Weekly Economic Outlook

Data-driven insights from the week’s economic reports

Business-focused analysis from the U.S. Bank Economics Research Group

July 31, 2026

The week’s economy at a glance

Strong enough to worry the Fed

This week’s economic data reinforced a theme that has persisted throughout much of 2026. The U.S. economy continues to outperform expectations, even as consumers remain cautious and price pressures remain uncomfortably high. Stronger-than-expected underlying demand, resilient consumer spending, and improved June inflation readings suggest the economy entered the second half of the year on solid footing. However, new tariffs and renewed conflict involving Iran have the potential to reverse some of that progress in the months ahead. The Federal Reserve’s increasingly hawkish tone underscores that policymakers remain focused on upside risks to prices rather than growth concerns. For now, the economy appears strong enough to keep the expansion intact, but not yet soft enough to convince the Fed that its inflation fight is over. Against that backdrop, we now expect the Federal Reserve to raise the policy rate by 25 basis points in September.

What this means for business: Consumer demand continues to hold up better than many expected, suggesting the economic expansion remains on solid footing. However, with inflation still above target and the Fed increasingly focused on price stability, businesses should be prepared for borrowing costs to remain elevated and the possibility of policy tightening if inflation fails to improve.

ECONOMIC DATA OF THE WEEK

3.2%

Consumer spending rose at a 3.2% annualized pace in the second quarter, marking a notable acceleration from the first quarter and underscoring the continued resilience of household demand. While headline GDP growth came in softer than expected, consumers remained a key source of strength, helping offset weaker contributions from other components of economic activity.

The figure also highlights an important theme running through much of this week's economic data: consumers may be cautious, but they're not pulling back. Confidence remains subdued, labor-market perceptions have softened, and affordability concerns persist. Yet household spending continues to expand at a pace consistent with steady economic growth.

ECONOMIC REPORT OF THE WEEK

Q2 GDP

If consumer spending was the week’s standout number, the second-quarter GDP report showed why it mattered so much. Real GDP increased at a 1.5% annualized pace in the second quarter, below expectations and down from 2.1% in the first quarter. However, the headline figure masked a significantly stronger underlying picture. Consumer spending accelerated sharply, business and residential investment remained supportive, and real final sales to private domestic purchasers – a key measure of underlying demand – surged 3.9% annualized, more than double its first-quarter pace.

The divergence between headline GDP and underlying demand largely reflected weakness outside the private sector. Trade, inventories, and government spending all weighed on overall growth, obscuring the continued resilience of households and businesses. As a result, the report offered little evidence that the economy is losing momentum in a meaningful way. Instead, the details suggest economic activity remained on relatively firm footing through the second quarter.

CHIEF ECONOMIST QUOTE OF THE WEEK

“Taken together, this week’s reports suggest the economy entered the second half of the year on firm footing. The robust private sector strength was hidden by the weak headline number. Together with three hawkish dissents in the same direction, which was the first time in 10 years, it seems now the questions for the FOMC are when they'll raise rates and whether Fed Chair Warsh will agree with the vote.”

― Beth Ann Bovino, Chief Economist, U.S. Bank

Economic trends: Business cycle indicators

June personal income, spending and inflation: Encouraging progress, lingering questions

Consumer spending remained firm in June, providing a strong finish to the second quarter. Real consumer spending increased 0.4% in June (2.5% year-over-year, or YoY), matching expectations and extending a healthy string of gains through the spring. Real disposable income rose a more modest 0.3% month-over-month (MoM), and 0.5% YoY, as lower energy prices provided some relief to household purchasing power. Taken together, the report suggests consumers entered the second half of the year with spending momentum intact, even as income growth remains relatively subdued. The personal saving rate also fell to a four-year low of 2.7%, underscoring households' continued willingness to spend rather than rebuild savings.

There was also encouraging news on inflation. The Federal Reserve's preferred inflation measure declined 0.1% over the month in June, while core Personal Consumption Expenditures (PCE) inflation rose a modest 0.1% MoM. On a year-over-year basis, headline PCE inflation eased to 3.7%, while core inflation edged down to 3.3%. The improvement was aided by a mid-June decline in energy prices, which provided some relief to household budgets and pushed headline inflation lower. That said, inflation remains well above the Fed’s 2% target, and the recent rebound in oil prices amid renewed tensions in the Middle East suggests some of June’s improvement may prove temporary.

