Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

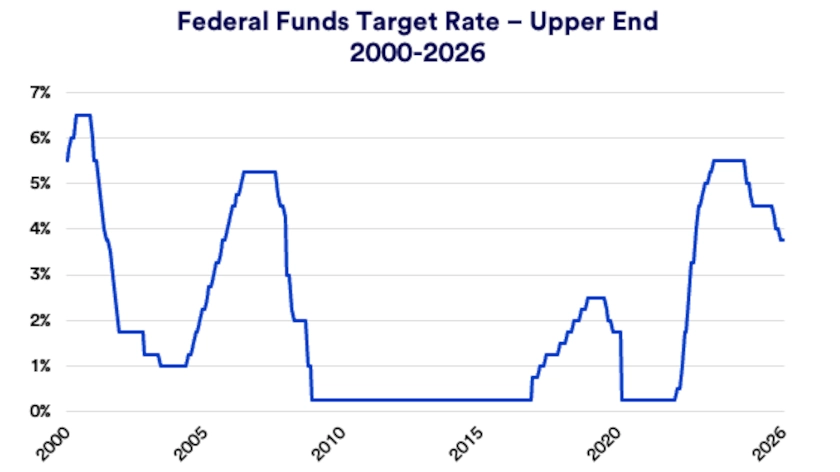

The U.S. Federal Reserve (Fed) held rates at a range of 3.50-3.75% and remain data dependent as markets still price two 2026 rate cuts.

Inflation remains elevated but hasn’t surged; tariffs could lift goods prices while shelter disinflation may continue.

Labor market shows cooling but stabilizing conditions; investors can use diversified fixed income beyond Treasuries to seek income and portfolio resilience.

The Federal Reserve’s (Fed) policymaking Federal Open Market Committee kept the federal funds target range at 3.50-3.75% at its January 2026 meeting, aligning with investor expectations. Policymakers largely supported the decision, though two members dissented in favor of a 0.25% rate cut, underscoring that the debate is when, not whether, to ease further. The Fed chose patience as it balances above-target inflation with a labor market that looks softer but steadier than earlier in the economic cycle.

Fed Chair Jerome Powell framed the moment as one of improving balance, noting that “the risks to both [inflation and labor markets] are a little less [than they were].” 1 Markets still reflect a high likelihood of two 0.25% rate cuts later in 2026, shaped by investor expectations and capital flows across the rate complex. 2 With Powell’s term expiring in May 2026, he emphasized that the Fed will follow the data and keep the forward path conditional on how the economy evolves.

The Fed left policy unchanged to evaluate the cumulative impact of rate reductions delivered in 2024 and across its final three meetings in 2025, while inflation remains elevated and job growth cools. Powell pointed to signs of labor market stabilization and argued the economic activity outlook has “clearly improved since the last meeting.” 1 That combination – steady policy now, openness later – keeps markets focused on each new inflation and employment print as a potential catalyst for the next move.

A weakening labor market over the last half of 2025 set the stage for the Fed’s 2025 easing, even though inflation has stayed above its target. Earlier in 2025, the Fed held rates steady while it weighed persistent inflation and uncertainty tied to tariffs, reinforcing their policy depends on both the level and direction of inflation and employment trends. Because the federal funds target anchors overnight lending rates between financial institutions, it influences most borrowing costs and helps shape interest rate conditions across the economy.

Inflation remains elevated, but it has not accelerated as much as feared following President Donald Trump's new tariff policies. Business “prices paid” surveys point to easing inflation expectations, and shelter costs – an important consumer inflation component - should continue falling. At the same time, rising tariff revenue could push goods inflation higher in coming months, which helps explain why the Fed continues to stress a data-driven approach. Addressing tariffs, Powell expects their effects will peak and continue to fade, supporting easier policy.

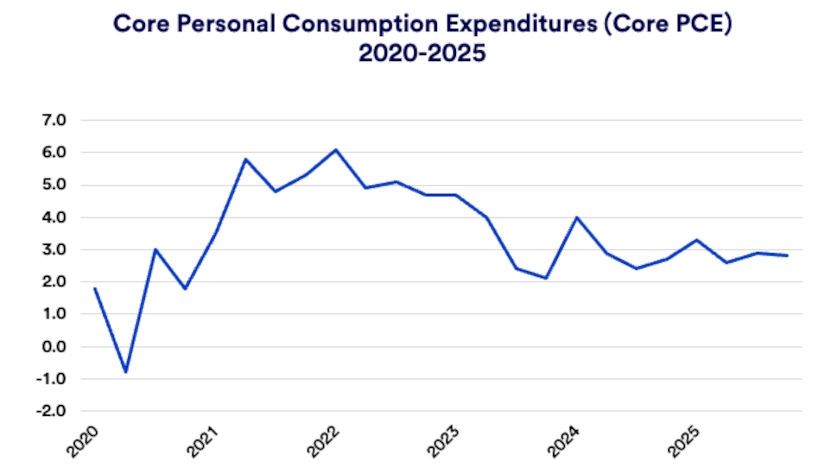

The inflation fight has already benefited from fed funds rate hikes in 2022-2023, which did much of the “heavy lifting”. Core Personal Consumption Expenditure inflation (the Fed’s preferred inflation measure) fell from a peak above 5.5% year-over-year in 2022 to 2.8% by June 2024, and the Fed has since shifted from restrictive policy to easing. 3 Specifically, the Fed cut rates 1% in 2024’s second half and 0.75% across the last three meetings in 2025, while still monitoring inflation’s next phase under the new tariff backdrop.

