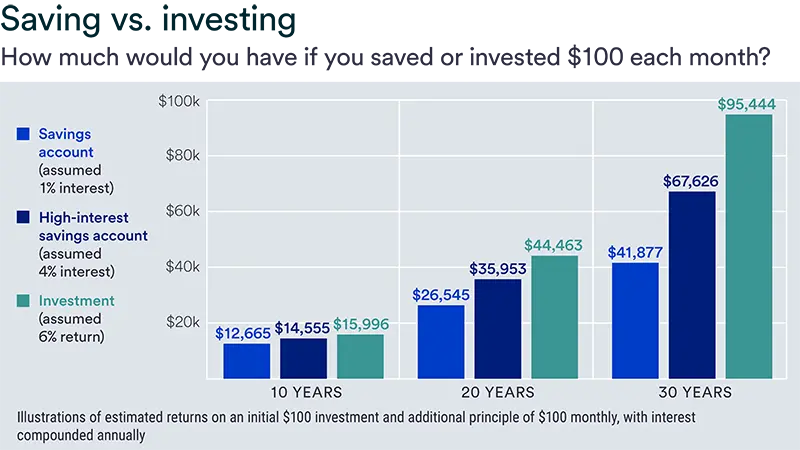

The money you put into a savings account is more liquid than the money you put into investments. When it comes to investing, patience is key. The longer your money stays invested, the more it can grow through compounding, which is when your earnings earn more earnings.

The primary benefits of investing include higher potential returns over time and the ability to manage the effects of inflation. Investing can help your money grow, especially for long-term goals. Here are a few reasons why:

Over longer periods, stocks have historically outpaced inflation more often than cash, but returns can vary significantly year to year and there are no guarantees.

A simple way to think about the timing is to save for what you’ll need soon and invest for what can wait. If you’re deciding between saving and investing, the right choice usually depends on when you’ll need the money and what the money is for.

You may want to focus on saving first if:

You may be ready to prioritize investing if:

Many people use both strategies at the same time. By setting aside savings for short‑term needs and investing for the long term, you can build flexibility today while working toward future growth.

Investing works by purchasing assets that have the potential to increase in value over time. Common investment options include:

While you can buy and sell these assets at any time, some types of investments may need more time to mature. Selling early may come with costs and fees. Market conditions also matter, as selling during a downturn can lock in losses.

It’s better to approach them as long-term investments to get the best potential for growth.

Many people begin investing through a retirement account. Common options include a 401(k) or an IRA.

Retirement accounts usually hold a mix of investments. These can include stocks, bonds, mutual funds and ETFs. You can choose your own mix or select a target date fund, which adjusts automatically as you get closer to retirement.

In general, people with more time before retirement may be comfortable taking on more risk. Those closer to retirement often shift toward lower‑risk investments.

The main benefits of saving include easy access to your cash and protection against market risk. While investing can help you achieve long-term financial goals, there should be a place for savings accounts in your financial plan, too.

Here are a few benefits of keeping some of your money in a savings account:

How savings accounts work is simple: you deposit funds into the account, and the bank pays you a yield based on an interest rate. Saving is a lower-risk way to set money aside, though returns are usually lower than investing. Common savings options include:

When you place money in a savings account, the bank pays you interest. In exchange, the bank uses those deposits to support its lending activities. Some accounts allow you to withdraw money at any time. Others, such as CDs, require you to leave funds in the account for a set period to avoid penalties.

In general, you may want to focus on building savings and pay down high-interest debt before diving into investing. This acts as protection against unexpected costs. A common rule of thumb is to have at least three to six months' worth of your household income set aside in an emergency fund.

Learn about savings accounts at U.S. Bank.

Remember, your financial plan should include both savings and investments. It’s important to understand the risks and rewards of savings and investing.

|

|

Risks |

Rewards |

|---|---|---|

|

Saving |

|

|

|

Investing |

|

|

Saving

Risks

Rewards

Investing

Risks

Rewards

The main difference is the time horizon and risk involved. Saving is designed for short-term goals and emergencies with minimal risk, while investing is meant to help you build long-term wealth and can fluctuate with markets.

Yes, it’s generally recommended to build an emergency fund first. Having three to six months of household income saved protects you from unexpected costs before you take on the risks of investing.

No, you typically don’t lose your principal in a standard savings account. As long as your bank is an FDIC member, your deposits are federally insured up to $250,000 against bank failure.

High savings rates can make saving more appealing for near-term needs. For long-term goals, investing may still be appropriate because the timeline is longer and markets can fluctuate. In many cases, focusing on when you’ll need the money can be more helpful than focusing on today’s rates alone.

Many beginners start by building a small emergency buffer and learning how retirement accounts work. From there, they may choose to save for short-term goals and invest for long-term goals, sometimes doing both at the same time.

A money market account is typically a bank deposit product and may be FDIC insured (within limits). A money market fund is an investment product and is not FDIC insured and may lose value.

A healthy financial plan isn’t about deciding between saving vs. investing. It often involves both. Savings can support near-term goals and emergencies, while investing can support long-term growth.

Whatever your financial situation and goals, start thinking about both options. You may also want to consider discussing your plans with a financial professional. They can help you put together a financial plan that sets you on a path toward your financial goals. They can also advise on how much flexibility you need today versus growth you want over time and adjust that balance as your life changes.

From investing online to working with a financial professional, we have investing options to meet your needs.

Investing can help you reach your financial goals, but it can be hard to know where to begin. This step-by-step guide can get you started.

Let us help you craft a portfolio that reflects your goals, time-horizon and values.