From a policy perspective, the June PCE report is unlikely to materially alter the broader narrative. Inflation is moving back in the right direction, but progress remains uneven and price pressures have not fully subsided. Combined with the stronger-than-expected picture of underlying demand revealed in the second-quarter GDP report, June’s data suggest the economy remains resilient enough to keep policymakers tightly focused on inflation rather than growth concerns. The result is a backdrop consistent with U.S. Bank Economics Research Group’s expectation that additional policy tightening remains possible later this year should inflation fail to continue moving lower.

Economic trends: Monetary policy

Fed holds steady, but the debate is shifting

The Federal Reserve left its target range for the federal funds rate unchanged at 3.50%-3.75% following its July meeting, extending the pause that has been in place since January. At first glance, the decision appeared uneventful. The post-meeting statement was largely unchanged from June, suggesting policymakers’ overall assessment of economic conditions has shifted little over the past six weeks. However, the 9-3 vote revealed a notably more divided Committee than in recent meetings, with Cleveland Fed President Hammack, Minneapolis’ Kashkari, and Dallas’ Logan dissenting in favor of a 25-basis-point rate increase. The three dissents in the same direction hasn't happened since 2016.

The dissents are significant because they suggest concerns about inflation are no longer confined to a single policymaker or region of the country. While a majority of participants concluded that current conditions warranted leaving rates unchanged, the presence of three votes for a hike highlights growing unease about the pace of inflation improvement and whether current policy is sufficiently restrictive. At a minimum, the vote indicates that support for higher rates has become increasingly visible within the Committee, even if it has not yet become the consensus view.

With no updated Summary of Economic Projections released at this meeting, Chair Kevin Warsh’s press conference took on added importance. Warsh described the economy as showing "impressive resilience" and reiterated that inflation remains above the Fed’s objective. At the same time, he offered little indication that policymakers are committed to any particular course of action in coming months, emphasizing instead the importance of assessing broader economic and financial conditions rather than reacting to any single data release. Taken together, his comments suggested a Fed that remains focused on restoring price stability, but one that is not yet prepared to signal when, or if, a pivot toward tightening might occur.

For now, the July meeting leaves the Fed on hold, but it also underscores that the policy debate is evolving. Stronger-than-expected private-sector demand, still-elevated inflation, and a growing number of policymakers advocating tighter policy suggest the Committee’s focus remains firmly on inflation rather than growth concerns. Consistent with our outlook, the meeting does little to rule out the possibility of additional tightening later this year should inflation fail to continue moving lower.

Economic trends: Business cycle indicators

Consumer confidence: Softer current conditions, subdued expectations

Consumer confidence edged lower in July, reinforcing a cautious but not sharply deteriorating household backdrop. The Conference Board’s Consumer Confidence Index declined to 90.8 (from an upwardly revised 92.2 in June), remaining below its long-run average and well under levels seen late last year. The decline was concentrated in consumers’ assessment of current conditions, with the Present Situation Index falling for a third consecutive month to 114.9. Meanwhile, the Expectations Index held steady at 74.7, albeit still below the 80 threshold historically associated with elevated recession risk.

The labor market details continue to warrant attention. The labor market differential – the share of consumers saying jobs are “plentiful” minus those saying jobs are “hard to get” – narrowed to +3.1, its lowest level since early 2021 amid the pandemic. Importantly, the move was not driven by a sharp increase in consumers reporting jobs are hard to find, but rather by fewer respondents saying jobs are plentiful. That nuance matters, as layoffs still appear contained but consumers are increasingly sensing a less favorable hiring environment. The report remains consistent with a ‘low-hire, low-fire’ labor market – one that is stable for many workers already employed, but more challenging for job seekers.

Price concerns also remain a constraint on confidence, even as some measures of inflation expectations have cooled. Consumers’ references to oil and gas prices eased but remained elevated, while mentions of food and grocery prices increased. That mix helps explain why confidence has struggled to improve meaningfully even as consumer spending has held up better than sentiment surveys might imply. Households are not signaling a broad pullback, but they remain sensitive to affordability pressures and increasingly selective in how they might allocate spending.

Taken together, July’s report points to a consumer sector that is still growing, but with less cushion. Confidence about current conditions is gradually weakening, labor market perceptions are softening, and expectations remain subdued. At the same time, the report does not suggest a sudden pullback in household demand. For now, the message remains one of continued caution.

