Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Reinsurance investments can offer qualified investors income potential with return drivers that differ from stocks and bonds.

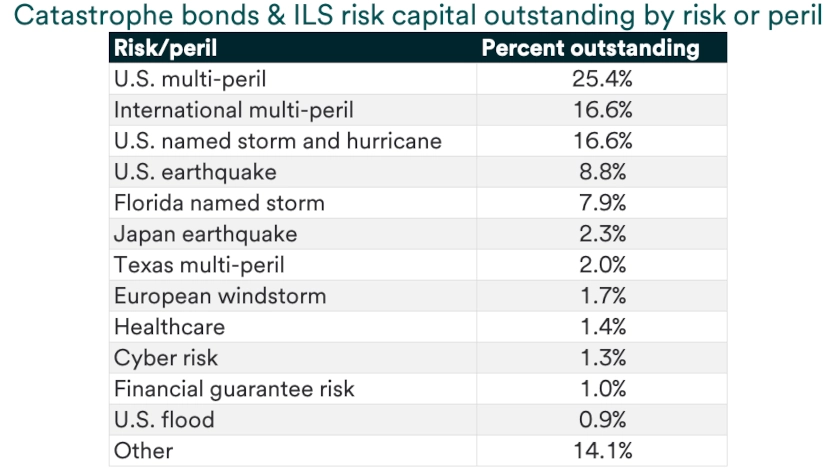

Catastrophe bonds and insurance-linked securities tie returns to insured events, premium pricing and contract triggers.

Investors should weigh natural disaster risk, climate-related exposure, liquidity and pricing discipline before allocating.

Reinsurance is drawing more interest as qualified investors look for return sources that do not depend primarily on the traditional business cycle. Instead of relying on corporate earnings, consumer demand or interest rate changes, reinsurance strategies seek to capture income from insurance premiums. This can add diversification potential because results often depend on insured events and pricing discipline rather than the same forces that typically drive stocks and bonds.

“Unlike stocks and bonds, performance of insurance-linked securities is not tied to the economic cycle or shifting investor sentiment.”

Natalie Burke, co-head of public markets manager research with U.S. Bank Asset Management Group

This overview explains how reinsurance investing works, what drives returns, and where investors should focus their risk analysis. The opportunity starts with income, but the risks can be meaningful when major catastrophes trigger insurance claims. Investors should evaluate whether the premium income they receive adequately compensates them for the specific event risks they accept.

Reinsurance plays an important role in the insurance industry. Insurance companies do not keep every risk on their own balance sheets. They regularly transfer a portion of potential claim obligations from catastrophes, such as hurricanes and earthquakes, to reinsurers, paying premiums in exchange for that protection.

Reinsurance investors receive income for taking on some of that risk. They may also experience losses if claims cross a specific threshold defined in the contract. For example, a contract may require damages to reach $500 million before coverage activates, and investors begin to absorb losses.

Reinsurance can help investors pursue income while adding a return source that behaves differently from traditional assets. Its results often connect more directly to insured event activity and insurance premium pricing than to consumer spending, corporate profits or recession dynamics. That distinction can make reinsurance a useful complement to stocks and bonds for qualified investors who can tolerate event-driven risk.

Catastrophe bonds, often called cat bonds, connect investors directly to defined catastrophe risks, such as hurricane damage, through a rules-based structure. If a specified event occurs and meets the bond’s trigger terms, the bond helps pay insurance companies for covered claims and investors may see a reduction in their principal. If the event does not trigger losses, investors can earn income that reflects the price of underwriting that risk.

Catastrophe bonds are part of a broader market known as insurance-linked securities, or ILS. These securities link investor returns to insured events rather than traditional corporate or government borrowers. That structure creates distinct risks, but it also creates a potential return source that qualified investors may not get from conventional stocks or bonds.

Investors can use catastrophe bonds and other insurance-linked securities to access return and risk characteristics that may look different from traditional investments. The appeal comes from earning income tied to insured events rather than the business cycle. For portfolios built around stocks and bonds, that difference can support diversification when traditional assets move together.

