A “low-hire, low-fire” economy reflects the labor market’s current state, with slower new job creation combined with near-historically low unemployment rates and relatively steady layoff activity. In the current economic environment, although employers are creating even fewer new jobs, they appear reluctant to initiate major workforce reductions. “The combination of slower job growth but still low unemployment reflects a sharp drop in both labor demand and labor supply,” says Matt Schoeppner, senior economist, U.S. Bank. “That leaves the labor market less dynamic and increasingly vulnerable to downside risk.”

Article

U.S. labor market: Defensive stability in a low-hire, low-fire economy

July 15, 2026

Key takeaways

The U.S. labor market remains in an unusual phase characterized by restrained hiring, low layoffs and muted job churn.

Low layoffs have helped keep unemployment relatively low even as hiring remains subdued, though recent job gains suggest labor market conditions may be stabilizing.

Slower labor-force growth has lowered the “breakeven” pace of job creation needed to maintain labor market balance, changing how payroll gains should be interpreted.

The key question is whether this low‑momentum equilibrium can persist – or whether limited churn leaves the labor market more exposed if layoffs begin to rise.

The U.S. labor market maintains an unusual condition defined by limited job creation and persistently low unemployment – an arrangement that appears stable, but increasingly defensive in nature. This is what former Federal Reserve Chair Jerome Powell has previously described as a “low-hire, low-fire” economy. 1

One of the clearest signs of this shift has been slower payroll growth. From January 2025 through June 2026, employers added an average of just 37,000 jobs per month, down from more than 200,000 during the previous three years. Yet unemployment has remained relatively low. 2 This divergence highlights how slower labor-force growth has reduced the pace of hiring needed to keep unemployment stable. More recent data suggest hiring conditions may be stabilizing after a prolonged slowdown, though evidence of a sustained reacceleration remains limited.

“The labor market's key stabilizing factor is that layoffs remain low," says Matt Schoeppner, senior economist, U.S. Bank. "As long as job losses remain contained, the labor market can hold in a relatively stable – albeit subdued – equilibrium." That stability, however, has been driven more by limited separations than robust hiring. The unemployment rate stood at 4.2% in June 2026, 2 even as employers appeared increasingly reluctant to expand headcount. "The combination of still-low unemployment and slower job growth reflects a pullback in both labor demand and labor supply," says Schoeppner. "With labor-force growth slowing, the economy no longer requires the same pace of job gains to keep unemployment stable. That helps explain why hiring conditions can appear subdued while unemployment remains low.”

Is the jobs market at an inflection point? While it remains too early to declare a definitive trend, recent data suggest conditions have stabilized following a prolonged slowdown. Payroll growth has averaged 111,000 over the past three months – well above the pace seen across much of the past year – while layoffs have remained subdued and unemployment low. "In addition to firmer job gains earlier this spring, businesses have been hiring more temporary workers and maintaining hours for existing employees, suggesting they are preserving workforce capacity despite slower hiring," says Beth Ann Bovino, chief economist, U.S. Bank. Hiring temporary workers and maintaining hours often signal that firms are operating closer to capacity and may need to add permanent staff in the coming months.

Bovino notes that "while there is still some volatility in the data, the labor market remains closer to a 'low-hire, low-fire' state than a renewed hiring cycle. The encouraging sign is that layoffs remain contained and unemployment remains low. The caution is that hiring has yet to show sustained reacceleration. For now, the labor market appears to be finding balance through limited worker turnover and slower labor-supply growth rather than stronger job creation.”

“With labor-force growth slowing, the economy no longer requires the same pace of job gains to keep unemployment stable.”

-

Matt Schoeppner, senior economist, U.S. Bank.

Examine the issues

The low-hire, low-fire labor market: Stability on the surface, vulnerability beneath

Slowing job growth reflects changing demographics

While the recent slowdown in job growth may raise concerns, it also reflects longer-term demographic shifts reshaping the labor market. “A notable change underway is that the number of retirees is rising, fewer babies are being born, and net immigration has diminished,” says Bovino. “As a result, the ‘breakeven’ pace of job growth needed to maintain a stable unemployment rate has declined considerably from past cycles.”

