Capitalize on today’s evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

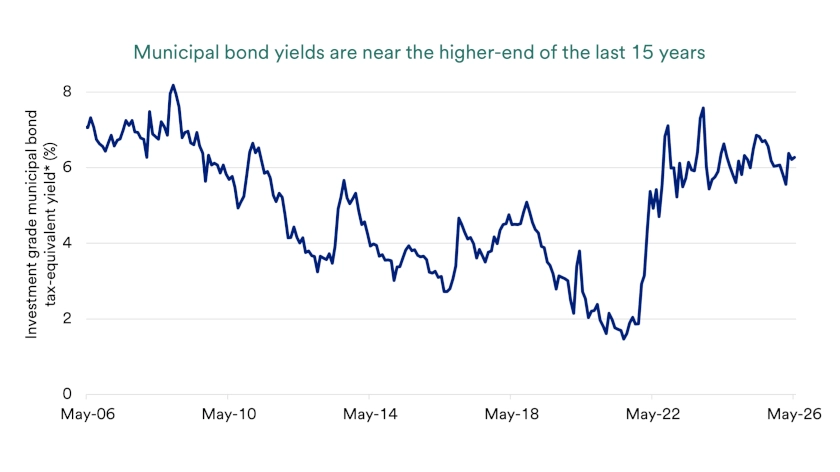

The municipal bond market offers tax-sensitive investors attractive income potential, with tax-equivalent yields near historically elevated levels.

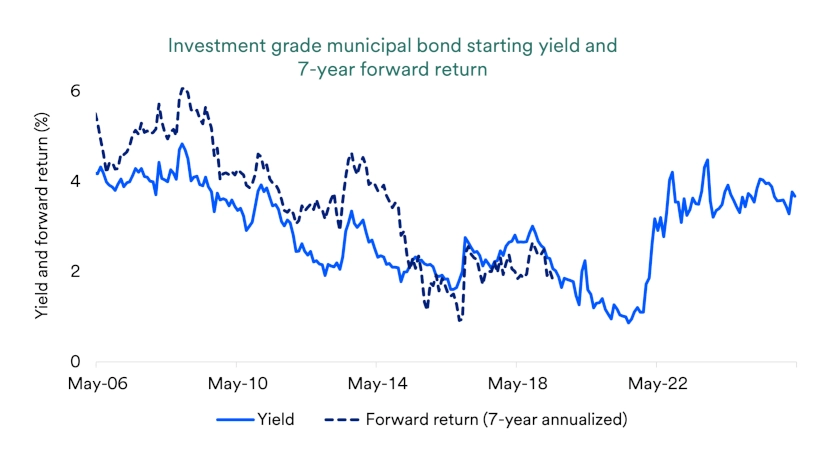

Bonds and interest rates remain closely connected; higher starting yields can support forward returns even as interest rates and bond prices fluctuate.

The bond market outlook favors diversified municipal bond exposure for high-tax households evaluating whether bonds are a good investment right now.

Municipal bonds currently offer tax-sensitive investors notable return potential with tax-equivalent yields near the upper end of the last 20 years. High-income investors in states with high state income tax rates may further benefit from state and federal tax exemptions for certain municipal bonds. Current opportunities in municipal bonds hinge on three key factors: favorable yields, meaningful tax-exemptions and solid issuer fundamentals.

Bond yields play a foundational role in determining future bond returns. This is especially true for bonds with investment grade credit ratings, since defaults tend to be low. Buy-and-hold investors can expect returns to closely track starting yields over time, despite yield fluctuations that can temporarily cause swings in bond prices.

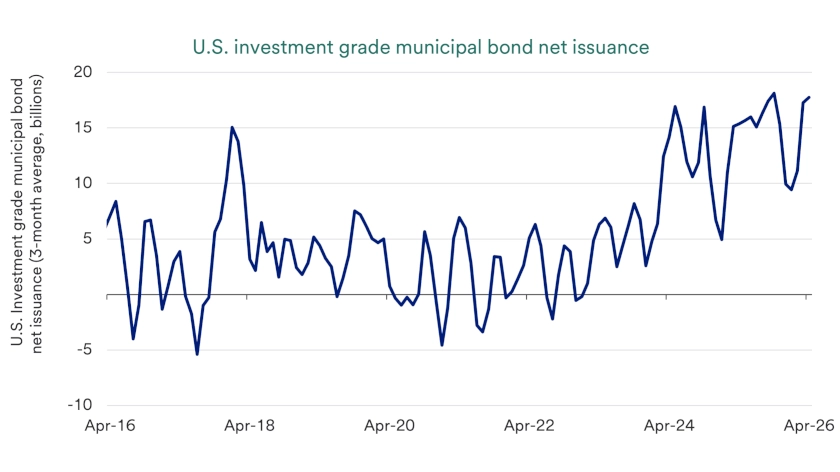

Two factors currently contribute to elevated municipal bond yields. First, elevated Treasury yields establish income opportunities across many parts of the bond market. Second, high municipal bond issuance improved yield opportunities. Municipal bond issuers borrowed a record amount in 2025, and municipal bond issuance is tracking even higher so far in 2026. This supply headwind creates opportunities for investors to purchase bonds at favorable yields and cheaper valuations than many other parts of the market.

