Financial guidance and support, tailored for you.

Explore the benefits of working with a dedicated wealth team.

The kiddie tax applies to a child’s unearned income, which includes interest, dividends and capital gains.

The 2026 kiddie tax allows the first $1,350 to be tax-free, taxes the next $1,350 at the child’s marginal rate, and applies the parent’s marginal rate to the rest.

It’s smart to speak with a tax advisor to see if you can gift assets to children or grandchildren in a more tax-advantaged way.

Using custodial accounts (such as a child’s savings or investment account) to gift assets to children and grandchildren is one way to potentially reduce your income taxes. This strategy allows you to shift income into the child’s lower tax bracket while also removing assets from your taxable estate.

However, the tax benefits of this strategy are limited due to what’s commonly referred to as the “kiddie tax.”

The kiddie tax is a tax on a child’s unearned income, such as interest, dividends and capital gains. It’s not a separate tax, but instead, a specific tax rule established to prevent families from using custodial accounts as a tax shelter.

According to Dan Willing, Senior Wealth Strategist with U.S. Bank Private Wealth Management, the laws creating the kiddie tax were enacted as part of the 1986 Tax Reform Act to curtail income-shifting strategies like this.

“Under the kiddie tax rules, children’s unearned income above a certain threshold is taxed at the parent’s marginal tax rate,” says Willing. Marginal tax rates currently range from 10% to 37% depending on your income.

The legislation defines a child as anyone who is under age 18 or a full-time student who is under age 24. For kiddie tax purposes, unearned income includes:

“There are usually better ways to accomplish tax saving goals than by outright gifting assets to children.”

Dan Willing, Senior Wealth Strategist, U.S. Bank Private Wealth Management

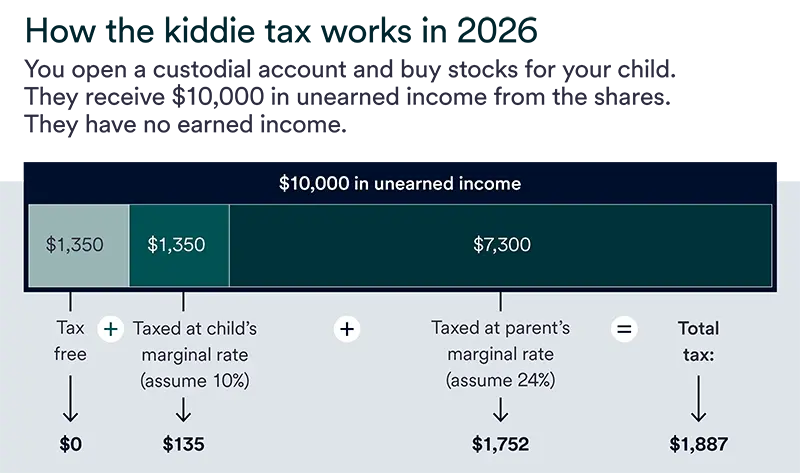

The 2026 kiddie tax threshold allows the first $1,350 of a child's unearned income to be tax-free. The next $1,350 is taxed at the child's marginal tax rate, which is generally 10% if the child’s taxable income is within the lowest tax bracket. Anything over $2,700 is taxed at the parent's marginal tax rate.

If you’re considering gifting assets to your children or grandchildren, it’s important to understand when the kiddie tax rule kicks in. Willing says that there are a few exceptions to these rules. The kiddie tax does not apply if a child:

Support includes food, clothing, shelter, healthcare and tuition, while earned income includes wages, salaries, tips and other compensation for personal services.

If a child has earned income, such as from a summer job, the rules get more complex. “In this case, it’s usually smart to consult a tax advisor for guidance,” Willing says.

The kiddie tax reduces the tax benefits of gifting assets by applying higher parent tax rates to a child's investment earnings.

Suppose you opened a custodial account and purchased stock shares for your child, and they received $10,000 in dividends, interest and capital gains from the shares (unearned income). They have no earned income to report.

All in, the tax on your child’s $10,000 of unearned income would come to $1,887.

You can report the kiddie tax in one of two ways:

If the child’s unearned income is greater than $2,700 in 2025 and 2026, they can file their own tax return using Form 1040 and attach IRS Form 8615, “Tax for Certain Children Who Have Unearned Income.” The form will calculate how much tax is due using the parent’s marginal tax rate for income above the $2,700 threshold.

If the child’s gross income (their income before taxes and deductions) is less than $13,500 in 2025 and 2026, this income can be included on the parent’s tax return using IRS Form 8814, “Parents’ Election to Report Child’s Interest and Dividends.” While this may simplify the tax-filing process, it could increase the parents’ taxable income.

Willing says the best way to avoid paying the kiddie tax in 2026 is to avoid generating income that’s subject to the tax. “There are usually better ways to accomplish tax saving goals than by outright gifting assets to children,” he says.

One option is to invest in a tax-advantaged account like a 529 college savings plan or help your child with earned income contribute to a Roth IRA, so earnings grow tax-free or are subject to more favorable tax treatment.

Another is to prioritize investments that generate minimal taxable income, such as tax-free municipal bonds or growth stocks that focus on capital appreciation instead of paying dividends.

While custodial accounts are simple to open, they permanently transfer control to the child at the age of majority, which may not align with your long-term planning goals. Willing prefers irrevocable trusts to custodial accounts for purposes of generational wealth transfer. “These can be set up in ways that are tax-efficient and allow more control over when distributions occur,” he says. “They provide much more significant guardrails than custodial accounts.”

The kiddie tax no longer applies once a child turns 18, unless they are a full-time student. For full-time students, the rules stop applying when they reach age 24.

Yes, distributions from an inherited IRA are generally considered unearned income. If the distributions exceed the annual threshold, they are subject to the kiddie tax.

No, the kiddie tax only applies to unearned income like dividends, interest and capital gains. Wages from a part-time job or summer employment do not trigger this tax.

Yes, taxable scholarships and fellowship grants count as unearned income under the kiddie tax rules. Tax-free scholarships used for tuition and required fees do not count.

The details of gifting as a strategy to reduce income taxes can get complex when the kiddie tax is factored in. You should speak with your tax and financial professional for guidance in your specific situation.

Learn how we can help you design a plan to grow and protect your wealth.

Did you know you can open a Roth IRA for your kids if they’re earning an income? Learn more about eligibility, contribution limits, tax implications and withdrawal rules for this custodial investment account.

A thoughtful approach to taxes and their impact can help keep your financial plan on track.