Financial guidance and support, tailored for you.

Explore the benefits of personalized wealth services.

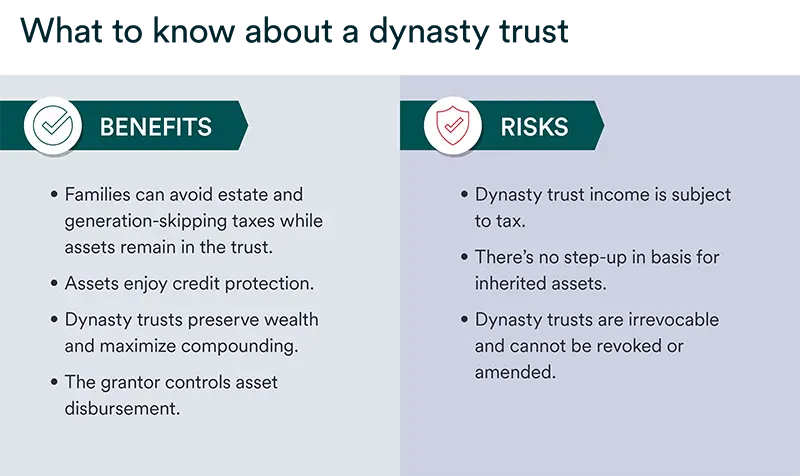

High net worth families can use dynasty trusts to enable long-term wealth growth for generations to come, because they don’t incur estate taxes or generation-skipping transfer taxes.

Dynasty trusts are irrevocable, meaning that the grantor cannot revoke or amend the trust once assets are placed in it.

Consider establishing a dynasty trust in a state with favorable tax and asset-protection laws.

For families with significant wealth, an important part of legacy planning is ensuring an effective and tax-efficient transfer of wealth to children, grandchildren and subsequent generations.

Trusts are a primary vehicle for transferring wealth, but not all types of trusts last for as long as you might prefer them to. A dynasty trust, which can last for multiple generations and provide key tax benefits, is often an appealing option.

A dynasty trust, sometimes called a legacy trust, is a type of irrevocable trust that facilitates the transfer of wealth to future generations while minimizing taxes. These trusts have traditionally been used by high net worth individuals and families to pass wealth to future generations without incurring estate taxes or generation-skipping transfer (GST) taxes.

“Dynasty trusts can be an effective tool for high net worth families to transfer assets to succeeding generations in the most tax-efficient manner,” says Justin Flach, managing director of wealth strategy for Ascent Private Capital Management of U.S. Bank.

Dynasty trusts enable long-term wealth growth for multiple generations that’s undiminished by estate and gift taxes, potentially resulting in decades of compounding returns for future beneficiaries.

“By placing assets in a dynasty trust, families can avoid estate and GST taxes as long as the assets remain in the trust,” says Flach. “This can be a huge long-term benefit.”

Justin Flach, managing director of wealth strategy, Ascent Private Capital Management of U.S. Bank

One note: A dynasty trust is similar to a bloodline trust but with one key difference: A bloodline trust restricts beneficial interest in the trust to those who are blood relatives of the grantor. “In other words, it excludes spouses, partners and stepchildren,” says Flach.

As with any financial vehicle, dynasty trusts offer upsides and downsides. It’s important to consider this type of irrevocable trust in the context of your overall legacy plan and tax strategy.

The laws governing dynasty trusts vary from state to state, with some states prohibiting them outright and others limiting the number of years a trust can operate.

“You want to establish a dynasty trust in a state that allows trusts to exist in perpetuity or for a very long time,” says Flach. “Also, choose a state with strong asset protection laws and one that does not levy state income tax on trust assets.”

Several states are commonly recognized as the best states for establishing a trust situs, including South Dakota, Nevada and Delaware. You don’t have to live in one of these states to establish a dynasty trust situs there, but you do need an in-state trustee. This trustee can be a financial institution with an office in your chosen state and that can meet the legal requirements for trusts sitused in that state.

A dynasty trust cannot be easily changed if circumstances or needs change, which stands in contrast to a revocable trust, such as a living trust, which can be changed or revoked. Therefore, when comparing a dynasty trust vs living trusts or other options, you need to be reasonably sure that you won’t need access to assets held in a dynasty trust during your lifetime.

Flach also notes that dynasty trusts usually aren’t created unless there’s a significant amount of wealth involved.

Some families are concerned about the potential impact on future beneficiaries of decisions they make while establishing a dynasty trust. However, you can structure a trust to specify that beneficiaries meet desired incentives or achieve certain goals before assets are distributed, such as graduating from college or building a career.

A dynasty trust is just one of many tools that high net worth families can use to accomplish their estate planning goals. “Families should carefully evaluate the pros and cons of a dynasty trust in light of their goals and circumstances to determine if it’s the right tool for them,” says Flach.

Learn more about trust and estate services from U.S. Bank.

High net worth families have a vested interest in maintaining generational wealth. Here are five estate planning strategies to explore.

Explore the benefits of personalized wealth services.