Investors should still size allocations carefully. Catastrophe bonds can lose value when insured losses exceed contract thresholds. The structure works best when investors understand the risk they are underwriting and can remain patient through event-driven periods of volatility.

The basic return math is straightforward, even though the risk modeling can be complex. Insurance companies pay premiums to transfer specific risks, and those premiums become an income source for ILS investors. Investors benefit when premium income exceeds loss payouts from covered catastrophic events.

Losses typically show up through declines in a bond’s principal value. In plain terms, investors receive income for accepting the possibility that a defined event could reduce the value of their investment. The key question is whether the income offered provides enough compensation for the size, frequency and timing of potential losses.

One useful way to understand reinsurance is to compare it to corporate bonds, while recognizing the loss trigger differs. “Corporate bond investors receive a stream of income but may occasionally incur a credit loss if the bond issuer is unable or unwilling to make timely principal and interest payments,” says Natalie Burke, co-head of public markets manager research with U.S. Bank Asset Management Group. “Investors must determine whether the income stream is sufficient to offset periodic credit losses of varying magnitude. It is similar with reinsurance, with losses determined by specific catastrophic loss events.”

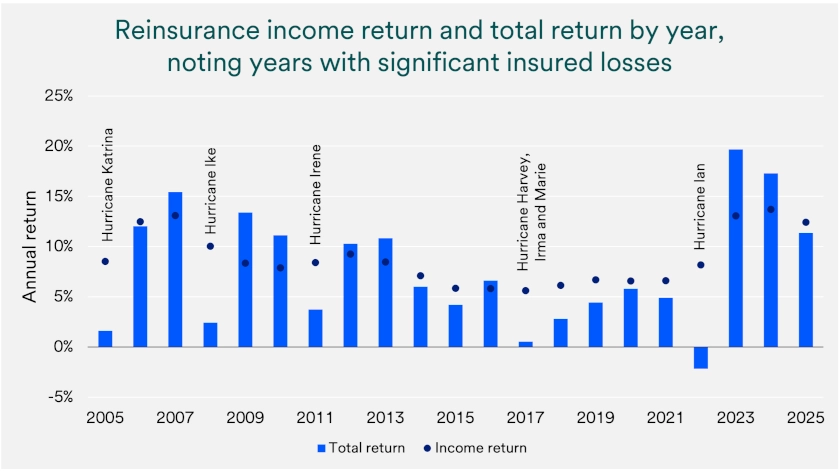

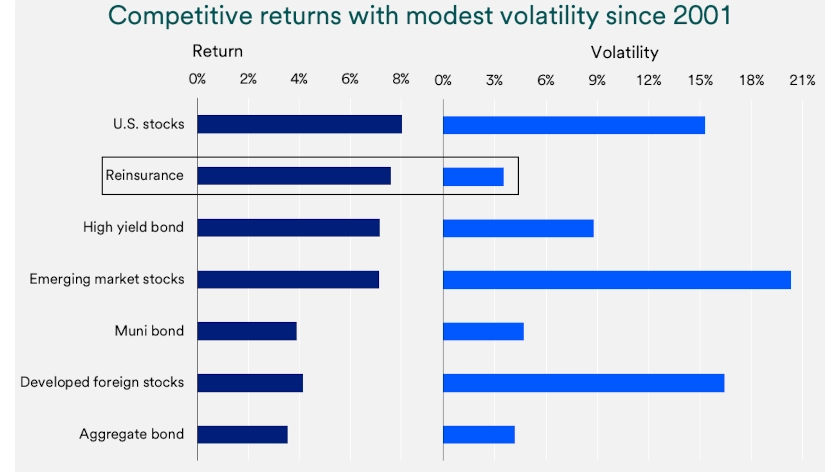

Reinsurance returns vary because catastrophic events do not follow a predictable schedule. Historical results show annualized returns exceeding 7% since 2002, comparing favorably with high-yield bonds and U.S. equities over the same period. 1 Those results came with lower annualized volatility.