That distinction is becoming increasingly important when interpreting labor market data. In previous cycles, payroll growth of less than 100,000 jobs per month would have been viewed as a clearer sign of labor market weakness. Today, however, slower labor-force growth means the economy can generate fewer jobs while still keeping unemployment relatively stable.

The 'breakeven' employment growth rate – the pace of payroll growth needed to keep unemployment steady – is a key labor market benchmark. In recent years, that figure was estimated to be as high as 250,000 jobs per month, reflecting strong immigration flows and rapid labor-force growth. Today, however, U.S. Bank Economics estimates the breakeven rate has fallen to roughly 25,000 to 50,000 jobs per month.³

“The lower breakeven rate helps explain how unemployment can remain in the low-4% range even as job growth has slowed,” says Matt Schoeppner, senior economist, U.S. Bank. “It also highlights a decline in labor market dynamism.” While layoffs remain near historic lows, job openings have trended lower, fewer workers are voluntarily leaving their jobs, and the hiring rate has fallen to post-pandemic lows. “Taken together, these are classic signs of a low-churn labor market,” he adds.

Job openings flatten out

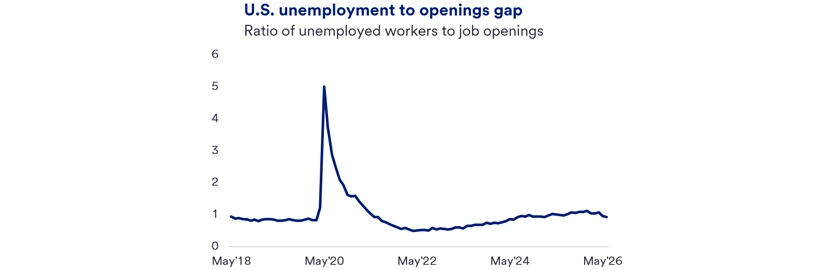

The labor market continues to adjust to the dramatic shift set in motion by the COVID-19 pandemic. After the economy virtually shut down in early 2020 – temporarily displacing millions of workers – the recovery that followed was rapid, with job openings far outpacing available workers for an extended period.

That imbalance has since faded. Today, the ratio of job openings to job seekers has returned to roughly one-to-one. This normalization reflects both the Federal Reserve's efforts to cool demand and a shift in employer behavior, as firms have grown more cautious about hiring while prioritizing retention over recruitment.

Recent Job Openings and Labor Turnover Survey (JOLTS) data suggest labor demand has stabilized at lower levels. Job openings held relatively steady in May, while hiring remained subdued, workers continued to quit at a slower pace, and layoffs stayed contained. Schoeppner notes that, taken together, these trends point to a labor market with relatively little turnover. "Employers still have positions to fill, but both workers and businesses appear increasingly reluctant to make major moves," he says. "The result is a labor market that remains stable, but considerably less dynamic than it was just a few years ago.”

Potential signs of labor market vulnerability

Concerns about the labor market remain closely tied to the still-subdued hiring environment. “So far, persistently low layoffs have served as a stabilizing force,” says Schoeppner. “When layoffs remain contained, even modest job growth can be enough to keep the labor market on steady footing.” He notes, however, that even a modest increase in layoffs could push unemployment higher, highlighting the labor market's sensitivity to downside shocks despite its current stability.

Another area worth monitoring is the pace at which workers choose to leave their jobs. While the quit rate surged in 2021 and 2022 during the post-pandemic recovery, it has since leveled off.2 “When the quit rate is high, workers are more confident they can find other employment,” says Bovino. “When it trends lower, it reflects greater caution about job opportunities.” She adds that today's environment has produced more so-called “job huggers” – workers who are reluctant to leave their current positions because attractive alternatives are harder to find.”