“Currently, investment grade municipals offer approximately 1.9% more yield than Treasury bonds on a tax-equivalent basis, which can meaningfully boost potential returns.”

Bill Merz, head of capital market research for U.S. Bank Asset Management Group

Measuring municipal bond yields in tax-equivalent terms allows investors to compare income opportunities in municipal bonds to other bonds that do not receive a tax benefit. “Currently, investment grade municipals offer approximately 1.9% more yield than Treasury bonds on a tax-equivalent basis, which can meaningfully boost potential returns,” says Bill Merz, head of capital market research for U.S. Bank Asset Management Group. This assumes an investor is in the top federal income tax bracket. Municipal bond tax-equivalent yields relative to Treasuries create attractive income potential versus other assets like corporate bonds that have somewhat elevated valuations.

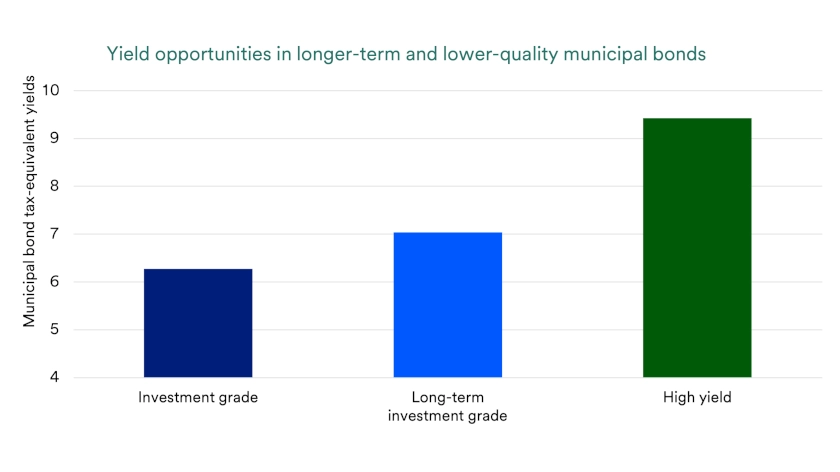

Municipal bonds’ tax-exemption magnifies the benefit of generating extra income through allocations to longer-term and lower-quality bonds. Over the last five years, high yield municipal bond yields have exceeded investment grade municipal bonds by 3.45% on average. Similarly, longer-term municipal bond yields yielded 0.7% more on average. Accordingly, maintaining a slight bias towards longer-term and lower-quality municipal bonds tends to improve return opportunities. However, primarily allocating to core investment grade municipal bonds remains important since longer-term and lower-quality municipal bonds have additional risks. Longer-term municipal bond prices tend to be sensitive to yield changes, since investors lock in income for many years, and investor sentiment shifts can cause changes in high yield municipal bond prices.

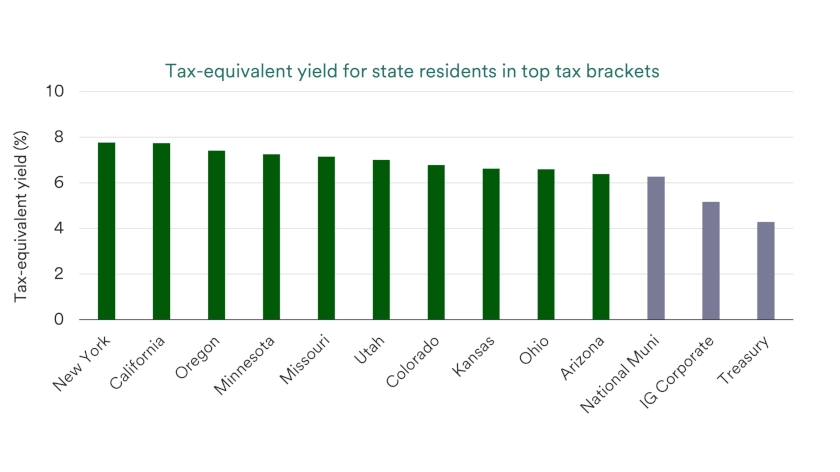

Investors in high tax states may have even better opportunities in municipals. For example, residents of California who own California municipal bonds may be exempt from the 13.3% state-level income tax rate on municipal bond income, in addition to federal income taxes. This double exemption enhances the tax-equivalent yield advantage for residents of certain states.