Income distributions have historically accounted for much of reinsurance’s total return. That income can help cushion portfolios during years with severe insured losses, although it cannot eliminate the risk of principal declines. Investors should focus on the balance between income potential, event exposure and the timing of their purchases and redemptions.

A central appeal of reinsurance is that its return drivers can differ from what moves equities and core fixed income. “Unlike stocks and bonds, performance of ILS is not tied to the economic cycle or shifting investor sentiment,” says Burke. “This is because of its different risk sources, specifically losses from catastrophes rather than a downturn in the business cycle.”

Reinsurance does not remove risk or guarantee positive returns when other assets decline. It may add a return stream tied to insurance pricing, catastrophe risk and contract design rather than corporate profits, interest rates or broad investor sentiment. That difference can help investors broaden their return sources.

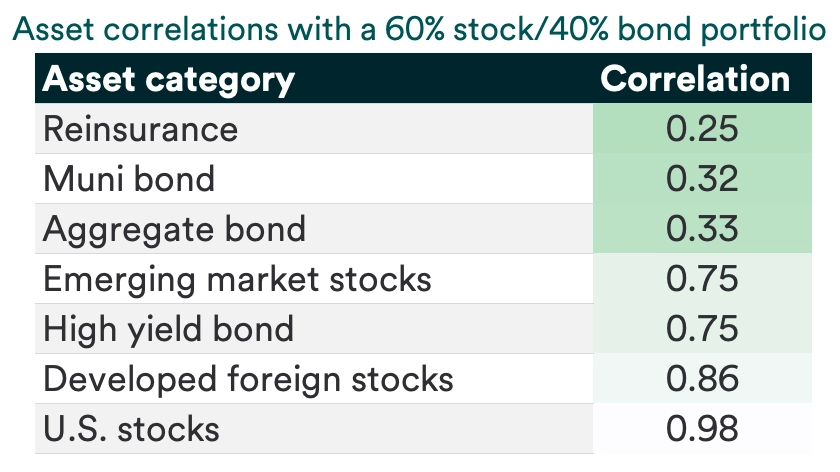

Diversification is not about finding something that always rises. It’s about combining assets that do not behave the same way at the same time. Correlation measures how closely different investments move together, with a correlation near 1.0 indicating similar movement and a correlation near -1.0 indicating movements in opposite directions.

Over a 24-year period, reinsurance showed low correlation versus a 60% stock/40% bond portfolio. Lower correlation can support diversification when investors combine assets thoughtfully. Correlations can change over time, and outcomes still depend on purchase timing, premium pricing, and the specific catastrophe risks an investor accepts.

Reinsurance also reflects the world’s evolving insurance needs. Developed economies still dominate the insured asset market, but emerging economies may require more coverage if recent trends continue. Broader coverage needs could expand the opportunity set for reinsurers and ILS investors while providing capital that supports growing overseas insurance demand.

The primary risk is clear: major natural disasters can produce substantial losses. Investor outcomes can also shift based on purchase and redemption timing, changes in premium pricing and the frequency, magnitude, and location of insured events. The most important investor question is whether the premiums earned provide enough compensation for the specific risks being underwritten.

Reinsurance risk is not uniform. A strategy concentrated in hurricane exposure may behave differently from one with broader peril or geographic diversification. Investors should look beyond headline income and understand what events could trigger losses, how much principal could be at risk and how easily they can exit the investment vehicle.

