Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

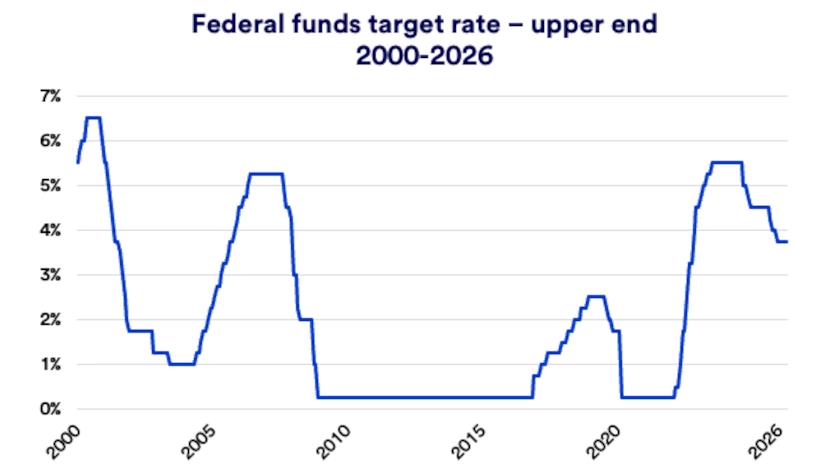

Federal Reserve (Fed) policy stayed steady at 3.50% to 3.75% as officials weighed inflation risk, slower hiring and Middle East uncertainty.

Energy prices could slow inflation’s return to the Fed’s 2% goal, even as shelter costs continue easing.

Markets expect the Fed to hold rates steady longer, making diversified portfolios and disciplined positioning especially important.

The Federal Reserve (Fed) influences borrowing costs, savings returns, and overall financial conditions across the economy. At its April 29 meeting, the Federal Open Market Committee (FOMC) left the federal funds target range at 3.50% to 3.75%, which markets broadly expected. The Fed also acknowledged that Middle East developments have increased uncertainty around the economic outlook and said officials are watching risks to both inflation and employment. 1

The decision kept the Fed in a wait-and-see posture as officials balance inflation risk against a softer labor market. Nearly all voting members supported holding rates steady, while one favored a 0.25% rate cut. Three other members disagreed with the statement’s easing bias rather than the rate decision itself, which showed a divide over how strongly the Fed should signal potential future cuts.

“The Federal Reserve held rates steady in April because inflation is still above target, job growth has slowed, and higher oil prices added a new layer of uncertainty,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group. Policymakers still need more evidence that inflation can keep moving lower before they gain confidence in a clearer rate-cut path.

Fed leadership is also entering a transition period. Jerome Powell held his final press conference as chairman, and Kevin Warsh is on track to replace him after the Senate banking committee advanced his nomination to the Senate floor on April 29. Chair Powell said during the press conference that he will remain on the Board of Governors for a period of time until the Justice Department’s investigation into him is “well and truly over.”

That timing affects the Fed’s leadership structure because President Trump cannot nominate a replacement for Chair Powell’s Board seat until Powell steps down. The investigation into Chair Powell centered on his Congressional testimony regarding cost overruns for the Fed’s ongoing headquarters renovations. Leadership changes do not automatically alter policy, but they can influence how the Fed communicates its outlook, manages its balance sheet and explains its rate decisions to investors.

Warsh has favored changes in Fed practices, including a smaller balance sheet and less forward guidance on interest rates and the economic outlook. Forward guidance refers to the Fed’s public signals about where rates and the economy may move next. Warsh has also expressed a preference for lower interest rates in the current environment, which could shape future policy discussions if inflation pressures ease and labor market conditions soften further.

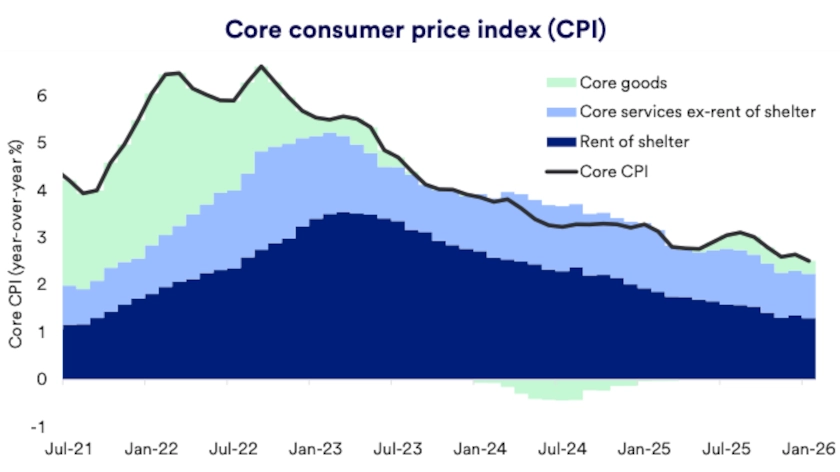

Inflation is much lower than it was in 2022, but the path back to the Fed’s 2% goal looks less certain today. The Fed’s preferred inflation measure, the core Personal Consumption Expenditures Price Index, rose 3.2% in the 12 months through March. Goods prices, which can respond quickly to higher energy and shipping costs, rose 3.8% from a year earlier. 2

