Is your financial strategy keeping pace with your life?

Connect with an advisor for clear answers and strategies that align with your ambitions.

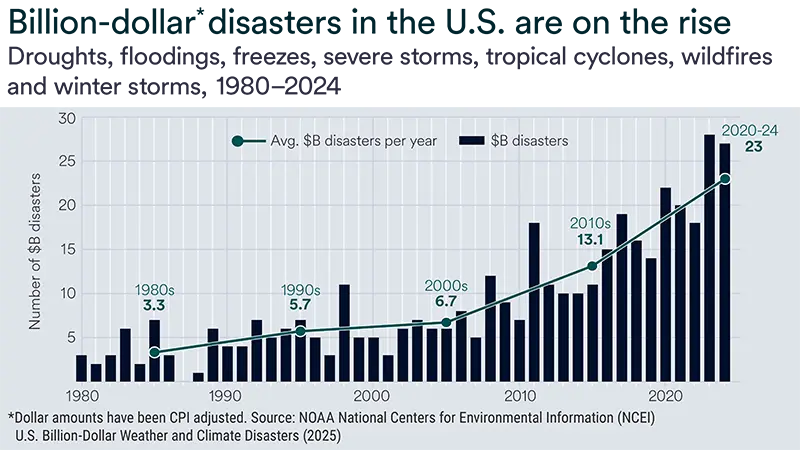

The number of weather/climate disaster events is climbing each year, impacting the finances of individuals, families and businesses.

A few financial “must haves” to financially prepare for these types of events include insurance with appropriate coverage, properly stored financial and planning documents, and some cash on hand.

Walking through “what if?” scenarios with a financial professional can help you stress test your financial plan and determine what steps you can take to be better prepared for the unexpected.

There were 27 weather/climate disaster events with losses exceeding $1 billion each in the U.S. in 2024, according to the NOAA National Centers for Environmental Information (NCEI). Compare this with 2022, when the U.S. experienced 18 such events.

These events spanned droughts, flooding, severe storms, tropical cyclones, wildfires and winter storms. “[Another] active year during which we had a high frequency, a high cost and large diversity of extreme events that affect people's lives and livelihoods [is] concerning because it hints that the extremely high activity of recent years is becoming the new normal,” NCEI states.

This “new normal” environment requires a new approach to protecting your assets and possessions.

While you can’t always be fully prepared for every natural disaster that affects your region, there are some steps you can take to protect your finances in the case of fire, hurricane, earthquake or other potentially catastrophic event. This is important, because any extreme event will not only be disruptive to your life but also to your finances.

“Natural disasters can have a significant impact on your overall financial plan, so it’s something we discuss often with our clients,” says Min Yoo, Senior Wealth Strategist with U.S. Bank Private Wealth Management. Unfortunately, this is also an area that many people overlook when establishing and administering their financial and disaster recovery plans.

One of the best ways to protect your assets in the event of an emergency is by having the right amount and type of insurance in place before a natural disaster happens. Be sure you understand what is and isn’t covered, what your deductible is and what will be allocated to structure (such as your home) versus contents in the event of an emergency.

Tom Nicoski, senior vice president and head of insurance at U.S. Bancorp Advisors, advises working with a property casualty agent to nail down the right amount of coverage for your specific property and/or possessions. If your home is worth $1 million, for example, the assumption will probably be that you have $300,000 of “insurable content” in that home. If the actual value of your assets exceeds that number, be sure to include it on your policy – even though it may increase your premium.

“Natural disasters can have a significant impact on your overall financial plan, so it’s something we discuss often with our clients.”

Min Yoo, Senior Wealth Strategist, U.S. Bank Private Wealth Management

When selecting policies, be sure to look beyond the premium price and read the fine print. Nicoski says the company’s experience, ratings and recent shifts (such as property insurers moving out of states like Florida and California) should all play into your decision.

“Ask your agent to identify the best options or conduct your own due diligence,” says Nicoski. “There are definitely situations where the ‘you get what you pay for’ mantra applies.”

Also be sure to keep a record of your belongings, any purchase receipts (as required) and photos of those items. Include all important records and documents in this exercise, with a particular emphasis on any estate planning documents, wills, passports, deeds, and birth and marriage certificates. If you own a business, be sure to include any important contracts, business entity records, articles of incorporation and other documents for safekeeping.

You’ll want to keep those records updated and stored either in a mounted fireproof safe or as a “virtual record” in the cloud. With the latter, you’ll still be able to log in and access those records from a different device in the case of a major property loss.

“With all of the technology advancements at your avail, you should consider using Google Drive, Dropbox or another cloud platform,” says Yoo. “That gives you an easy way to scan and upload documents and keep them safe and easily accessible.”

In the immediate aftermath of a hurricane, earthquake, wildfire or other natural disaster, getting access to life’s essentials may be difficult for some time. For this reason, it’s always good to keep a certain amount of cash on hand and to also keep at least some of your other assets liquid and accessible.

“Ideally, you’ll want to keep about six months’ worth of expenses in some form of liquid investment, such as a money market or other type of account,” Nicoski recommends. You should also keep about $300 to $500 in cash for instant access, knowing that apps like Zelle can also provide fast access to funds if needed in the aftermath of a natural disaster.

When working with clients, Yoo’s focus has historically been on helping those individuals and families plan for retirement. Today, more of those discussions include how to plan for unexpected events that could potentially derail those well-thought-out plans.

Individuals and families can borrow a page from the business world, which has been creating disaster plans and assessing “what if?” scenarios for decades.

For example, you can look at what perils typically affect your region (such as hurricanes, floods, blizzards, wildfires, earthquakes or tornadoes), and then stress test your individual financial situation to see what would happen if a natural disaster occurred. A financial professional can walk you through these scenarios and determine which proactive steps make the most sense.

“We start with a baseline assessment and then add different scenarios to model out the level of potential disruption to your life and finances in the event of a natural disaster or other catastrophic event.”

Both Yoo and Nicoski say it’s never too early to start financial planning for a potential disaster, knowing that many of these events pop up at the most unexpected times. Using an insurance strategy, recording your belongings, storing those records in a safe place and incorporating “what if?” scenarios into your financial plan, you’ll be better prepared to recover and rebuild quickly when the unexpected happens.

Over your lifetime, both exciting and challenging life events can have an impact on your financial wellbeing. A financial professional can help you manage your finances and assess your insurance needs to prepare for important moments.

Just like your financial goals, insurance policies are as unique as you are.

We can help you identify and prioritize your financial goals and design a plan to work toward them, making adjustments as your needs evolve.