Monthly Economic Outlook

Economic forecast: July 2026 trends and analysis

Macroeconomic insights and outlook from the U.S. Bank Economics Research Group to help guide your business strategy

July 2026

Economic outlook at a glance

Advancing to the next round

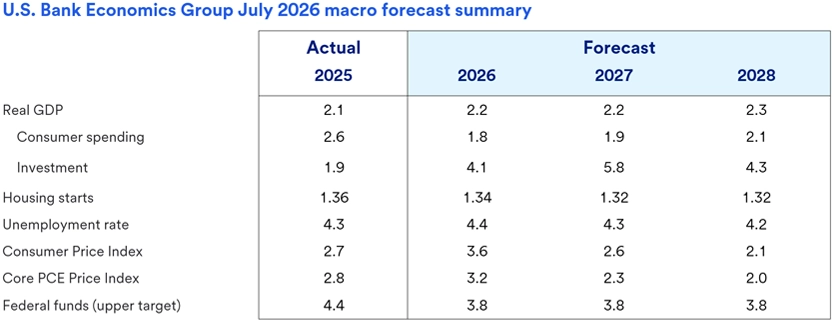

Our July 2026 U.S. economic outlook points to an expansion increasingly defined by divergence rather than broad-based strength. Consumer spending continues to support growth despite ongoing pressure on household purchasing power – with the FIFA World Cup and other summer experiences providing an additional near-term boost – while business investment remains concentrated in technology, AI, and digital infrastructure. Revised data suggest households entered the year with somewhat larger savings buffers than previously estimated, providing a modest source of support for consumption. And the labor market has found firmer footing in recent months, though June's employment report suggests hiring momentum remains uneven and conditions continue to resemble a "low-hire, low-fire" environment.

At the same time, inflation remains elevated, and progress toward the Federal Reserve's 2% objective remains uneven. While broader price pressures have not materially reaccelerated, recent data reinforce that the last mile back to target may be more persistent than previously anticipated. This combination of resilient activity, sticky inflation and a labor market finding firmer footing is likely to keep the Federal Reserve on hold through 2027. However, the June FOMC meeting signaled a more conditional and less transparent policy framework, making additional rate hikes a more credible risk.

Key takeaways:

Growth: We expect real GDP growth of 2.2% Q4-over-Q4 in 2026 (2.2% annual average) and 2.3% Q4-over-Q4 in 2027 (2.2% annual average) as consumer spending moderates amid ongoing pressure on household purchasing power. Strength in AI-related investment should continue to offset weakness in residential construction, keeping growth mostly intact.

Labor market: The labor market has found firmer footing, with low layoffs, moderate job growth, and slower labor-force growth supporting near-term stability. We expect the unemployment rate to average roughly 4.4% in 2026 before edging down to 4.3% in 2027.

Inflation: Inflation remains elevated. While lower energy prices and fading tariff pressures offer some relief, firm shelter and healthcare inflation in May suggest underlying price pressures remain stubborn. We continue to expect core Personal Consumption Expenditures (PCE) inflation to ease from 3.3% in Q2 2026 to near 2% by late 2027, though the path back to target is likely to remain uneven.

Federal Reserve: The Federal Reserve is expected to remain on hold through 2027. With labor market conditions broadly stable and inflation still above target, policymakers appear increasingly focused on the Fed's price stability mandate, making additional rate hikes a more credible risk.

Risks

We have reduced our 12‑month recession probability to 25%, reflecting resilient economic activity, a firmer labor market, lower oil prices, and easing concerns over this spring's energy shock. Nevertheless, thinning household financial buffers and the potential for renewed inflation pressures remain key downside risks to the expansion.

Macroeconomics forecast at a glance

Produced by the U.S. Bank Economics Research Group, our in-depth economic forecast examines the trends and economic indicators shaping business decisions this year and into the future.

July 2026 Report

Go beyond the highlights. Download the full monthly forecast for a comprehensive view of the economy, including all supporting data tables, charts and insights from the U.S. Bank Economics Research Group.

Get more business-focused economic analysis

For additional insights, see our weekly economic highlights and Chief Economist Beth Ann Bovino’s latest economic commentary.

If you have questions about any of the topics above or want to learn more, please contact us to connect with a U.S. Bank corporate and commercial banking expert.

Not currently a subscriber? Sign up to get our economic insights delivered to your inbox weekly.

Sources: U.S. Bank Economics, Bloomberg, Yale Budget Lab, U.S. Bank Economics calculation

Tags:

U.S. Bank Economics Research Group

Beth Ann Bovino

Chief Economist

Ana Luisa Araujo

Senior Economist

Matt Schoeppner

Senior Economist

Adam Check

Economist

Andrea Sorensen

Economist

Past monthly forecasts

Visit the archive to read previous monthly forecasts from the U.S. Bank Economics Research Group.

Learn more

If you have any questions about any of these topics or want to learn more, please contact us to connect with a U.S. Bank Corporate and Commercial banking expert.