Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Historically, stock market performance improves after midterm elections, but election results alone do not reliably explain market returns.

Economic growth, inflation, interest rates and corporate earnings typically influence markets more consistently than party control of Congress.

Investors should follow policy developments while keeping portfolio decisions aligned with their goals, time horizon and tolerance for risk.

Midterm elections can change control of Congress and influence which policy proposals advance or stall. On November 3, 2026, voters will decide all 435 House seats and 35 Senate seats. The results could reshape the balance of power during the final two years of President Donald Trump’s current term.

Republicans currently hold narrow majorities in both chambers. As of July 14, the House included 218 Republicans, 212 Democrats, one independent and four vacancies, while the Senate included 53 Republicans, 45 Democrats and two independents who caucus with Democrats. Republicans control the White House and Congress, but their Senate majority falls short of the 60 votes generally required to end debate on most legislation and the two-thirds majority in each chamber required to override a presidential veto.

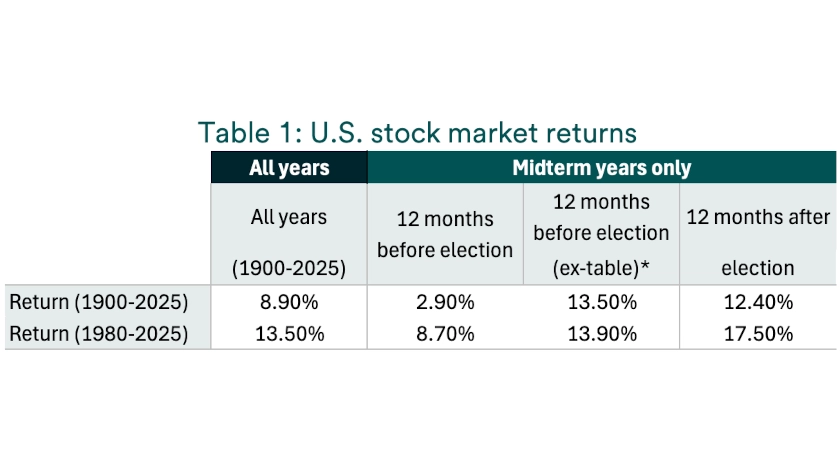

Investors often ask whether a change in congressional control will impact the stock market. To examine that relationship, U.S. Bank Asset Management Group Research reviewed Bloomberg market data covering 31 midterm elections from 1900 through 2025. The analysis compared U.S. stock returns before and after midterm elections while recognizing that markets respond to economic, business and geopolitical developments alongside public policy.

In the 12 months before midterm elections, U.S. stocks represented by the S&P 500 have historically produced an average return of 2.9%, below the 8.9% average for all years in the study. Campaign uncertainty and changing policy expectations may contribute to uneven trading as investors assess possible outcomes. However, the historical gap does not establish that midterm elections caused weaker returns.

Investors should not treat the pre-election pattern as a signal to move in and out of the market. Markets often adjust to policy expectations before voters cast their ballots, and policy expectations can shift repeatedly during campaign season. Economic growth, inflation, interest rates and corporate earnings can outweigh political developments.

Stock market performance after midterm elections has historically been stronger. In the following 12 months, U.S. stocks produced an average return of 12.4%. Once the election results become clear, investors can shift more attention toward the economic and corporate trends that support or restrain stock prices.

That stronger average does not mean stocks rose after every midterm election or that investors should expect the pattern to repeat in 2026. It also does not point to one portfolio decision that fits every investor. Instead, the data supports maintaining a strategy aligned with long-term goals and risk tolerance rather than making large changes in response to election headlines.

