How to choose the right savings account for your goals

5 money-saving tips to boost your savings

6-min. read

The APY (annual percentage yield) shows how much your money earns over a year — when compound interest is included.

A higher APY helps your savings grow faster.

The more frequently interest compounds, the more you earn.

Comparing APYs across accounts can help you find the best home for your money.

Annual percentage yield might sound like bank speak, but it really just means that your money earns money. Here’s what it means, how it works and why it matters.

First things first: Annual percentage yield (APY) is not the same thing as an interest rate. It’s actually the real MVP of your savings account. A higher APY can help you reach your goals faster — whether that’s saving for your next tropical vacation, building your emergency fund or putting a down payment on a car.

If growing your money sounds like something you can get behind, this article is for you. Let’s break it down.

APY is the total amount of interest you earn over the course of a year on the money you have saved. It is not the same as the interest rate on the account. Rather, it’s the yield as you earn interest on your interest — and your money compounds over the course of the year.

TL;DR: Think of APY as your money’s side hustle. It keeps working, even when you’re not.

An interest rate is what your bank offers as an incentive to keep your money in one of its accounts. Rates change all the time based on the type of account and broader economic factors.

APY is how that works in real life. It’s what you actually earn after compounding interest. And what is compounding? It’s the interest you earn on interest. Every time your balance grows thanks to interest (which could be weekly, monthly or over another time period), your next interest payment is calculated on that higher amount. That’s how your savings build momentum.

TL;DR: Interest rate = the promise. APY = the paycheck.

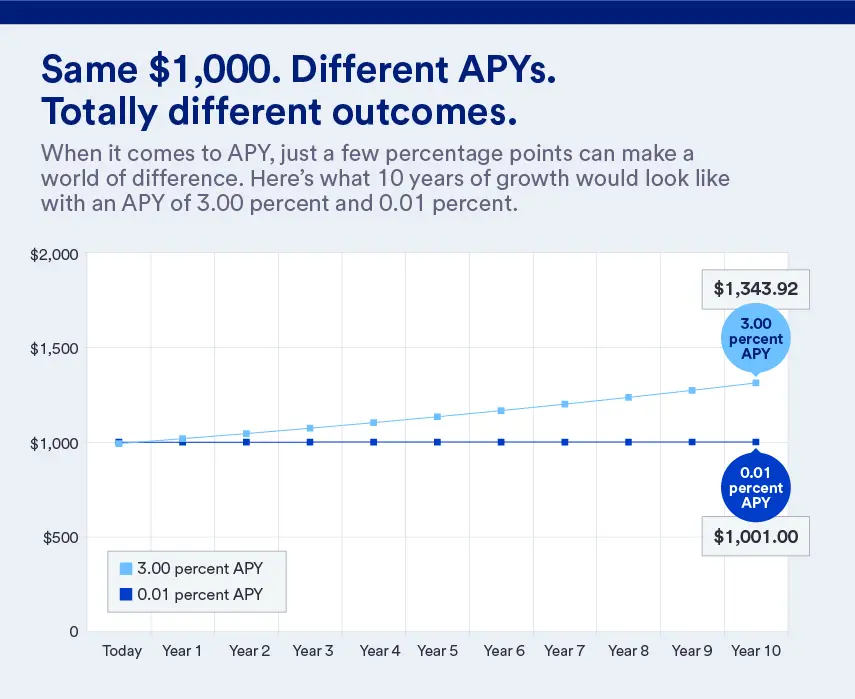

Say you have $1,000 in an account that offers you an interest rate of 3.00 percent annually. If you have an account that compounds monthly, it will pay you one-twelfth of that interest rate, or 0.25 percent of your balance every month.

At the end of the year, you’ll have $1,030.42 in your account — so you earned $30.42 in interest. That means your APY, your actual rate of return, was slightly higher (3.0416 percent) than your 3.00 percent rate.

Each successive month, you earn interest on the new, slightly larger amount of money in your account. The 3.00 percent rate used here is just an example — real interest rates on savings accounts can vary and may change over time, which affects how much you earn. But in this illustration, the balance that’s earning it gets a little bigger each month.

This might not seem like a big jump, but it adds up, especially as your money continues to compound over time. The more often interest compounds (daily > monthly > annually), the faster your savings grow.

TL;DR: The higher the APY, the faster your money grows.

You don’t get one big APY payout at the end of the year. Instead, the interest that makes up your APY is usually paid out in smaller chunks, typically monthly or quarterly, depending on your account. Each time interest is paid, it’s added to your balance, and that new total becomes the starting point for the next compounding period.

So while your APY is calculated as an annual figure, you’ll actually see the results show up as regular “interest earned” deposits throughout the year — little boosts that keep your balance growing.

If you want to run the numbers yourself, you’ll need to know your interest rate and how often the account compounds. Or skip the math and use a trusted calculator, like the one from the U.S. Securities and Exchange Commission.

TL;DR: APY is measured yearly, but the money lands in your account periodically. Think of it as a steady stream of mini paydays for your savings.

Because it reflects compounding, APY is the best measure for how your money grows. Building an emergency fund? A higher APY helps it grow faster, even if you never add another dollar. Saving for a trip? Think of APY as your travel fund’s secret upgrade — it keeps working in the background while you plan.

Whether you have a clearly defined goal or are just trying to stash away a few dollars for a rainy day, a higher APY helps your money move in the right direction.

TL;DR: A higher APY means your money reaches your goals before you do.

Earn competitive interest with a U.S. Bank Smartly® Savings account.

When choosing an account, compare APYs across savings, CDs and money market options. The U.S. Bank Smartly® Savings account, for example, offers competitive APYs depending on your balance and other factors. The Elite Money Market account offers attractive APYs if you meet certain balance requirements.

The account you choose should depend on how much money you are saving and how long you want to save it for. If you’re not going to touch your money for a specific time period (say 9 or 13 months), consider a CD with a fixed APY. Just make sure the account clearly lists its APY to help you visualize how your balance can grow.

TL;DR: Don’t chase hype — chase growth.

Because the interest rate tells you what’s promised, but the APY shows what you’ll actually earn once compounding kicks in. APY is the truer reflection of your total return.

Some banks boost APYs for higher balances or linked accounts. You can also open a high-yield savings or money market account, or consider CDs with longer terms for a fixed, often higher APY.

Yes, for variable-rate accounts. APYs fluctuate based on market conditions and the Federal Reserve’s rate changes. Fixed-rate products, like most CDs, keep the same APY for the full term.

Yes — the IRS considers earned interest as taxable income. Your bank will typically send you a 1099-INT form if you earn more than $10 in interest for the year.