While higher tariffs increase costs for businesses and consumers, uncertainty surrounding tariff policy often creates additional challenges. Companies may delay investments, postpone hiring plans, or alter sourcing decisions when they lack visibility into future costs or trade rules. “Businesses can typically adapt to higher costs once they understand what those costs will be,” says Matt Schoeppner, senior economist at U.S. Bank. “The greater challenge is making long-term decisions when policy outcomes remain uncertain.” As trade-policy uncertainty has diminished, businesses have gained a clearer framework for planning, even though tariff rates remain elevated.

Article

A new phase for U.S. trade policy: Moving from shock to adjustment

July 20, 2026

Key takeaways

Greater visibility into future trade policy has reduced one of the largest risks facing businesses and financial markets.

While tariffs remain a headwind to inflation and growth, their economic effects have generally proven more manageable than many initially feared.

Businesses adapted by diversifying suppliers, reconfiguring supply chains, and shifting sourcing toward alternative trading partners rather than reducing trade altogether.

Future U.S. trade debates are likely to focus less on tariff levels and more on technology, national security, and supply chain resilience.

The first half of 2026 brought no shortage of uncertainty surrounding U.S. trade policy. Legal challenges to President Trump’s tariff actions, new tariff mechanisms, ongoing sector-specific investigations, and renewed negotiations kept trade policy at the center of the economic outlook. Economists continued to worry that escalating trade tensions could reignite inflation pressures, disrupt investment decisions, and increase the risk of slower economic growth.

“Those concerns are understandable,” says Beth Ann Bovino, chief economist, U.S. Bank. “Tariffs act as a tax on imported goods, raising costs for businesses and, in many cases, consumers.” Throughout much of the past year, businesses have faced difficult decisions regarding sourcing, pricing, and investment, often without knowing whether existing tariff rates would remain in place, increase further, or eventually be negotiated lower.

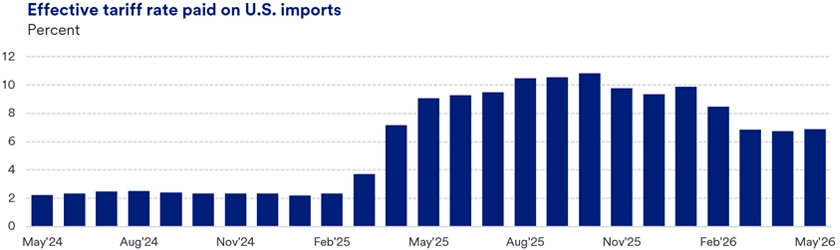

Today, the picture looks somewhat different. Effective tariff rates remain higher than they were just a few years ago, continuing to create challenges for businesses operating across global supply chains. At the same time, however, the U.S. economy has proven more resilient than many expected. Consumer spending has remained relatively strong, labor-market conditions have found firmer footing, and importers have increasingly adapted to the new trade environment.

“Perhaps most importantly, uncertainty has begun to diminish,” says Bovino. “While questions about the direction of future trade policy remain, businesses now have greater visibility into operating conditions.” As a result, the economic conversation has shifted from whether tariffs could derail growth to how importers are adapting to a world where higher tariffs will persist. In that respect, the more important development is not the level of tariffs themselves, but the growing ability of businesses to plan around a more predictable trade environment.

“Businesses can often adapt to bad news. What is much harder to adapt to is uncertainty surrounding bad news.”

-

Beth Ann Bovino, chief economist, U.S. Bank

The biggest development wasn't tariffs – it was uncertainty

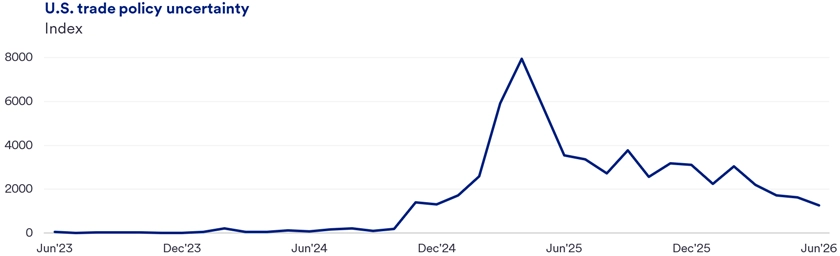

When discussing U.S. trade policy, it is easy to focus on tariff rates themselves. Yet for much of the past year, economists have been more concerned about the uncertainty surrounding trade policy than the tariffs alone.