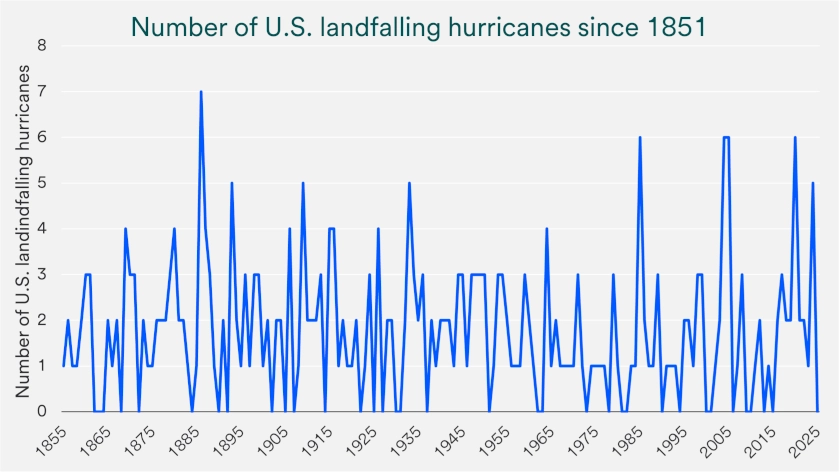

Catastrophes create financial risks for reinsurance investors and devastating human consequences for affected communities. Climate discussions often focus on whether disasters are becoming more frequent or severe. According to the National Oceanic and Atmospheric Administration (NOAA), landfalling hurricanes have not significantly increased since data became available in 1851. 2

Even if storm counts do not rise meaningfully, exposure can still increase. Higher population density, rising insured property values, and expansion into areas exposed to damage can increase potential losses. For reinsurance investors, severity and insured exposure can matter as much as the number of events.

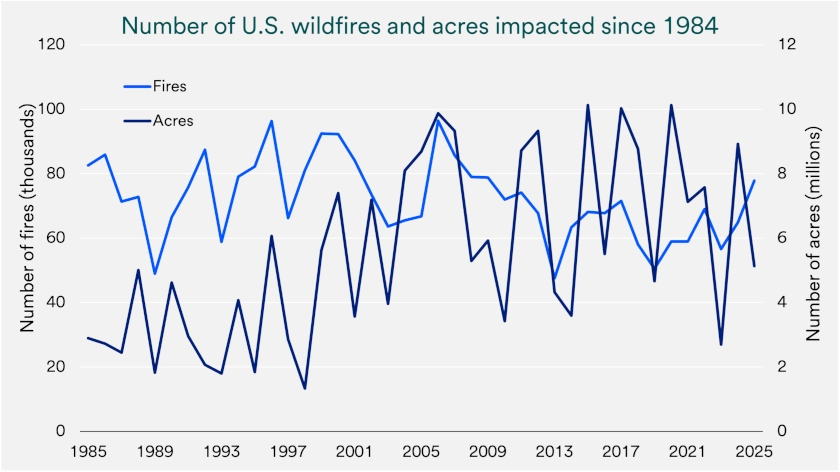

Wildfires also draw significant attention, but reliable historical data can be more limited. National Interagency Fire Center data since 1984 indicate that the number of wildfires has decreased while the area burned has increased in recent years. 3 For reinsurance investors, the size of losses can matter more than event counts alone.

Reinsurance pricing can adjust as conditions change. Unlike many traditional bonds with fixed coupon payments, reinsurance contracts can reflect updated views of risk after major loss events. “Reinsurers typically modify premiums to reflect changing loss expectations,” says Burke. “Expectations are derived based on data assessing the risk of natural disasters occurring and potential losses associated with them.”

This pricing flexibility is an important part of the investment logic. After major losses, insurers and reinsurers may seek higher premiums to reflect updated risk assumptions and rebuild capital. Investors should watch whether premium increases adequately compensate for changing loss expectations.

Insurance and reinsurance companies have strong motivation to price risk conservatively enough to remain profitable and maintain credit strength. “In the wake of significant losses due to more frequent or severe catastrophes, insurance companies apply premium increases to help rebuild capital, retain strong credit ratings, and bolster their ability to meet future claims,” says Burke. “Insurers will utilize premium hikes to address rising climate-disaster-related claims.”

Those incentives do not eliminate potential investor losses. They do, however, explain why pricing discipline is central to the reinsurance market. A healthy market needs enough capital to meet claims and enough income potential to attract investors willing to bear catastrophe risk.

Over the past 20 years, publicly traded U.S. insurance companies posted strong profitability, with annualized earnings growth slightly higher than the S&P 500. That record suggests insurers have generally assessed and priced evolving risks effectively rather than simply absorbing losses over time. For investors, a resilient underwriting ecosystem helps keep insurance premium markets functioning through event cycles.