Economic trends: The week ahead

Data and reports we’re watching this week: Labor market stability under the microscope

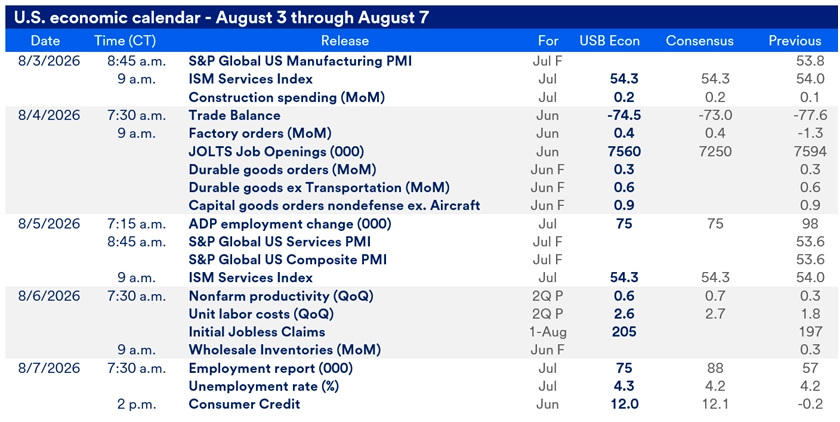

Attention this week turns to labor market conditions, with Tuesday’s June Job Openings and Labor Turnover Survey (JOLTS) and Friday’s July Employment Report providing fresh insight into labor demand and hiring trends. Over the past several months, the narrative has shifted from concerns about gradual weakening to growing confidence that the labor market has found a sustainable equilibrium. This week’s releases should help determine whether that picture remains intact as the economy moves through the second half of the year.

Tuesday’s June JOLTS report will provide an updated read on labor demand. We expect job openings to remain relatively steady at 7.56 million, little changed from May’s 7.59 million. Demand for workers likely remained strongest in healthcare, while leisure and hospitality may have continued to benefit from World Cup-related activity. Meanwhile, we expect the quits rate to hold near recent levels or edge slightly lower, reinforcing the view that worker mobility remains subdued and that labor market churn is no longer contributing meaningfully to inflation pressures.

The week’s focal point will be Friday’s July Employment Report. We expect nonfarm payroll growth of 75,000 (consensus: 88,000), up modestly from June’s 57,000 increase and consistent with continued expansion in employment. Some sectors that likely benefited from temporary World Cup-related hiring, particularly leisure and hospitality, may see partial reversals in July, while construction payrolls could also soften. At the same time, healthcare and other service-producing industries should continue to provide underlying support.

We expect the unemployment rate to tick up to 4.3% from 4.2% in June. Last month’s decline was driven in part by a drop in labor force participation, particularly among younger prime-age workers. We expect much of that weakness to prove temporary, with labor force participation rebounding modestly and pushing the unemployment rate slightly higher even as broader labor market conditions remain stable.

Taken together, this week’s data releases are likely to reinforce a picture of a labor market that has settled into a low-hire, low-fire equilibrium. Job growth remains sufficient to support continued expansion, labor demand appears steady, and layoffs remain subdued by historical standards. Such an outcome would leave Federal Reserve officials focused primarily on inflation developments.

Economic data calendar this week

What we’re watching this week, including release dates and projections from the U.S. Bank Economics Research Group.

Federal Open Market Committee (FOMC) Speaker Calendar

- August 5, 3:05 p.m.: Cook (Board of Governors/Voter)

- August 6, 6:30 p.m.: Musalem (St. Louis Fed/Non-Voter)

- August 7, 9 a.m.: Barkin (Richmond Fed/Non-Voter)

Next update: Week of August 10

For additional insights, see our Monthly Macroeconomic Outlook and Chief Economist Beth Ann Bovino’s latest commentary.

If you have any questions about any of the topics above or want to learn more, please contact us to connect with a U.S. Bank corporate and commercial banking expert.

Not currently a subscriber? Sign up to get our economic insights delivered to your inbox weekly.

Sources: U.S. Bank Economics, Bloomberg, U.S. Bureau of Economic Analysis (BEA), Federal Reserve, Conference Board

Tags:

U.S. Bank Economics Research Group

Beth Ann Bovino

Chief Economist

Ana Luisa Araujo

Senior Economist

Matt Schoeppner

Senior Economist

Adam Check

Economist

Andrea Sorensen

Economist

Past weekly reports

Visit the archive to read previous outlook reports from the U.S. Bank Economics Research Group.

Learn more

If you have any questions about any of these topics or want to learn more, please contact us to connect with a U.S. Bank Corporate and Commercial banking expert.