These types of investing misconceptions can get in the way of building a solid financial future. Get the facts around common investing myths.

Hispanics and retirement planning

Many older Hispanics/Latinos also haven’t engaged with the concept of saving for retirement, Isordia says, as it was always expected that their adult children would take care of them. This means that many older people didn’t seek out jobs with 401(k) plans, and they may not have had financial education on topics such as types of retirement plans, like IRAs (individual retirement accounts).

As part of this, younger generations have often taken on debt to assist aging parents or left their careers altogether.

“A lot of people in the community feel like they will have to leave their job to take care of their parents,” Isordia says. “They don't look at different options for parents, such as getting help from caretakers. This was especially true for taking care of parents in the Silent Generation, but I’m beginning to see some differences as baby boomers start to retire.”

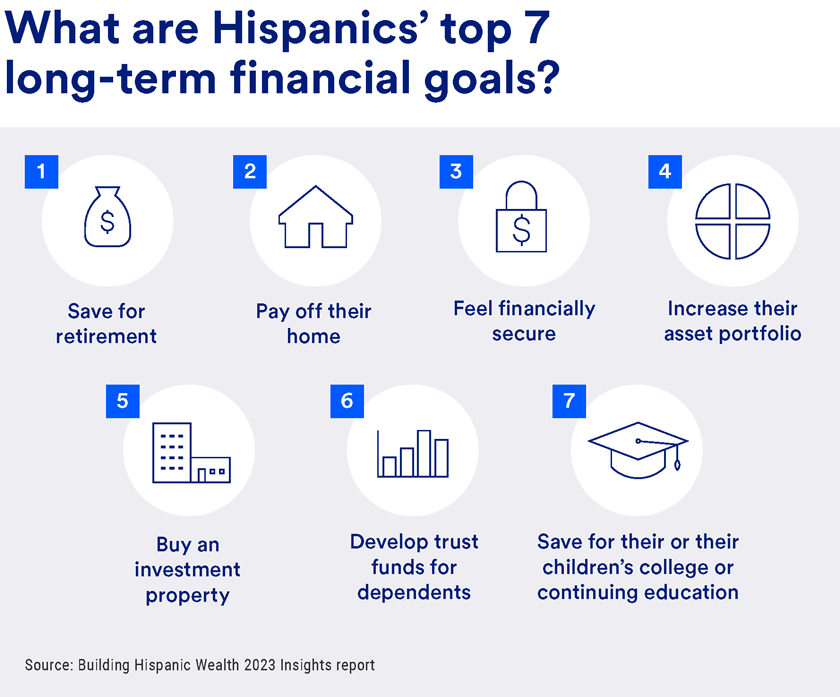

A shift in legacy planning for Hispanics/Latinos

Older generations also didn’t tend to leave financial legacies for the next generation, preferring the mentality of, “I worked hard to get ahead; now you have to work hard to get ahead.”

“Now, more Hispanics and Latinos are making sure their kids are going to be OK, though I don’t feel that’s happening as much as it should, and we’re starting to educate people on that,” Isordia says.

With all that background in mind, here are five tangible steps Hispanics/Latinos can take today to begin working toward financial wellbeing.

Financial literacy for Hispanics/Latinos: Five ways to build a bright financial future

- Begin investing, either by opening an IRA or by taking advantage of a workplace retirement plan. Either way, you’ll realize tax benefits and grow your money through compound growth.

“A lot of Hispanics and Latinos don’t open 401(k) plans to invest in because they don’t want to lose money,” Isordia says. “But I tell them that they’re losing money by not taking advantage of their employer’s matching contributions. I recommend that they at least start contributing the same percentage that their employer is matching, and then build from there.”

- Automate saving. Your responsibility is to you, your family and community, in that order. Think about paying yourself first by setting up automatic contributions to your retirement account.

“That’s a huge mindshift for Hispanics and Latinos, who have been raised to feel that taking care of themselves first is selfish,” Isordia says. “But you have to take care of yourself first to be able to effectively take care of others, including leaving a legacy for your kids.”

- Support and protect your family through financial planning activities like securing insurance, saving for children’s education and estate planning.

“Planning is definitely something we have to educate Hispanics and Latinos to do more of,” Isordia says. “For example, after they die, a lot of their homes end up in probate, because they never really planned for how to appropriately transfer ownership to their kids. I tell my older clients, ‘You’ve worked so hard – do you want to lose it now to the state? Look at some ways for your kids to keep the house, as well as ways to transfer other aspects of your wealth.’”

- Boost your financial education. “There's always more to learn for all of us – even us doing this as a profession,” Isordia says. She also encourages parents and guardians to talk about money with their kids from an early age so they enter adulthood prepared to manage their finances.

- Seek financial planning support. An experienced financial professional can help you build a customized financial plan, which you’ll review regularly to make sure you’re on track.

“We can help people be successful in their financial goals, whether it's saving for retirement, buying a house or paying for their kids’ college tuition,” Isordia says. “Right now, their money is just sitting there, but we can help them build their investments so they can better realize their goals.”

If you need a financial professional, you don’t have to look very far. Start working with a financial advisor or wealth specialist today and create a strategy customized to your financial goals.