Start investing today with U.S. Bancorp Advisors.

Investment products and services are: Not a deposit | Not FDIC insured | May lose value

Giving your child a strong foundation in investing concepts will help them grow into financially confident adults.

Introduce your kids to compound interest and encourage them to start young and contribute regularly to take advantage of long-term growth.

You can help your child start investing by opening an investment account tailored to their needs and work with them to set investment goals.

Teaching your children about money is like giving them a superpower. While many parents start with a piggy bank or a savings account, it’s important to take this education to the next level as your kids get older.

Introducing them to the world of investing when they’re in their tweens and teens—both key principles and how to invest—is an important step toward their eventual financial independence.

Understanding how and why to invest is a key part of financial literacy, extending beyond just earning and saving money. It introduces concepts like goal setting, patience, and discipline, all while offering your child the potential to grow their money.

Whether they’re saving for college, buying their first car, or have dreams of starting a business, the earlier you have the conversation, the more time they have to invest and work toward their financial goals.

Investing introduces concepts like goal setting, patience, and discipline, all while offering your child the potential to grow their money.

Compound interest makes money grow exponentially over time by reinvesting earnings. A quick and fun way to demonstrate the power of compounding — especially to younger children — is to ask if they’d rather have a $100 bill today or a penny that doubles every day for 30 days. They might be surprised to hear that in 30 days, that penny would be worth about $5.4 million. 1

Unfortunately, there’s no such thing as a penny that doubles each day, but this example can help them begin to understand that through investing, they can use their money to grow more money.

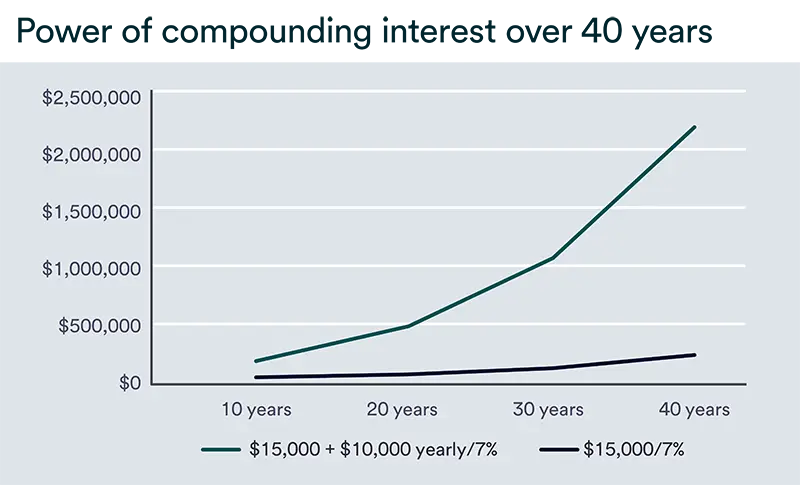

Investing wisely takes discipline and patience. The graph below illustrates this lesson in two scenarios.

Investing is about working toward long-term goals, not funding short-term needs and desires. For example:

That said, it’s important to talk about risk and its relationship to reward. Money in a savings account has little to no risk, but it also delivers small returns. Investing in stocks or mutual funds might provide higher returns, but it comes with higher risks as markets can fluctuate. By helping them understand these trade-offs, you’ll prepare them to make smarter financial decisions.

Once your child understands the basic investing principles, show them how it works in real life

Choose an account that aligns with their goals and your family’s situation. Here are some options to consider:

After you’ve opened your child’s account, the next question is how to fund it. Many parents start with a small gift to their child’s account.

Then, help your child fund their account with a portion of their allowance, earnings, or gifts. Teach them to divide their income into four categories: spending, saving, sharing and investing. For example, if they earn $100 a month, they might spend $30, save $20, share $20 and invest $30. This exercise can help them see how budgeting, saving, and investing all work together.

Once your child knows how much they’ll have to invest, it’s time to decide how to invest.

One approach is to allow them individual shares in companies they know and like. Kids can relate to owning shares in companies they recognize, like their favorite sneaker or game brands. Explain how these companies sell their products, they’re creating profits for their shareholders—and now your child is one of them.

Alternatively, teach them how to build a diversified portfolio. While this may not be as exciting as owning individual shares, it can certainly be less volatile. For example, exchange-traded funds (ETFs) allow them to invest in a wide range of companies with just one purchase. A popular starting point could be an ETF that tracks the S&P 500, giving them exposure to 500 of the largest companies in the U.S. Note that not all investment accounts will allow you to select individual investments.

By combining fun, familiar examples with sound financial education, you can help your child feel confident and empowered about managing their money.

Yes, a parent or guardian can open an investment account for their child and manage it until the child reaches the age of majority, which varies by state. Options include a Trump account, custodial accounts, Roth IRAs for kids, and education-specific accounts like a 529 plan.

The minimum age to open a brokerage account is 18. However, a parent can open an account on their child’s behalf and manage it until the child reaches the age of majority.

The best investment account for your child depends on their goals and how the money is likely to be used.

For education-focused goals, a 529 plan may make sense. For children with earned income, a custodial Roth IRA can offer tax-free growth and flexibility later in life. For families focused on opening a retirement account as early as possible, a Trump account may be worth considering, as it’s designed to keep money invested until adulthood.

Support your child’s financial independence by teaching smart investing habits. Learn how we can help you start investing today.

Talking to your kids about money may not always be easy, but it’s important to their future financial wellbeing. Here are tips for how to teach kids about money at every age.

Explore the benefits of personalized wealth services.