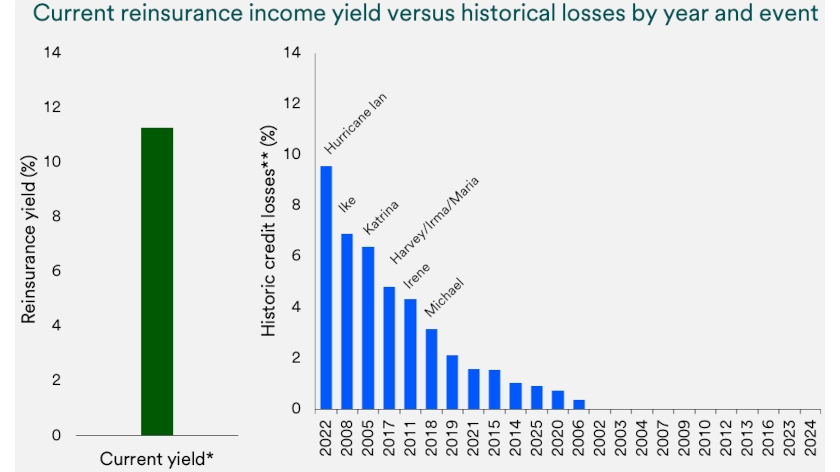

As of June 2026, recent reinsurance income significantly surpassed average historical losses. “This indicates an ability for reinsurance investments to deliver strong results even if natural disaster losses exceed historical norms,” says Burke. “Long-term investors may benefit from a combination of portfolio diversification, substantial current income, and the cushion that income provides to help offset potential losses from excessive claims.”

Investor access has expanded as the insurance and reinsurance markets have grown and the need for underwriting capital has increased. Hedge funds originally served as a key entry point, but they often require longer commitments and offer limited liquidity. Over time, interval, mutual fund and exchange traded funds have broadened access.

Each vehicle offers a different tradeoff between access, liquidity and investment flexibility. Interval funds do not trade on public exchanges, but they typically offer periodic redemption opportunities, subject to possible limits if redemption requests exceed available capacity. Mutual funds, meanwhile, provide the highest liquidity through daily trading.

Reinsurance lets insurance companies transfer some of their potential claim obligations to another party (a reinsurer) in exchange for premiums, so the original insurer doesn’t keep every risk on its own balance sheet. As an investor, you can access this risk transfer market through instruments such as cat bonds, where you earn premium-like income when covered events do not trigger losses.

If a defined catastrophe occurs and meets the contract’s trigger terms, the insurer receives funds and you may lose some principal, so returns depend on whether premium income outweighs event-driven losses over time.

Investors typically use reinsurance as a complement to stocks and bonds, sizing it thoughtfully to add another income stream with different drivers than corporate earnings or interest rate shifts.

You can gain exposure through several vehicle types – hedge funds, interval funds, mutual funds or exchange traded funds – each offering a different tradeoff between return potential and liquidity.

In practice, you align the structure (and its liquidity) with your goals and constraints, then evaluate the specific event exposures you are underwriting so the premium potential compensates you for the risks you assume.

Reinsurance can diversify portfolios because its results often link to premium pricing and insured event outcomes rather than the traditional business cycle that tends to drive stocks and core bonds. Over long periods, reinsurance has shown low correlation versus a traditional 60/40 stock-bond mix, which can help when stock bond correlations rise at the wrong time.

Diversification still depends on timing, pricing, and the exact risks you choose, so you benefit most when you combine reinsurance with other assets intentionally rather than expecting it to “always zig when others zag.”

Reinsurance can add a differentiated return stream to portfolios when used thoughtfully and sized appropriately. It can also reward patience, because income distributions often do much of the long-term work while losses arrive episodically.

The next practical step is to evaluate structure, liquidity, and risk exposures with your wealth professional to see if an allocation matches your goals, constraints, and tolerance for event-driven drawdowns.

For qualifying investors with concentrated stock positions, exchange funds may provide an appealing combination of diversification, long-term returns and tax benefits.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.