Capitalize on today’s evolving market dynamics.

With markets in flux, now is a good time to meet with a wealth advisor.

September’s Consumer Price Index showed elevated inflation, accelerating somewhat since April but in line with early 2025 increases.

Investors haven’t expressed significant concern, as inflation remains lower than 2021-2023 levels.

Investors do wonder if higher tariffs will push inflation higher.

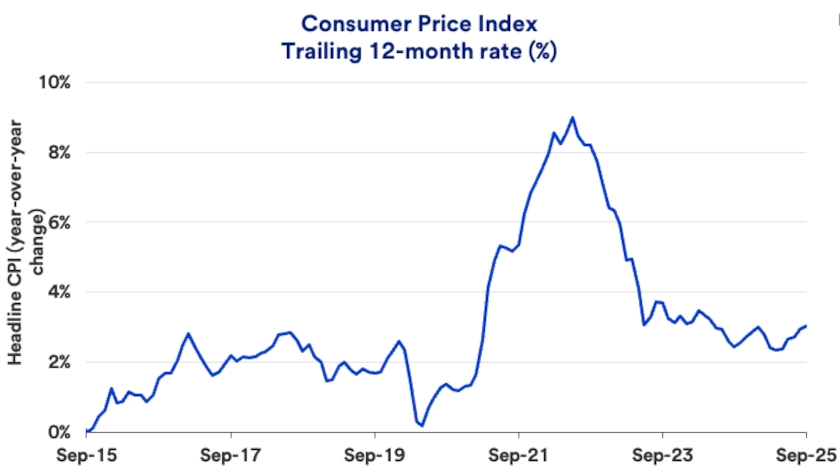

After a two-week delay due to the government shutdown, the Bureau of Labor Statistics reopened long enough to release the September Consumer Price Index (CPI). This month’s measure is a key input to the Social Security Administration cost-of-living adjustment. The index increased by 3.0% over the past 12 months, above August’s rate of change of 2.9% and in line with January’s 2025 3.0% increase. 1 This inflation level remains well above the average in the pre-pandemic decade and elevated relative to the Federal Reserve’s (Fed) 2% target.

Investors and economists worried this year’s higher imported goods tariffs might boost prices and lead to rising inflation. However, while certain goods prices increased relative to pre-tariff levels, the impact has not been as large or as widespread as investors initially feared. “Investors today watch inflation closely because of the uncertainty related to tariff impacts,” says Bill Merz, head of capital markets research for U.S. Bank Asset Management Group. Prices for often-imported goods like household furnishings, household supplies and apparel have accelerated so far this year.

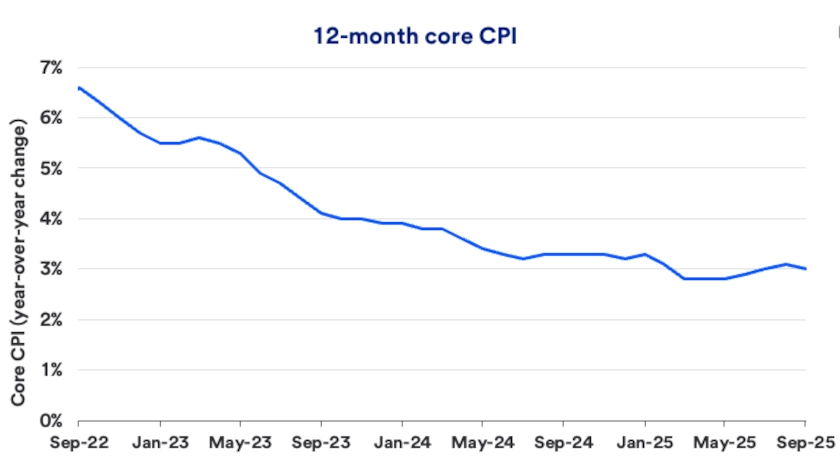

Volatile food and energy prices greatly impact inflation as measured by the broad, commonly cited headline CPI number. However, market professionals often focus on core inflation measures, which exclude volatile food and energy costs. In September, the 12-month core CPI fell slightly versus August at 3.0%. 1 Shelter costs increased by 3.6% year-over-year, comprising more than one-third of the CPI goods and services basket, significantly contributing to sticky inflation. 1 All items less food, energy and shelter decelerated to 2.6% year-over-year from 2.4% in January. 2