What’s driving the U.S. labor market slowdown

The current labor market slowdown reflects a combination of structural and cyclical forces, including:

- Slower labor-force growth. Population aging, lower birth rates, and reduced immigration have slowed labor-force growth, lowering the breakeven pace of job gains and reducing overall labor market dynamism.

- Policy and cost uncertainty. Higher tariffs and ongoing policy uncertainty have increased costs for some businesses and complicated planning decisions, potentially causing firms to delay hiring or investment – particularly in goods-producing industries.

- Federal spending restraint. Reductions in federal government spending have resulted in layoff announcements in some areas while weighing on confidence among federal contractors and related industries.

- Uneven consumer demand. Lower- and middle-income households continue to face affordability pressures, constraining discretionary spending and limiting hiring momentum in some consumer-facing sectors.

- Artificial intelligence adoption. Demand for some entry-level technology roles appears to be easing as firms reassess staffing needs amid rapid adoption of AI-driven tools. More broadly, AI may increasingly influence the composition of hiring and labor demand across industries.

Taken together, these forces point to a labor market that is becoming less dynamic than in prior years. Even so, low layoffs and slower labor-force growth have helped maintain labor market stability, allowing unemployment to remain relatively low despite more subdued hiring.

Layoffs: the key stabilizer

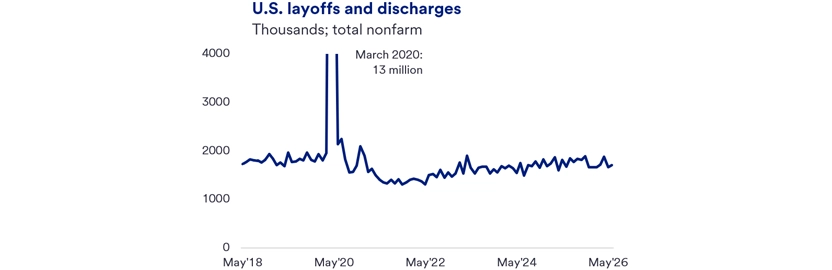

The primary firewall between today's soft patch and a broader downturn is continued restraint in layoffs. Firms remain reluctant to cut headcount after experiencing the costly post-pandemic scramble to rehire. “Businesses learned that mass layoffs can be expensive to reverse,” says Schoeppner. “Instead, many are adjusting at the margins – through hiring freezes, reduced hours, and cuts to temporary help.”

Together, these behaviors point to a labor market operating in a state of defensive stability, where employers prioritize retaining existing workers over expanding payrolls. Although hiring has slowed, firms appear willing to tolerate softer demand rather than risk being understaffed should conditions improve.

Schoeppner notes that this caution reflects how employers are adapting to a less dynamic labor market. “Many firms are stretching their existing workforce through longer hours and higher productivity expectations rather than reducing headcount,” he says. “Lower turnover has helped keep job growth modest while holding the unemployment rate relatively stable.”

Recent data reinforce this picture. Weekly initial jobless claims have hovered just above 200,000 throughout much of 2026, signaling a still-subdued layoff environment.4 Continuing unemployment claims, which rose following the government shutdown in late 2025, have since trended lower.

At the same time, the hiring rate remains near levels typically associated with periods of economic weakness. As a result, the labor market remains somewhat dependent on continued restraint in layoffs. Any meaningful increase in job losses could place upward pressure on unemployment more quickly than in past cycles, given subdued hiring and limited worker mobility. For now, however, the “low-fire” side of the labor market continues to provide an important source of labor market stability.

A new economic variable

Even amid subdued hiring, the economy appears positioned to avoid a recession in the near term as long as layoffs remain contained. The Federal Reserve's decision to cut the federal funds rate three times in late 2025 underscored its growing focus on labor market conditions. More recently, however, renewed inflation concerns – driven in part by higher energy prices and broader cost pressures – have complicated the policy outlook and may keep interest rates elevated for longer.

"The concern is that higher – and often volatile – energy prices could feed into core inflation," says Bovino. "If that keeps interest rates elevated, businesses may become more cautious about investment, which could weigh on labor demand."