The details explain why Fed officials remain cautious. Elevated energy costs tied to the closure of the Strait of Hormuz are pushing prices higher in areas that touch consumers and businesses. The Federal Reserve’s April Beige Book also pointed to broad cost pressure, with sharp increases in energy and fuel costs across all districts and additional input cost increases beyond energy-related categories. 3

That does not mean inflation is returning to 2022 levels. It does mean the final move toward the Fed’s 2% goal could take longer and may not move in a straight line. “Inflation may temporarily accelerate,” says Bill Merz, head of capital markets research for U.S. Bank Asset Management Group. “But factors beyond energy costs determine inflation over the medium-term.”

Some areas of inflation may still improve from here. The March Consumer Price Index (CPI) increased 3.3% over the prior year, while core CPI excluding food and energy rose 2.6%, and shelter costs increased 3.0% over the year. 4 Those readings support the view that housing costs may continue easing with a lag, even if higher energy prices create a near-term headwind.

That lag is important because rent trends usually move into official inflation data gradually. Slower rent growth can still offset some pressure from higher goods, fuel and transportation costs later this year. The inflation backdrop looks far better than it did in 2022, but it looks less predictable than it did earlier this year.

Middle East developments are a key reason the inflation path looks less clear. About 20% of global oil and liquefied natural gas move through the Strait of Hormuz, and fertilizer shipments also rely on that route. If shipping remains constrained, higher fuel, transportation and fertilizer costs can eventually reach household budgets, business expenses and food prices.

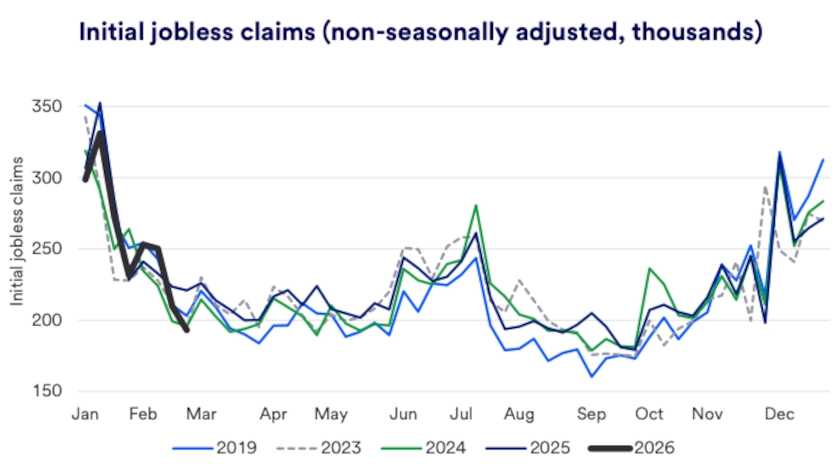

The labor market looks softer than it did a year ago, but it does not show signs of broad stress. Private employers added an average of 46,000 jobs per month through March this year. The unemployment rate stood at 4.3% in March, and weekly initial jobless claims fell slightly to 189,000 in the week ending April 24. 5

Slower hiring can cool the labor market without creating the widespread job losses that often hurt consumer spending quickly. That distinction gives the Fed room to keep rates steady while it watches whether slower hiring spreads into broader weakness. “The job market is softer,” says Merz, “but it still looks more like reduced hiring than widespread layoffs, and that difference matters for the Federal Reserve.”

The Fed’s April 29 statement described a labor market that continues to cool without showing signs of a sharp break. Officials noted that job gains have remained low on average while unemployment has changed little in recent months. 1 That combination points to a slower job market rather than a sudden downturn, which supports the Fed’s decision to remain patient.

The Fed’s March Summary of Economic Projections, released six weeks before the April meeting, already showed some effect from higher oil prices. Officials’ median inflation projections increased slightly, but economic growth expectations increased as well. 6 That mix reflected resilient consumer spending, steady corporate activity and a labor market with slower but still positive hiring.

“Markets lean toward the Fed maintaining current policy settings, but inflation, oil prices, and labor market conditions can shift the outlook.”

Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group

Earlier Fed tightening helped bring inflation down over the past four years. Aggressive rate increases from early 2022 to mid-2023 helped lower core PCE inflation from a peak above 5.5% year-over-year in 2022 to 3.0% in February 2026. The Fed later shifted course as inflation slowed, cutting its target interest rate by 1.75% through 2024 and 2025.

From late February to early April, oil prices rose more than 76%, pushing the Fed back into a more cautious stance. 7 Interest rate markets now imply a high likelihood that the Fed keeps its 3.50% to 3.75% policy range in place through the end of the year. 8 “Markets lean toward the Fed maintaining current policy settings, but inflation, oil prices, and labor market conditions can shift the outlook,” says Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group.

Interest rate decisions are only one part of Fed policy. The Fed began buying short-term Treasury bills in December 2025 to maintain ample reserves in the banking system and keep short-term rates close to its intended policy range. The Fed recently announced it would reduce regular purchases, and its bond holdings now stand near $6.7 trillion after peaking near $9 trillion in 2022. 9

These purchases affect liquidity, which means the money available to buy goods, services and financial assets. When the Fed buys Treasury bills, it absorbs part of the new supply and can support smoother market functioning. Stronger liquidity can also help markets absorb unexpected shocks, and current liquidity measures remain constructive.

Investors should watch liquidity alongside inflation, employment and rate expectations. A stable liquidity backdrop can support markets, but it does not remove risks tied to energy prices, geopolitics or policy uncertainty. It does, however, give investors another reason to focus on broad portfolio resilience rather than a single rate forecast.

For investors, this environment rewards discipline more than prediction. Higher energy prices could lift inflation and slow economic activity, but consumer spending and corporate earnings have remained resilient. As Tom Hainlin notes, “Investors do not need to predict every rate move to make progress. They need a portfolio built for more than one outcome.”

Diversification becomes more valuable when inflation, interest rates and geopolitics move at the same time. A mix of assets such as globally diversified stocks, global infrastructure and structured credit can help broaden return sources when traditional stock and bond holdings face the same macroeconomic pressure. A diversified plan can also help investors stay anchored when short-term headlines move faster than long-term fundamentals.

A nation’s central bank, which in the United States, is the Federal Reserve, typically controls monetary policy. The Fed’s management of monetary policy can have a significant impact on the shape of the nation’s economy. Congress’ mandate for the Fed is to maintain price stability (manage inflation); promote maximum sustainable employment (low unemployment); and provide for moderate, long-term interest rates. Fed monetary policy influences the cost of many forms of consumer debt such as mortgages, credit cards and automobile loans.

The Fed is the nation’s central bank, and perhaps the most influential financial institution in the world. The central governing board of the Federal Reserve reports to Congress, while the President appoints the chair of the Federal Reserve. There are also 12 regional federal reserve banks that are set up like private corporations.

The Federal Reserve’s Federal Open Market Committee sets a target interest rate policy for the federal funds rate. This is the rate at which commercial banks borrow and lend excess reserves to other banks on an overnight basis. The Fed raises or lowers the rate to impact underlying economic conditions. For example, in 2022, as inflation surged, the FOMC began raising interest rates to make borrowing more expensive and slow economic activity. The Fed designed that strategy to ease pricing pressures and reduce the inflation rate. In periods when the economy is slow or in a recession, the Fed tends to lower rates to try to stimulate economic activity and help the economy expand again.

Review your portfolio positioning with your financial professional and confirm that your investment mix still reflects current conditions and future expectations. The Fed may hold rates steady for longer if inflation remains elevated, but the outlook can change if energy prices, labor market data or financial conditions shift. A disciplined plan can help you respond thoughtfully rather than react emotionally.

The Federal Reserve kept its main policy rate unchanged at 3.50% to 3.75%. In its statement, the Fed said economic activity has been expanding at a solid pace, job gains have remained low, and inflation remains elevated. The FOMC also said developments in the Middle East are contributing to a high level of uncertainty for the U.S. economy. 1

Inflation is much lower than it was in 2022, but it is still above the Fed’s 2% goal. The March personal consumption expenditure report showed price pressures from energy costs, 2 and the Federal Reserve’s Beige Book noted widespread input cost pressures tied to elevated energy and fuel costs.3 That combination can slow further progress even when the longer-term trend still looks better than it did a few years ago.

The Fed’s median projection still points to one quarter-point cut in 2026, even after officials raised their inflation forecasts. 6 Interest rates price in the likelihood that the Fed holds its policy rate steady through 2026, though Kevin Warsh, the next Fed Chair nominee, previously supported reducing interest rates. In practical terms, that means lower rates are still possible this year, but the path depends more heavily now on what happens to inflation, energy prices, and the labor market.

The Federal Reserve held rates steady as expected at its March policy meeting, citing inflation uncertainty and energy prices, while officials’ projections continue to point to one rate cut in 2026.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.