“There was never much debate that higher tariffs would create some economic headwind,” says Matt Schoeppner, senior economist, U.S. Bank. “The bigger question was how large that drag might become.” Early in the policy rollout, businesses faced an unusually wide range of possible outcomes. Some scenarios envisioned effective tariff rates settling at or above historic highs, while others raised the possibility of further escalation, retaliatory actions by major trading partners, or broader disruptions to global supply chains.

“Those risks carried important economic implications,” says Schoeppner. “Businesses considering major investments often found themselves operating in an environment where future costs, sourcing arrangements, and customer demand were increasingly difficult to predict.” Many firms had limited visibility regarding whether tariffs would remain in place, expand to additional products, or become part of a broader series of trade restrictions.

Bovino notes that “this distinction is important because businesses can often adapt to bad news. What is much harder to adapt to is uncertainty surrounding bad news.” Companies can adjust pricing strategies, identify alternative suppliers, or modify investment plans once costs are known. But making those decisions becomes more difficult when policy itself remains in flux.

Over time, however, the outlook began to change. While tariffs remain higher by historical standards, policy outcomes have generally proven less severe than many had initially feared. Measures of trade-policy uncertainty tell a similar story, surging during the height of tariff-related concerns before declining noticeably as the range of potential policy outcomes began to narrow.1 “Trade negotiations and policy developments have provided a better sense of where effective tariff rates are likely to settle,” says Schoeppner, “while businesses have gained a better understanding of the costs they may face and how to manage them.”

As a result, analysts have become better able to evaluate the economic consequences of higher tariffs. Trade policy remains an important risk to monitor, but the range of possible outcomes appears narrower today than it did several months ago. “That increased visibility may ultimately prove just as important for economic growth and recession risk as the tariff rates themselves,” says Bovino.

Supply chains adjusted rather than broke

One of the biggest questions surrounding higher tariffs was how businesses would respond. Economists generally worried that higher import costs would disrupt supply chains, reduce trade volumes, and ultimately weigh on economic activity. Yet the experience of the past year suggests many businesses adapted more quickly than expected.

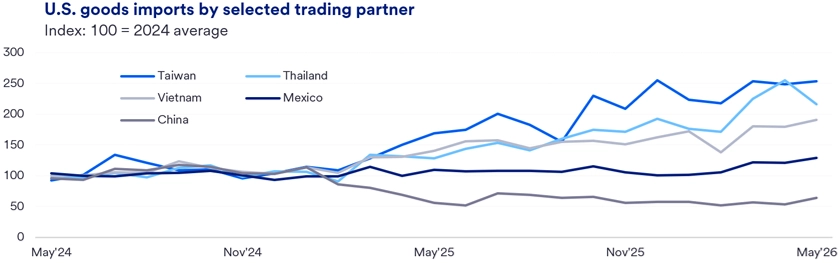

“One common assumption was that higher tariffs would simply result in less trade,” says Schoeppner. “In many cases, what occurred instead was different trade.” While imports from China have declined sharply – down roughly 35% to 40% from 2024 figures, based on U.S. Census Bureau trade data – businesses have increasingly shifted sourcing to other countries, including Vietnam, Thailand, and Taiwan.2 At the same time, near-shoring strategies – particularly toward Mexico – have gained momentum as companies look to shorten supply chains and reduce exposure to geopolitical and trade-policy risks.

This shift highlights an important distinction between trade disruption and trade reallocation. Rather than abandoning global supply chains altogether, many companies adjusted supplier networks, reconfigured logistics relationships, and diversified production across a broader set of markets. “That distinction has become increasingly important to our evaluation of tariffs,” says Bovino. “Early on, an expected outcome was less trade, but the actual outcome has been different trade.”

Trade agreements can also provide businesses with a clearer framework for long-term investment and sourcing decisions. As tariff treatment becomes more predictable, firms have become more deliberate in structuring supply chains around existing trade frameworks, even as negotiations such as those surrounding the U.S.-Mexico-Canada Agreement (USMCA) continue.

Bovino notes that this adjustment process helps explain why economic outcomes have generally proven more durable than many expected. “Businesses are remarkably adaptable when incentives change,” she says. “Once the rules become clearer, companies tend to find new ways to source products, manage costs, and maintain operations.”

Overall, while the transition has not been seamless – and many businesses continue to face higher costs and operational challenges – the evidence increasingly suggests that supply chains are evolving rather than breaking. Rather than triggering a collapse in cross-border trade, higher tariffs are instead contributing to a gradual reshaping of trade flows and production networks.