A second key consumer inflation measure, the Personal Consumption Expenditures (PCE) price Index, rose to 2.76% year-over-year in August, in line with the prior month. Core PCE, which excludes food and energy, increased remained stable at 2.9% year-over-year through August. 3 Both indices, CPI and PCE, measure the prices consumers pay for goods and services. The Federal Reserve targets PCE inflation in assessing the Fed’s 2% inflation target. However, the Bureau of Economic Analysis is closed due to the federal government shutdown. We do not expect any updates until the government reopens.

Inflation peaked at over 9% annually in June 2022, as measured by CPI, and has since trended lower with some fluctuations since September 2024. 2 However, President Trump's tariff plans raise inflation concerns. In September, the Federal Reserve's Federal Open Market Committee median projection for core PCE inflation was 3.1% at year’s end. 4

Investors are assessing what tariff rate or tariff policy duration will ultimately lead to higher prices. In other words, what’s the threshold when businesses can no longer avoid passing on higher tariff costs to consumers?”

Tom Hainlin, national investment strategist for U.S. Bank Asset Management Group

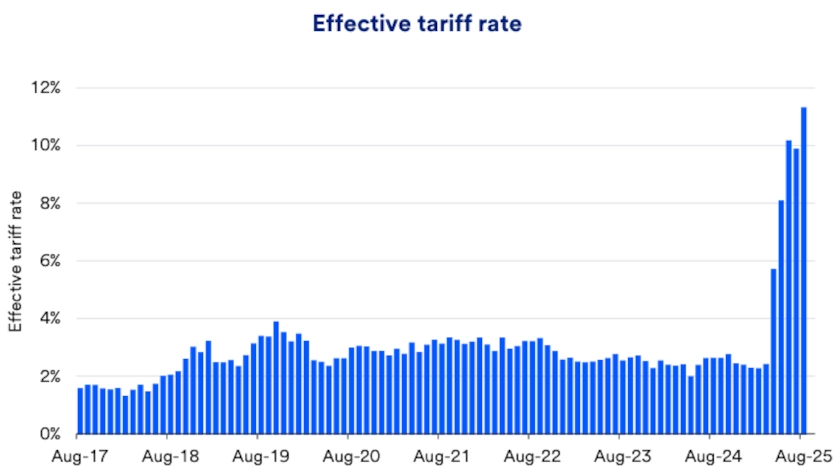

To start 2025, U.S. tariff revenue equaled an effective tariff rate of 2.5%, calculated as tariff revenue divided by imported goods values. By August, it neared 11%, while recently negotiated tariff rates range from 10% to 20%, though some reached higher levels. 5 If negotiations fail to lower current announced tariffs, the Yale Budget Lab estimates that the effective rate could reach 17% after substitution effects. 6 “Investors are assessing what tariff rate or tariff policy duration will ultimately lead to higher prices,” says Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group. “In other words, what’s the threshold when businesses can no longer avoid passing on higher tariff costs to consumers?”

How will higher tariffs impact inflation during 2025’s concluding months? “Our proprietary model suggests higher core goods prices may continue creeping into inflation data, but the impact on overall inflation should be modest,” says Merz. According to the Fed, all 12 regional districts within its jurisdiction report inflationary pressures related to tariffs. 7

Producer prices, which reflect business costs, indicate a mixed picture, though reporting after August data is delayed due to the government shutdown. The Producer Price Index rose 2.6% in August on a year-over-year basis, compared to 3.3% in July, while prices excluding food and energy rose 2.8% versus July’s 3.7% increase. 8 Moderating producer prices conflict with multiple business surveys indicating higher input costs, further complicating the inflation picture.