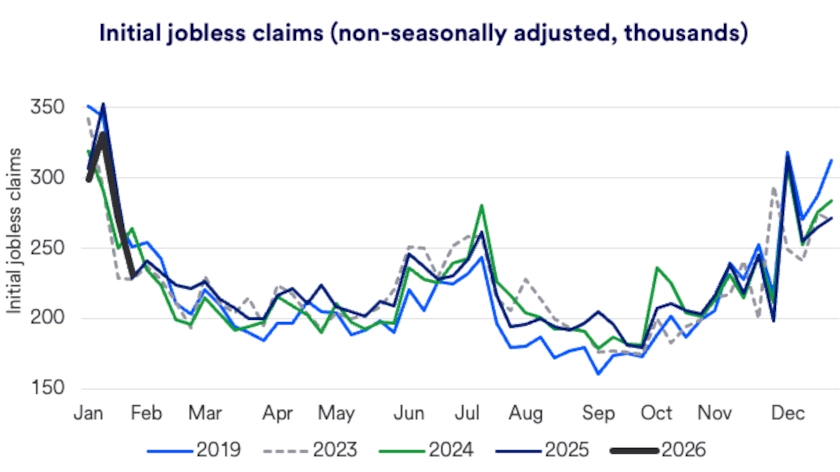

On the labor market side of its mandate, the Fed is watching for signs that slowing hiring becomes something more persistent. December non-farm payrolls rose by 50,000 net new jobs, 4 recovering from earlier weak reports, while Automatic Data Processing estimated 41,000 private sector job gains. 5 The unemployment rate stands at 4.4%, which remains low by historical standards even as it drifts higher. 4

“Negative labor market revisions and recent data indicate a softer hiring picture, but one which appears to have stabilized.”

Bill Merz, head of capital markets research at U.S. Bank Asset Management Group

Other signals paint a similar “cooling, not cracking” picture. Weekly initial jobless claims reports remain low and consistent with prior seasonal patterns, yet continuing claims have climbed above those of recent years, suggesting job seekers are taking longer to find work. 6 Bill Merz, head of capital markets research with U.S. Bank Asset Management Group, emphasizes that the labor market is a key policy input: “Negative labor market revisions and recent data indicate a softer hiring picture, but one which appears to have stabilized,” says Merz. Higher income consumers continue to drive solid aggregate consumer spending.”

Rate decisions matter, but so does liquidity – the amount of money readily available to fund spending and investment. The Fed previously expanded its balance sheet by purchasing bonds during and after the Covid pandemic to lower long-term borrowing costs, and that legacy still influences market functioning today. In December, the Fed stopped shrinking its $6.2 trillion bond holdings (after peaking at $8.5 trillion in 2022) and began buying short-term Treasury bills to keep bank reserves ample and short-term interest rates near policy targets.

By supporting financial system reserves and aiming to cushion money markets against shocks, this approach can reinforce smoother market plumbing even while their policy remains restrictive relative to the prior decade. In practical terms, investors often experience this through steadier short-term funding conditions and a monetary policy stance that can pivot as the data changes. That combination – policy patience plus liquidity support – helps explain why markets can price future easing even while the Fed holds steady in the present.

Markets have responded constructively so far in 2026, with the S&P 500 up over 1.9% year-to-date after gaining 17.9% in 2025, despite a volatile April tied to tariff announcements. 7 Bonds also delivered positive performance in 2025, with most traditional bond categories returning 6-to-8%, while 10-year U.S. Treasury yields generally stayed between 4.00-4.3% in recent months. 8

For investors, this environment can reward discipline more than prediction. We continue encouraging investors to explore ways to diversify fixed income holdings beyond U.S. Treasury securities. Opportunities exist in high-yield municipal bonds for highly taxed investors, structured credit such as collateralized loan obligations (CLOs), non-government agency backed mortgages, and catastrophe bonds or reinsurance for qualified investors. Consult your financial professional and review portfolio positioning to ensure your investments align with current market conditions and future expectations.

A nation’s central bank, which in the United States, is the Federal Reserve (Fed), typically controls monetary policy. The Fed’s management of monetary policy can have a significant impact on the shape of the nation’s economy. Congress’ mandate for the Fed is to maintain price stability (manage inflation); promote maximum sustainable employment (low unemployment); and provide for moderate, long-term interest rates. Fed monetary policy influences the cost of many forms of consumer debt such as mortgages, credit cards and automobile loans.

The Fed is the nation’s central bank, and perhaps the most influential financial institution in the world. The central governing board of the Federal Reserve reports to Congress, while the President appoints the chair of the Federal Reserve. There are also 12 regional federal reserve banks that are set up like private corporations.

The Federal Reserve’s Federal Open Market Committee (FOMC) sets a target interest rate policy for the federal funds rate. This is the rate at which commercial banks borrow and lend excess reserves to other banks on an overnight basis. The Fed raises lowers the rate to impact underlying economic conditions. For example, in 2022, as inflation surged, the FOMC began raising interest rates to make borrowing more expensive and slow economic activity. The Fed designed that strategy to ease pricing pressures and reduce the inflation rate. In periods when the economy is slow or in a recession, the Fed tends to lower rates to try to stimulate economic activity and help the economy expand again.

The Federal Reserve kept rates at 3.50%–3.75%, noting improving inflation and labor trends as investors continue to price in two cuts for 2026.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.