The inflation story looks more manageable

Another major concern surrounding tariffs was their potential impact on inflation. Early on, economists worried that higher import costs could lead businesses to pass those costs on to consumers, create a broad price shock, and complicate the Federal Reserve's efforts to return inflation to target.

“Tariffs are still inflationary,” says Bovino. “The question is not whether tariffs raise costs, but whether they create a lasting inflation problem or a one-time increase in prices.” That distinction has become increasingly important as the economic effects of higher tariffs grow clearer. Bovino notes that "Fortunately, the data indicates that the textbook 'one-time level shock' rather than a sustained source of inflation, still holds."

While tariffs have contributed to higher goods prices, the effects have generally been more concentrated and manageable than many initially feared. U.S. Bank estimates that tariffs have added roughly one-half of a percentage point to inflation since early 2025. While meaningful, that increase is considerably smaller than the broad inflation spiral many initially feared.3 In addition to pricing adjustments, businesses have responded through a combination of cost-control measures and supply chain changes, while evidence of broader spillovers into services inflation has remained limited.

“As time has progressed, the magnitude of tariff effects has become easier to quantify,” says Schoeppner. “That doesn't mean the costs have disappeared, but it does mean businesses, consumers, and policymakers have a better understanding of what they're dealing with.”

“This shift has changed the inflation debate,” adds Bovino. “Rather than asking whether tariffs are inflationary, economists are increasingly focused on whether the effects persist. And, in many respects, that is a far more manageable policy question.” Higher tariffs continue to place upward pressure on prices, but the inflation shock now appears more like a manageable headwind than the broad-based risk. U.S. Bank Economics views the recent CPI data as indicating that this one-time shock has nearly, if not, completely, been passed through with modest damage to the U.S. economy.

Growth proved more resilient than expected

While inflation concerns attracted significant attention, tariffs also raised questions about the broader economic outlook. Early on, economists worried that higher import costs would materially reduce purchasing power, pressure profit margins, weaken business confidence, and discourage investment. Under those conditions, many feared slower growth – or even a recession – could follow.

“Tariffs still represent a headwind to economic activity,” says Bovino. “Higher costs can affect both businesses and consumers, and they remain an important consideration in our outlook.” Yet despite those challenges, economic activity has generally remained on solid footing. Consumer spending has continued to support growth, labor-market conditions have remained relatively stable, and business investment has held up better than many expected. In addition, strong spending on artificial intelligence (AI)-related technologies has provided an important offset to other areas of weakness.

“The economy has not been immune to the effects of tariffs,” says Schoeppner. “But the adjustment process has proven smoother than some expected.” A more predictable policy backdrop, combined with supply chain adaptation and continued AI investment, has helped limit some of the downside risks that seemed more pronounced earlier in the cycle. Reflecting that shift, the U.S. Bank Economics Group has reduced its estimated probability of near-term recession from roughly 40% at the height of trade concerns last year to 25% today.4

This distinction matters. The tariff drag appears real, but also manageable. Those are two very different inferences. While higher tariffs continue to weigh on economic activity at the margin, the economy has shown a greater capacity to absorb those costs than many initially anticipated. As a result, tariffs increasingly look less like a catalyst for recession and more like a persistent, but manageable, headwind to growth.

Why the rest of the world faces a different calculation

While the U.S. economy has generally adapted well to higher tariffs, the experience has not necessarily been the same for every country. One reason is that trade plays a different role across economies.

“The United States is often less sensitive to trade disruptions than many other countries because trade represents a smaller share of overall economic activity,” says Schoeppner. While total U.S. trade (exports plus imports) amounts to roughly one-quarter of U.S. GDP, trade exposure is often considerably higher across many other developed and emerging economies.3

That distinction matters when trade policy becomes more restrictive. Economies such as Canada, Mexico, and many countries across Europe and Asia rely more heavily on exports and cross-border supply chains to support growth. As a result, changes in tariffs, trade agreements, or market access can have a larger effect on economic activity.

Bovino notes that the changing trade landscape has already produced different outcomes across regions. “Many of the adjustments taking place within global supply chains have altered the distribution of trade, creating both winners and losers.” Countries benefiting from near-shoring, supply chain diversification, and growing demand for technology- and semiconductor-related exports have generally been better positioned to capture investment and trade flows, while others have faced greater pressure from shifting sourcing decisions.