Municipal bond credit fundamentals remain sound based on credit rating agency actions and state-level finances. Both provide reassurance that well-diversified high quality municipal bond portfolios supported by active credit research and monitoring should exhibit low credit losses in the future, consistent with historical precedent. Active credit research involves specialists reviewing individual bonds to identify favorable investment opportunities.

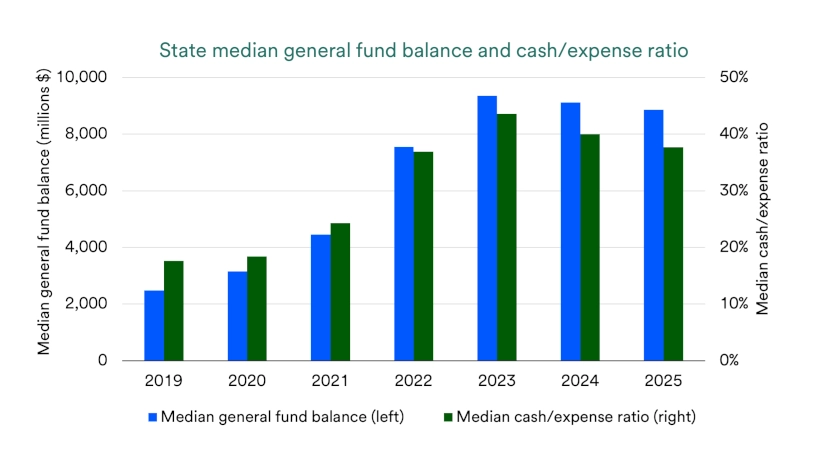

State level general fund balances, which reflect differences between state revenues and expenditures, increased nearly fourfold between 2019 and 2025, on average. Median state cash balances relative to expenses doubled over the same period. Excess cash also contributed to steady growth in rainy day funds among the states. Rainy day funds refer to surplus revenue that has been set aside for budget deficits and unexpected financial needs. Since 2010, the median state rainy day fund rose from six days’ worth of typical expenditures to 47 days’ worth of expenditures in 2025.

Credit rating agencies, like Moody’s, review thousands of municipal bonds. Rating changes over time indicate a trend of more upgrades relative to downgrades, referred to as ratings drift. According to Merz, “Municipal ratings drift has been improving since the Covid pandemic and reflects improving financial positions for many municipal bond issuers.” Municipal bond ratings are also generally more stable than for corporate bonds which are more sensitive to economic cycles.

“Compelling yields, reasonable valuations, potential tax benefits and strong credit fundamentals translate to municipal bond opportunities for tax-sensitive investors in current markets,” notes Merz.

Talk with your wealth professional for more information about how to position your fixed income investments as part of a diversified portfolio.

A municipal bond is typically a state, city, or county-issued debt security. Government entities issue such bonds to finance major capital projects, such as roads, schools, or public buildings. As is the case with other types of bonds, investors effectively lend money to the municipal bond issuer in exchange for a promise of regular, timely interest payments. Unlike most other bonds, the interest investors earn on municipal bonds is generally exempt from federal income tax. When the municipal bond matures, the issuer repays the principal. Investors can purchase municipal bonds when they are initially issued or buy them on the secondary market.

Municipal bonds function similarly to other types of bonds, with the issuer making regular and timely interest payments to investors. At the municipal bond’s maturity, investors receive back their original investment, or principal. Unlike most other bonds, municipal bond interest is generally exempt from federal taxation. Therefore, municipal bond issuers typically offer lower nominal yields than similar bonds issued by the federal government or other entities. Accounting for the bonds’ tax-exempt status, investors need to assess a municipal bond’s tax-equivalent yield. For an investor in the 24% federal tax bracket, a municipal bond offering a 3% nominal yield exempt from federal income tax would generate income equivalent to the after-tax income of a U.S. government bond yielding 3.95%.

Risk-averse investors, particularly those seeking to generate an income stream, may opt for municipal bonds over other risk assets. Like any fixed-income security, municipal bonds are subject to interest rate risk. In periods when interest rates rise, the market value of a municipal bond may dip below its par value (the initial investment made). Inflation is another risk. During periods of higher inflation, the stable income generated by a municipal bond will result in less purchasing power. It’s also essential to assess an issuer’s credit risk. Credit rating agencies measure the creditworthiness of state and local government entities. This helps assess the likelihood of receiving timely interest payments and a return of principal upon the bond’s maturity.

The S&P 500’s recent rollercoaster performance has investors wondering what lies ahead for the stock market.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.