Start investing today with U.S. Bancorp Advisors.

Investment products and services are: Not a deposit | Not FDIC insured | May lose value

Tax diversification means holding a mix of tax-advantaged accounts, tax-free accounts, and fully taxable accounts, each with distinct tax treatments that can work together to reduce your overall tax burden.

Spreading your savings across all three account types gives you more flexibility in retirement, letting you choose where to pull income from based on your tax situation in any given year.

Pairing tax diversification with tax-efficient investing (placing the right assets in the right accounts) can help you minimize taxes over your lifetime and keep more of what you've saved.

When you think of diversification, the first thing that comes to mind might be a mix of stocks, bonds and cash to lower your investment risk. But when you’re saving for retirement, tax diversification is just as important.

Tax diversification is when you have a variety of investment accounts with different tax treatments: fully taxable, tax-advantaged and tax-free. Using all three types of investment accounts can help you manage your taxable income over time and create more flexibility during retirement.

To put this strategy to work, you first need to understand how each account type functions.

Let’s look at the three main types of investment accounts.

Retirement accounts such as 401(k)s, 403(b)s and traditional IRAs are considered tax-advantaged (also called tax-deferred).

If you don’t have access to an employer-sponsored plan like a 401(k) or 403(b), a traditional IRA offers similar tax benefits but has lower contribution limits. Read more about the difference between IRAs and 401(k)s.

Traditional IRAs, 401(k)s and 403(b)s can help lower your taxable income today. However, they offer less flexibility in retirement due to RMDs, which could push you into a higher tax bracket. That’s where tax-free accounts can play a valuable role.

This category includes Roth IRAs and Roth 401(k)s, as well as 529 college savings plans and health savings accounts (HSAs).

The benefits of Roth accounts generally kick in when you retire. Since qualified withdrawals are tax-free, you could pay less tax overall during your retirement years.

A traditional brokerage account (generally comprised of stocks, bonds and mutual funds) is fully taxable. Other accounts, such as bank savings accounts and certificates of deposit (CDs), are also fully taxable.

Here’s what to expect from fully taxable accounts:

While fully taxable investment accounts offer few immediate tax benefits, they’re the most flexible in terms of use and withdrawals. They’re a good option if you’ve maxed out contributions to your retirement accounts and want to continue investing.

If you’re like most people, your default investment account is your tax-advantaged employer-sponsored plan. It’s easy to use, there’s often an employer match and contributing to it can lower your taxes during your working years. So how can you build more tax-free income before retirement, especially if most of your savings are in tax-advantaged accounts? One option is a Roth conversion.

Implementing a tax diversification strategy can create opportunities to shift future income into different tax categories. One example of this is a Roth conversion, in which you move money from a tax‑deferred account (like a traditional IRA or pre-tax 401(k)) into a Roth (tax‑free) account.

This type of money move is best evaluated in the context of your broader financial plan, since it involves tradeoffs between paying taxes now or in the future. Learning how different account types work together can help inform long‑term planning decisions.

Tax diversification is a strategy in which you determine where money lives (tax-deferred, tax-free, or fully taxable investment accounts). Tax-efficient investing, also called asset location, is a strategy in which you determine what investments live in each account.

Interest, dividends and capital gains are taxed differently on different asset types (stocks, bonds, ETFs, mutual funds, etc.), so placing the same mix into the wrong accounts can cost you money each year.

Investment Account

Best-Fit Asset Examples

Rationale

Tax-advantaged

High-yield bonds, high-dividend stocks, REITs (Real Estate Investment Trusts)

High-tax assets benefit from deferred taxation

Tax-free

High-growth stocks

Maximizes tax-free compounding

Taxable (brokerage)

Index funds, in-state municipal bonds

Tax-efficient assets by nature

Tax diversification and tax-efficient investing are complementary strategies. Using these strategies together can help you further minimize your tax liability. That combination pays off most clearly when you’re drawing down your portfolio in retirement.

The biggest perk of a tax-diversified investment portfolio is that it gives you more flexibility in retirement.

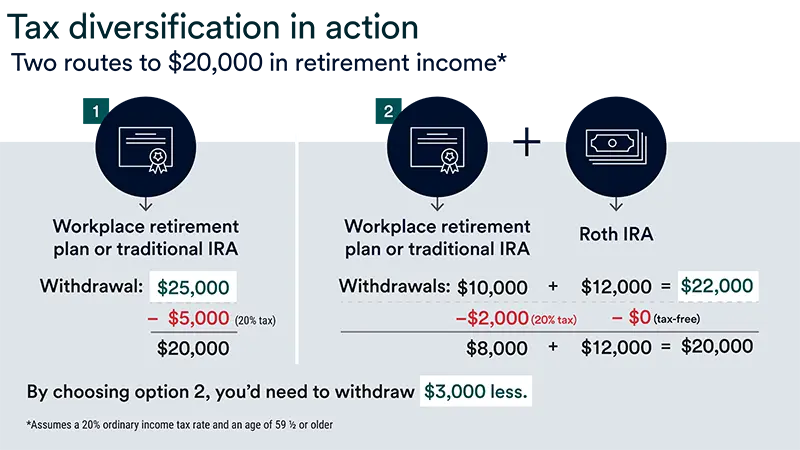

For example, imagine you need $20,000 in income. If you take it all from a 401(k), you pay income tax on every dollar. If your tax rate is 20%, you’d need to withdraw $25,000 to meet your income need.

If you also have a Roth IRA, you have more options. You could take $10,000 from your 401(k) (leaving you $8,000 after tax) and $12,000 tax-free from the Roth IRA. You still get $20,000 but you only withdraw $22,000 total. That saves you $3,000.

Tax diversification also helps you adapt to changing tax rates. In years when taxes are higher, for example, you can withdraw more from your tax-free Roth account. In years when your tax rate is lower, you can withdraw more from your taxable accounts.

When it comes to lowering your taxes over a lifetime, awareness is key. Choosing the right account for your life stage helps you keep more of what you save. Talk with a financial professional and tax advisor to build tax diversification into your financial plan.

Learn how our approach to wealth planning can help you see a full view of your financial picture.