Schoeppner notes that higher energy prices do not necessarily translate directly into layoffs but can pressure hiring and business expansion plans. "Energy costs eventually affect transportation, manufacturing, logistics, and warehousing," he says. "If those pressures persist, they could contribute to softer labor demand in energy-sensitive sectors."

For the Federal Reserve, the labor market signal remains mixed. Slower hiring and moderating wage growth suggest labor demand continues to cool, while low unemployment and limited layoffs indicate conditions remain relatively stable. As a result, policymakers may have room to remain patient, but not a compelling reason to keep easing policy aggressively. If inflation pressures prove more persistent, the Fed could be forced to keep policy restrictive for longer than currently expected.

Could artificial intelligence (AI) alter the labor market landscape?

There has been an extensive discussion about whether artificial intelligence is beginning to replace jobs in some industries. Schoeppner notes that with hiring already subdued, it remains unclear whether AI is materially affecting aggregate employment trends. Instead, he views AI implementation less as an immediate job-destroying shock and more as a shift in job composition and productivity.

“Employers increasingly appear to be backfilling roles rather than approving large numbers of new positions,” says Schoeppner. “Over time, AI is more likely to substitute for incremental labor demand than to directly replace existing workers.” To date, the most visible effects appear concentrated in clerical and administrative functions, particularly among some entry-level white-collar roles.

While the transition to broader AI adoption may cause some near-term adjustment, Bovino is more optimistic about the long-term implications. “As AI is implemented, it will ultimately create new jobs, new businesses and entirely new industries,” she says. “That said, the adjustment is likely to present challenges in the near term.”

A low-hire, low-fire equilibrium

In the near term, the economy appears increasingly settled into a low-hire, low-fire labor market environment. Layoff trends therefore warrant close monitoring, as persistently low job losses have played a central role in keeping unemployment stable despite slower hiring.

At the same time, slower labor-force growth has lowered the pace of hiring needed to maintain labor market balance, helping explain why unemployment has remained low even as hiring has cooled. The result is a labor market that appears stable on the surface but is considerably less dynamic than in the years immediately following the pandemic.

Looking ahead, the key question is whether this low-churn equilibrium can persist. As long as layoffs remain contained, the labor market appears capable of maintaining steady footing. However, subdued hiring and limited worker mobility suggest that future labor market performance may depend less on robust job creation and more on the continued absence of meaningful workforce reductions.

FAQ

The “breakeven” employment growth rate – the monthly pace of job creation required to maintain a steady unemployment rate and support labor market stability – is considered a key, labor-related economic measure. Today, with U.S. population growth slowing and labor-force growth moderating, U.S. Bank Economics estimates the breakeven rate has fallen to roughly 25,000 to 50,000 jobs per month. In recent years, that figure was estimated to be as high as 250,000 new jobs per month, driven at the time by strong immigration and labor force gains.3 “The lower breakeven rate partially explains how the unemployment rate can hold in the low 4-percent range even as new job creation flatlines,” says Matt Schoeppner, senior economist, U.S. Bank. “It also underscores a loss of labor market dynamism.”

The unemployment rate has remained relatively stable despite slower hiring for several reasons. While companies have tempered hiring, they also appear increasingly reluctant to reduce their workforce. As a result, the unemployment rate remains near historically low levels. Companies may be holding on to workers partially due to a slowdown in labor supply growth. Given current demographic trends, far fewer new jobs are needed each month to maintain labor market stability and a stable unemployment rate because labor-force growth has slowed sharply.3

Tags:

U.S. Bank Economics Research Group

Beth Ann Bovino

Chief Economist

Ana Luisa Araujo

Senior Economist

Matt Schoeppner

Senior Economist

Adam Check

Economist

Andrea Sorensen

Economist

Subscribe to our economic insights newsletter

Not currently a subscriber? Sign up to get our economic insights delivered to your inbox weekly.

Learn more

If you have any questions about any of these topics or want to learn more, please contact us to connect with a U.S. Bank Corporate and Commercial banking expert.

Start of disclosure content

Disclosures

Start of disclosure content