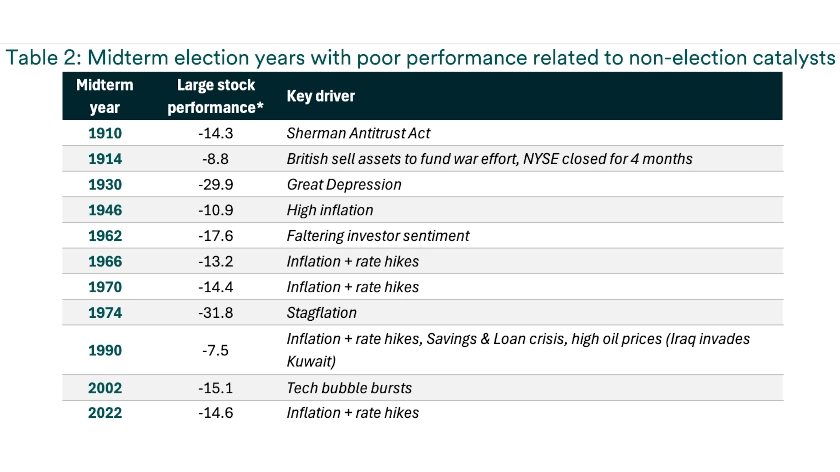

Economic and geopolitical events help explain many of the weakest midterm-year results. Of the 31 elections in the study, 11 coincided with developments such as inflation shocks, rising interest rates, the Great Depression, war or financial stress. These forces had a more direct connection to business activity, corporate profits and investor confidence than the elections themselves.

The economy remains the primary engine of market returns. Elections can influence fiscal policy and regulation, but the economic backdrop often determines how markets respond.

The economy remains the primary engine of market returns. Employment, consumer spending, inflation, interest rates and corporate earnings affect company revenues, expenses and financing conditions. Elections can influence fiscal policy and regulation, but the economic backdrop often determines how markets respond.

Statistical testing also found that the differences between midterm years and other years were not large or consistent enough to establish a reliable election effect. A t-test, which evaluates whether the difference between two groups likely reflects a recurring pattern rather than random variation, did not show that midterm elections consistently changed returns. 1 The limited sample of 31 elections and the wide range of outcomes, from losses of more than 30% to gains approaching 50%, also restrict the conclusions investors can draw from the averages alone.

The historical record becomes more useful when investors examine the events surrounding negative returns. Inflation, Federal Reserve policy, wars, financial crises and changes in business conditions provide important context for several weak midterm years. These examples reinforce the case for viewing elections as one part of the market outlook rather than as an independent investment signal.

Investors should also distinguish between a recurring historical pattern and a dependable forecast. Elections take place within different economic and market environments, making direct comparisons difficult. The conditions surrounding each election can shape returns more than the election itself.

The 2026 results may influence taxes, fiscal policy, trade, regulation and other policies that affect economic growth and corporate earnings. Continued Republican control could provide greater alignment with the president’s agenda, although Senate voting thresholds would still constrain some legislation. A divided government could limit major policy changes and place greater emphasis on areas where the parties can reach agreement.

Policy proposals may also change as the campaigns develop and election prospects shift. Investors should assess individual proposals based on their potential economic and business effects rather than assume that either party’s success will produce a predictable market result. The historical evidence does not show that one configuration of political control consistently delivers stronger stock returns.

Midterm elections can affect fiscal policy and investor sentiment, but economic fundamentals generally play a larger role in long-term market performance. The job market, household spending power, inflation, interest rates and corporate earnings offer more useful signals about the market outlook. Investors can account for political uncertainty by staying diversified, matching portfolio risk to their time horizon and avoiding large tactical shifts based only on election headlines.

The results may change the direction of specific policies, but history does not support rebuilding an investment strategy around which party controls Congress. A wealth management professional can help you assess how market conditions and policy developments relate to your goals. Stay informed with the latest market news impacting investors.

This information represents the opinion of Wealth Management of U.S. Bank and U.S. Bancorp Investments. The views are subject to change at any time based on market or other conditions and are current as of the date indicated on the materials. This is not intended to be a forecast of future events or guarantee of future results. It is not intended to provide specific advice or to be construed as an offering of securities or recommendation to invest. Not for use as a primary basis of investment decisions. Not to be construed to meet the needs of any particular investor. Not a representation or solicitation or an offer to sell/buy any security. Investors should consult with their investment professional for advice concerning their unique situation. The factual information provided has been obtained from sources believed to be reliable but is not guaranteed as to accuracy or completeness. Any organizations mentioned in this commentary are not affiliated or associated with U.S. Bank or U.S. Bancorp Investments in any way.

Investors are increasingly focused on how the administration’s policy changes are impacting markets and the economy.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.