What if one chat could change how you feel about money?

Meet with a financial advisor to get insights and next steps for your money.

Inflation is the average increase in the cost of goods and services over time. As the cost of goods rises, your money buys less. This also impacts your savings and the real return on your investments.

While cash and fixed income investments often decrease in value during high inflation, real assets like commodities and real estate tend to hold their value.

Diversification across asset classes and focusing on real returns may help you build a more resilient portfolio.

Most people understand that inflation increases the price of their groceries and decreases the value of the dollar in their wallet. In reality, though, inflation affects all areas of the economy, and over time, it can even take a bite out of your investment returns.

Understanding the relationship between inflation and your investments is essential to making informed investing decisions. Here’s a high-level look at the effects of inflation on investments and, specifically, how inflation affects stocks. For a deeper dive, read analysis on inflation’s current impact on investments.

Inflation is the average increase of cost of goods and services over time. As prices rise, your purchasing power decreases. In other words, with inflation, your money “buys less” over time.

Inflation can be calculated broadly as the overall increase in the cost of living or for specific categories, such as the cost of gas, groceries or housing.

Inflation is an economic reality that influences every aspect of your financial life, from the cost of your morning coffee to the long-term value of your retirement portfolio.

Inflation shrinks your savings even when they’re in accounts generating an average interest rate, which makes factoring it into your retirement planning particularly important.

When you’re working, your earnings should theoretically keep pace with inflation. When you’re living off your savings, inflation diminishes your buying power.

For example, if you need $50,000 per year to sustain your current lifestyle, and the annual inflation rate is 3%, in 30 years you’ll need roughly $121,000 per year to have that same buying power. 1

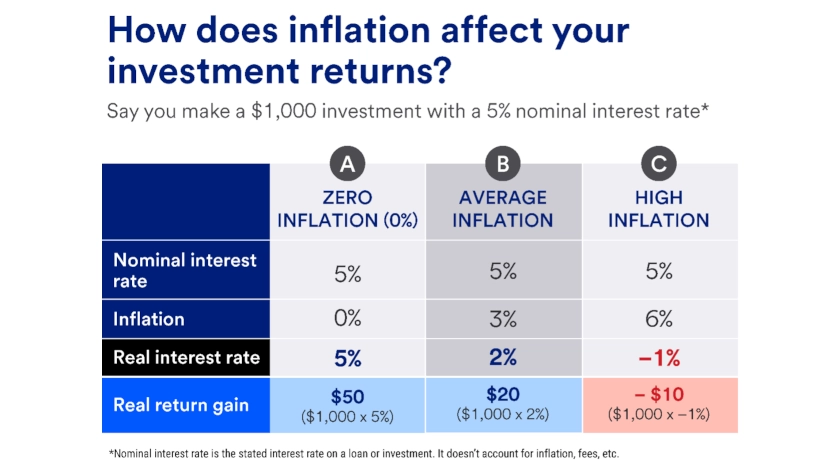

To understand how inflation can eat away at your investment returns, it’s important to differentiate between nominal and real interest rates.

Investors earn a real return only when the nominal rate outpaces inflation. This means investments with lower interest rates are hit harder by the effects of inflation.

Cash and cash equivalents are often hit the hardest. When there’s little to no interest being generated to compete with the rate of inflation, it can quickly eat into the purchasing power of your cash.

Inflation can significantly reduce real returns on fixed income investments such as corporate or municipal bonds, treasuries and certificates of deposit (CDs).

Typically, investors buy fixed income securities because they want a stable income stream in the form of interest payments. However, since the income stream remains the same on most fixed income securities until maturity, the purchasing power of the interest payments declines as inflation rises. As a result, bond prices tend to fall when inflation is increasing.

Consider a one-year bond with a $1,000 face value and a 5% coupon.

Accelerating inflation is even more detrimental to longer-term bonds, given the cumulative impact of lower purchasing power for cash flows received far in the future.

Inflation has a more moderate or even positive impact on other asset types, such as stocks and real assets.

Companies often raise prices to account for higher costs, which can help their stock price rise along with general consumer prices. However, as with bonds, high inflation can negatively affect a stock’s nominal returns. For example, assume you have a return of 5% in your stock portfolio. If inflation is at 6%, the real return is negative (–1%).

Real assets, such as commodities and real estate, tend to have a positive relationship with inflation. Energy-related commodities like oil have a particularly strong relationship with inflation, and industrial and precious metals also tend to rise when inflation is accelerating.

When it comes to real estate, property owners often increase rent payments in line with the Consumer Price Index, which can flow through to profits and investor distributions.

Inflation might be beyond your control, but that doesn’t mean you can’t take action to help preserve your investments and savings from its effects.

Diversification is one strategy you can use to help build a resilient portfolio. Spreading your investments across different asset classes, industries and geographic locations can help manage inflation risk. By owning different types of investments that react differently to economic environments, you can position your portfolio to be more resilient during challenging market periods.

It’s also important to focus on your real rate of return rather than just the nominal rate. This mindset shift ensures you are always evaluating your wealth in terms of purchasing power rather than just the dollar figure on your statement.

Inflation is an economic reality that influences every aspect of your financial life, from the cost of your morning coffee to the long-term value of your retirement portfolio. While it presents challenges for your investments, understanding the mechanics of nominal versus real returns can empower you to make smarter decisions.

As you monitor the economic landscape, focus on the variables you can control: your savings rate, your diversification strategy, and your long-term plan.

Consulting with a financial professional can help you tailor these strategies to your unique circumstances, ensuring that the steps you take are most appropriate for your situation and long-term goals.

From investing online to working with a financial professional, learn more about your investing options.

Interest rates influence the cost of borrowing money and the reward for saving it. Understand how rate changes can affect your loans, savings and investment portfolio.

Let us help you craft a portfolio that reflects your goals, time-horizon and values.