As a result, the impact of tariffs is increasingly being measured not only by their effect on overall trade volumes, but also by how they reshape the geography of global trade and growth. What has proven manageable for the U.S. may present a very different challenge for more trade-dependent economies.

What trade and tariff updates should businesses watch next?

If the first half of 2026 was defined by diminishing uncertainty surrounding tariff rates, future tariff updates may be shaped by a different set of questions. Increasingly, the focus is shifting away from how high tariffs might go and toward how trade policy is being used to advance broader economic and strategic priorities.

“Trade policy is becoming more closely intertwined with industrial policy, supply chain security, and national security considerations,” says Schoeppner. Industries tied to semiconductors, artificial intelligence, advanced manufacturing, energy infrastructure, and other strategic technologies are likely to receive heightened attention from policymakers in the years ahead.

Bovino adds that this shift is already influencing business investment decisions. “Supply chain resilience, access to critical components, and domestic production capacity have become more important alongside traditional considerations such as cost, efficiency, and market access.” In many cases, where products are made is becoming nearly as important as how efficiently they can be produced.

Importantly, uncertainty has not disappeared – it has evolved. Last year, businesses were focused primarily on tariff levels and the risk of escalation. Looking ahead, questions surrounding market access, supply chain security, technology leadership, and the future direction of trade agreements may become increasingly important.

“Growing investment in AI infrastructure, semiconductors, and advanced technologies is already influencing global trade and investment patterns,” says Schoeppner. “As those trends continue, businesses may find that competitiveness depends not only on tariff policy, but also on their ability to operate within emerging technology and supply chain ecosystems.”

Bottom line

The trade environment looks very different today than it did just six months ago. Tariffs remain materially higher than they were just a few years ago, continuing to create challenges for businesses operating across global supply chains. They also remain a source of upward pressure on prices and a modest headwind to economic growth.

At the same time, the adjustment process has generally proven smoother than many expected. Businesses adapted by diversifying supply chains, and the broader economy remained on solid footing. Rather than triggering a broad economic disruption, higher tariffs have initiated a reconfiguration of trade flows, investment decisions, and sourcing strategies.

Most importantly, uncertainty surrounding U.S. trade policy has begun to diminish. While questions remain about the direction of future policy, businesses, consumers, and financial markets now have greater visibility into the environment in which they are operating. That increased clarity does not eliminate the costs of tariffs, but it does make those costs easier to understand, plan for, and manage.

FAQ

Rather than reducing trade activity altogether, many businesses have adjusted by diversifying suppliers, shifting sourcing to alternative countries, and reevaluating supply chain strategies.

“One of the key developments has been adaptation,” says Beth Ann Bovino, chief economist at U.S. Bank. “Many firms adjusted procurement strategies, explored new supplier relationships, and found ways to manage higher costs.” These changes have helped limit some of the economic disruption that many economists initially feared.

Tariffs remain inflationary because they increase the cost of imported goods. However, the inflationary effects have generally been more manageable than many early announcements and estimates suggested. “Tariffs have contributed to higher prices,” says Bovino. “The more important question has been whether those effects become persistent and broadly embedded throughout the economy.” To date, tariff-related price increases have largely been concentrated in goods, while broader spillovers into other areas have remained relatively limited.

Reciprocal tariffs are tariffs imposed in response to another country’s tariffs or trade barriers. The goal is often to pressure trading partners to lower their own barriers or negotiate different trade terms. Reciprocal tariffs can also increase costs for importers and create uncertainty for businesses that rely on global supply chains.

While much of the recent tariff news has focused on tariff rates and trade negotiations, future attention may increasingly shift toward supply chain security, industrial policy, and strategic industries such as semiconductors, artificial intelligence, advanced manufacturing, and energy infrastructure. “We're seeing trade policy become more closely connected to economic competitiveness and national security considerations,” says Schoeppner. “As a result, businesses will likely continue monitoring not only tariff rates, but also how evolving trade and industrial policies influence investment decisions and global supply chains.”

Tags:

U.S. Bank Economics Research Group

Beth Ann Bovino

Chief Economist

Ana Luisa Araujo

Senior Economist

Matt Schoeppner

Senior Economist

Adam Check

Economist

Andrea Sorensen

Economist

Subscribe to our economic insights newsletter

Not currently a subscriber? Sign up to get our economic insights delivered to your inbox weekly.

Learn more

If you have any questions about any of these topics or want to learn more, please contact us to connect with a U.S. Bank Corporate and Commercial banking expert.

Start of disclosure content

Disclosures

Start of disclosure content