Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Interest rates shape stock market performance through borrowing costs, consumer demand, Treasury yields and stock valuations.

In 2026, Federal Reserve and market expectations point to a steady rate path, with roughly one possible cut as inflation risks persist.

Sector leadership has broadened, supporting opportunities across energy, utilities, industrials, technology and healthcare.

Interest rates and the stock market remain closely connected. Changing rates affect borrowing costs for companies and consumers, the amount households spend or save, the income investors can earn from bonds, and the value investors place on future corporate earnings. These connections help explain why investors track both the Federal Reserve (Fed) and the 10-year U.S. Treasury note when they assess the outlook for stocks. At the market close on April 30, 2026, the S&P 500 stood at 7,209, reaching a new all-time high, while the 10-year U.S. Treasury yield was 4.40%, and the fed funds target range stood at 3.50-3.75%. 1

In 2026, the story of interest rates and the stock market goes beyond the Federal Reserve (Fed) alone. Investors are also weighing earnings growth, fiscal policy, tariffs, the Iran conflict, energy prices and shifting sector leadership as they evaluate the stock market. This broader mix keeps rates central to the market conversation while reinforcing that stock performance rarely depends on one variable alone.

Higher interest rates can pressure stocks in several ways. They raise borrowing costs for companies, which can limit investment, slow expansion plans and reduce profit growth. They can also weaken demand for interest-sensitive purchases, such as homes and cars and other large items that often require financing.

Higher bond yields can also compete with stocks by giving investors a stronger income alternative. When investors can earn more income from Treasury securities and other bonds, they may become more selective about how much they are willing to pay for stocks. The effect can be especially important for companies whose profits depend more heavily on future growth than current earnings.

Even so, the relationship between interest rates and stocks is rarely simple. The Fed sets short-term rates, but longer-term Treasury yields move with inflation expectations, economic growth expectations, and government borrowing needs. “Despite higher interest rates, solid corporate earnings growth supports equity prices,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group.

The outlook for 2026 has become more straightforward than earlier in the cycle. After cutting rates by 1% in 2024 and 0.75% in 2025, the Fed kept the federal funds target range at 3.50% to 3.75% at its first three 2026 meetings. Market expectations have shifted from one to two cuts later this year to a steadier rate path as energy supply uncertainty complicated the inflation outlook.

At the Fed’s March meeting, members’ median projection called for one rate cut. Since then, Fed officials’ public comments increasingly emphasized inflation uncertainty. Many policymakers want more confidence that inflation is moving lower in a lasting way before they support additional rate cuts.

Interest rates today reflect a push and pull between growth support and inflation risk. The One Big Beautiful Bill Act cut corporate and individual taxes, while global central banks reduced rates in 2025, making policy more supportive of growth even though those effects take time to move through the economy. Consumer cash flow also adds support, with total individual tax refunds reaching $309 billion as of April 28, 2026, up 16% from the comparable 2025 level and about $44.2 billion higher year-over-year. 1

“Opportunities exist in all markets. Even when interest rates stay elevated, investors can still find strength in sectors with durable demand, improving earnings, or long-term growth themes.”

Terry Sandven, chief equity strategist with U.S. Bank Asset Management Group

Inflation risk from tariffs has not disappeared. After the Supreme Court ruled President Trump could not impose tariffs under the International Economic Emergency Powers Act, the Trump administration announced a temporary 15% global tariff under Section 122 while exploring other options. That policy backdrop still leaves room for higher goods prices than investors faced in 2024.

The Iran conflict adds another layer to the rate outlook. Higher oil prices have kept markets focused on whether higher energy costs will prove temporary or last long enough to affect inflation, economic growth, and corporate profit margins. That uncertainty helps explain why interest rates can remain rangebound even when investors expect eventual Fed cuts.

From 2023 through 2025, information technology and communication services produced some of the strongest gains in the S&P 500. Both sectors outpaced the broader index over that period. 1 That leadership helps explain why many investors came to associate the market’s advance with growth-oriented companies tied to digital services, software, and artificial intelligence(AI).

