Higher rates, shifting expectations

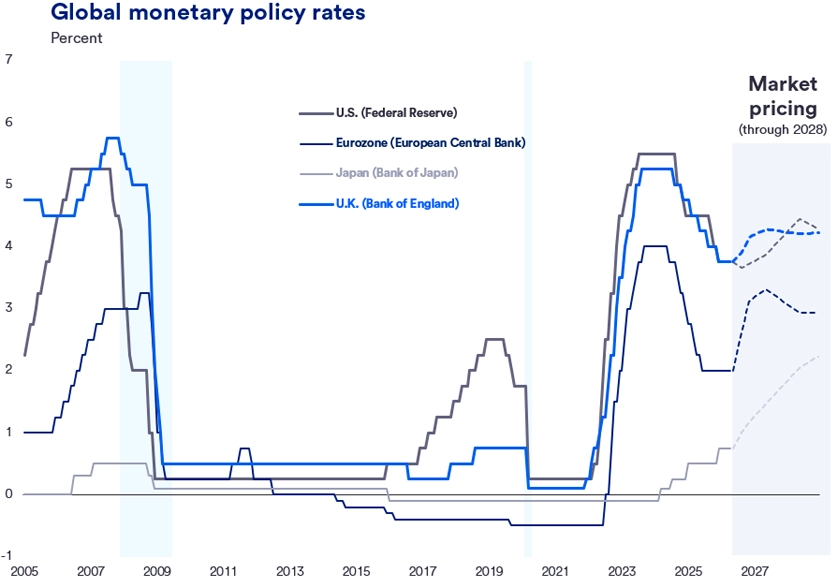

Bond markets have responded to this evolving backdrop. Treasury yields have moved higher across the curve in recent months, with the 2-year and 10-year yields recently surpassing 4.10% and 4.65%, respectively – both at +15-month highs – reflecting firm inflation data and a reassessment of the policy outlook. Not long ago, markets were anticipating additional rate cuts in 2026. Today, however, expectations have shifted meaningfully, with investors now pushing out the timing of easing – and in some cases, even considering the possibility that the next move could be a rate hike.

“This repricing reflects a broader shift in how policy risks are viewed,” says Schoeppner. “Rather than focusing primarily on when rate cuts will resume, markets are now weighing a wider range of potential outcomes.” The result is a more volatile interest rate environment, with greater sensitivity to incoming economic data and geopolitical developments.

A resilient U.S. economy complicates the outlook

Part of what makes the Fed’s job more challenging is the underlying strength of the U.S. economy. Despite higher borrowing costs, growth has remained relatively stable. Consumer spending, business investment, and broader activity indicators suggest the economy continues to expand near its 2% to 2.5% trend in the first half of 2026, even if the pace is uneven. The labor market tells a similar story. At a headline level, conditions appear solid, with steady job gains averaging ~50,000 per month in early 2026 and an unemployment rate holding in the low 4% range. That said, beneath the surface, there are signs of gradual cooling. Hiring activity has slowed, and labor force participation dynamics suggest that demand for workers may be easing.

Importantly, this adjustment is happening without a meaningful increase in layoffs. Rather than a sharp downturn, the labor market is rebalancing more gradually – described as a “low-hire, low-fire” environment. “This type of adjustment tends to reduce inflation pressure over time,” Bovino adds, “but it does not typically create the kind of economic weakness that would prompt immediate rate cuts.”

A delicate policy balance

Taken together, these dynamics are shaping a more asymmetric policy outlook. Growth and employment remain strong enough to support the economy, removing the urgency for the Fed to cut rates. At the same time, inflation remains elevated enough to limit policymakers’ ability to ease.

“This leaves the Fed focused on flexibility,” says Schoeppner. “Policy communication has emphasized data dependence and caution, with officials intentionally avoiding firm guidance on the future path of rates.” In practical terms, that means the Fed is likely to remain on hold until there is clearer evidence that inflation is moving sustainably back toward target.

For now, the most likely scenario is that the Fed maintains its current policy stance through much of 2026. But with uncertainty still high, the range of possible outcomes remains wide – including the possibility that rates could move higher next year if inflation pressures prove more persistent than expected.

“This backdrop may also pose challenges for incoming Fed Chair Kevin Warsh,” adds Bovino, “whose stated preference for a more proactive easing stance could be difficult to implement in an environment where inflation risks remain elevated and the policy bar for rate cuts has moved higher.”

Global central banks: navigating a shared shock

While the Federal Reserve plays a central role, it is far from alone in navigating this environment. Central banks around the world are confronting many of the same challenges – most notably the impact of an energy shock on both inflation and growth, and the uncertainty surrounding how long those pressures may persist.

In Europe, for example, the ECB faces a sharp tradeoff. As a net energy importer, the euro area is more exposed to higher energy costs, which tend to feed more directly into inflation. “As a result, the ECB has shown a continued bias toward guarding against inflation risks, even as economic growth remains soft,” says Schoeppner. Policymakers are increasingly focused on preventing higher prices from becoming entrenched, which has kept the possibility of further rate increases on the table.

The Bank of England faces a similar balancing act but appears more explicitly divided between growth and inflation concerns. While inflation remains a key issue, the economic backdrop has shown signs of softening, leading policymakers to proceed cautiously. Still, both have learned from the 1970s, and have reduced energy dependence which will give them some relief today.

Japan stands apart from other major economies. After years of exceptionally low interest rates, the BOJ is gradually moving toward policy normalization. “Inflation has proven more durable, and increasingly domestically driven,” says Bovino, “allowing the BoJ to take steps toward higher rates.” That said, policymakers remain mindful of global risks and are moving carefully to avoid undermining economic momentum.