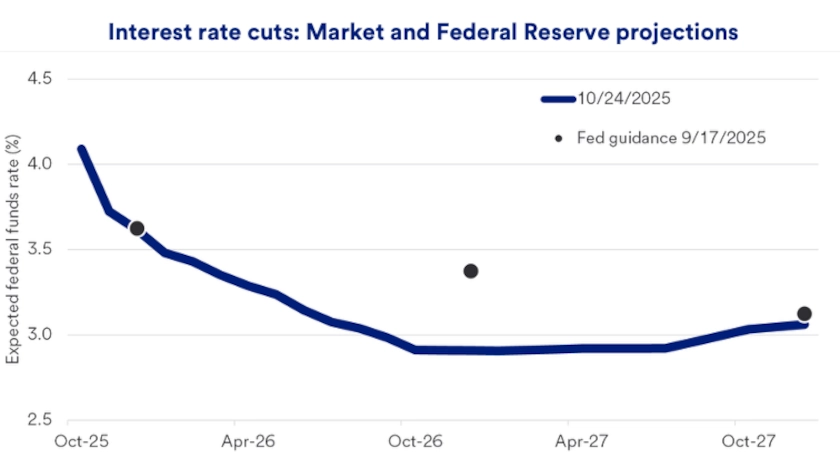

In 2022 and 2023 the Fed rapidly raised interest rates to combat inflation, then cut rates by one percent in late 2024. This year, despite lingering inflation, the Fed cut rates in September amid softer labor market conditions.

Fed Chair Jerome Powell and many Fed members have indicated openness to additional cuts this year. The Fed currently projects two additional rate cuts this year, in line with investor expectations.

Markets could be sensitive to sustained, accelerating inflation,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group. However, Haworth warns that inflation is not the only key measure that could trigger market volatility. “Further labor market weakness may suggest higher economic slowdown odds, which would represent a material market development,” notes Haworth.

“Ultimately, it comes down to what the consumer is doing, and despite weaker labor market data, consumer spending remains strong.” says Merz.

Rapidly evolving changes characterize the current environment, including the possible inflationary effects from increased tariffs. Investors benefit from keeping a broadly diversified portfolio, which could include such inflation sensitive assets as Treasury Inflation Protected Securities or Global Infrastructure.

“We continue to emphasize multiple return and income sources within client portfolios, and having a global perspective and the flexibility to embrace a variety of asset classes will likely benefit investors,” notes Hainlin.

It’s important to remember that a consistent long-term strategy tends to benefit most investors. This likely precludes any dramatic changes to your asset allocation strategy in response to today’s capital market environment.

Be sure to talk with your financial professional about what steps may be most appropriate for your situation.

The inflation rate measures the change in living costs for the average consumer over a given period. While there are various measures of inflation, the most popular is the Consumer Price Index (CPI), a measure of changes in the prices paid by urban consumers for a market basket of consumer goods and services. The CPI inflation rate for the 12 months ending September 2025 was 3.0%. 1

Higher living costs, reflected by inflation, represent a loss of purchasing power. This is an important consideration not only in your day-to-day living, but in your long-term financial planning. To improve your quality of life over time, you’ll want to see your income grow faster than the inflation rate. To retain your lifestyle in retirement, you want to be sure that income you receive from your own investments and other sources keeps pace with changes in living costs over the course of retirement. This is why inflation has such a significant impact on individuals.

The Federal Reserve, which Congress charged with maintaining stable prices, targets a long-term inflation rate of 2%. Between 2012 and 2020, the annual inflation rate was between 0.7% and 2.3%. Since that time, inflation has been much higher. It stood at 7.0% in 2021, 6.5% in 2022 and 3.4% in 2023 before dropping to 2.9% in 2024.6 Still, the Consumer Price Index, the most commonly cited inflation measure, remains above the Federal Reserve’s 2% target. 3

The S&P 500’s recent rollercoaster performance has investors wondering what lies ahead for the stock market.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.