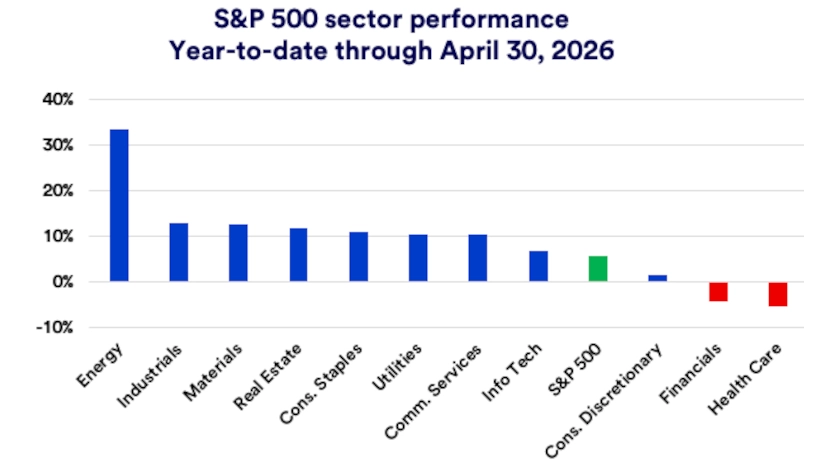

Performance trends in 2026 show a broader leadership mix, as investors respond to the war with Iran and changing macroeconomic conditions. Energy and materials rank as the two best-performing sectors year-to-date, benefiting from energy supply constraints tied to the closure of the Strait of Hormuz. Those sectors can remain strong performers if the conflict with Iran continues to support higher commodity prices and supply concerns.

Information technology and communication services still benefit from the billions of dollars flowing into AI infrastructure. Utilities also benefit from rising electricity demand tied to new data centers, even as interest rates remain elevated. Healthcare, while lagging the rest of the market so far in 2026, continues to offer investors multiple paths for favorable exposure. Pharmaceuticals, biotechnology, medical devices, diagnostics tools, and life sciences each provide distinct growth and risk profiles.

The shift in market leadership shows why opportunity does not depend on one investment style, one sector, or one interest rate environment. “Opportunities exist in all markets,” according to Terry Sandven, chief equity strategist with U.S. Bank Asset Management Group. “Even when interest rates stay elevated, investors can still find strength in sectors with durable demand, improving earnings, or long-term growth themes.”

Investors should view interest rates as one important input, not the entire market thesis. Borrowing costs, consumer spending, bond yields, tax policy, energy prices, and sector fundamentals are all influencing stock prices at the same time. A disciplined investment approach can account for that full picture rather than relying on one forecast about the next Fed meeting.

Investors still have reasons for patience. The 2026 outlook remains constructive because of resilient consumer spending, accelerating technology investment, and supportive fiscal and monetary policy, even as tariffs, inflation, geopolitical tension, and valuations create meaningful risks. “Relatively stable inflation, rangebound interest rates and rising corporate earnings continue to support higher stock prices,” says Sandven.

Interest rates influence stocks through business costs, consumer demand, and investor preferences. Many companies borrow to expand operations, so higher rates can raise interest expenses and reduce profits available for hiring, equipment, and new projects. When rates move lower, borrowing costs can ease, which may support business investment and future growth plans.

Consumer behavior matters as well because many large purchases depend on financing. Higher rates often increase monthly payments on loans, which can reduce demand for durable items such as homes, appliances and vehicles and weaken sales for related businesses. Higher rates can also draw money toward bonds and away from stocks as investors may prefer the surety of income from bonds relative to uncertain returns on stocks. Higher rates can also reduce what investors are willing to pay today for profits expected further in the future.

Stock markets often respond quickly when the Federal Reserve raises or cuts interest rates. Rate hikes can slow parts of the economy by raising borrowing costs, and they can increase the appeal of investments like CDs and bonds that offer interest income. Companies may also face higher debt costs, which can reduce spending on expansion or replacing old equipment and pressure profits.

Rate cuts are designed to support economic activity by lowering the cost of borrowing. Lower loan costs can encourage consumer spending and make it easier for companies to finance growth initiatives. When interest rates are lower, some investors may shift assets toward stocks in search of higher long-term return potential.

Investors often compare potential stock returns to what they can earn in U.S. Treasury securities, where interest and principal payments are backed by the U.S. government. When rates rise, Treasury yields can become more competitive, which may reduce demand for stocks. When rates fall, Treasury yields can decline, which can make stocks comparatively more attractive for investors seeking growth.

Investors also consider how rate levels change the market’s focus between near-term results and longer-term growth. When rates are low, investors often place a higher value on companies expected to grow profits more in future years. When rates are high, investors may place more emphasis on companies generating profits today, including those that pay dividends, rather than relying primarily on future earnings growth.

Yes, inflation matters because it often shapes the path of interest rates and corporate margins. If inflation stays high, the Federal Reserve may have less room to cut rates, and companies may face more pressure from higher input and wage costs. In 2026, tariffs and higher oil prices tied to the Iran conflict kept inflation in focus even as other parts of inflation were more stable.

Higher-rate environments do not automatically rule out strong stock performance. In 2026, investors favored sectors with stronger pricing power, steadier demand, or direct exposure to higher energy prices, including energy, industrials, materials, and utilities. Technology and healthcare can also continue to offer opportunities when powerful long-term trends such as artificial intelligence, aging populations, and medical innovation support earnings growth.

The Federal Reserve kept rates at 3.50%–3.75%, noting improving inflation and labor trends as investors continue to price in two cuts for 2026.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.